BarFZ

John H. Frenzl Trust — Full Case Timeline (Working Drafts)

Ch.0 — The Foundation (1950-01-01 – 2012-12-15)

Status: Narrative draft v2 (2026-06-13) — upgraded to chapter-consistent format: intro, analysis, inline images (hash-matched via

ch0_image_map.txt), escaped dollar amounts, forward-links. Awaits Landon's factual verification + caption confirmation. Source:_INCOMING/2026.05.16 BarFZ OneNote/exported/Ch.0 1950.01.01-2012.12.15.mhtFrame note: This is the bedrock chapter. Everything Justin Imhof did in Ch.2–Ch.10 is a departure from the 50/50 equal-partnership the Frenzl brothers built here over fifty years. Read this to know what "normal" looked like — so the breaks read as breaks.

INTRO — Two Brothers, One Operation, Fifty Years

Chapter 0 establishes the baseline: who the Frenzls were, what they built, and the equal-partnership intent that every later document either honored or violated.

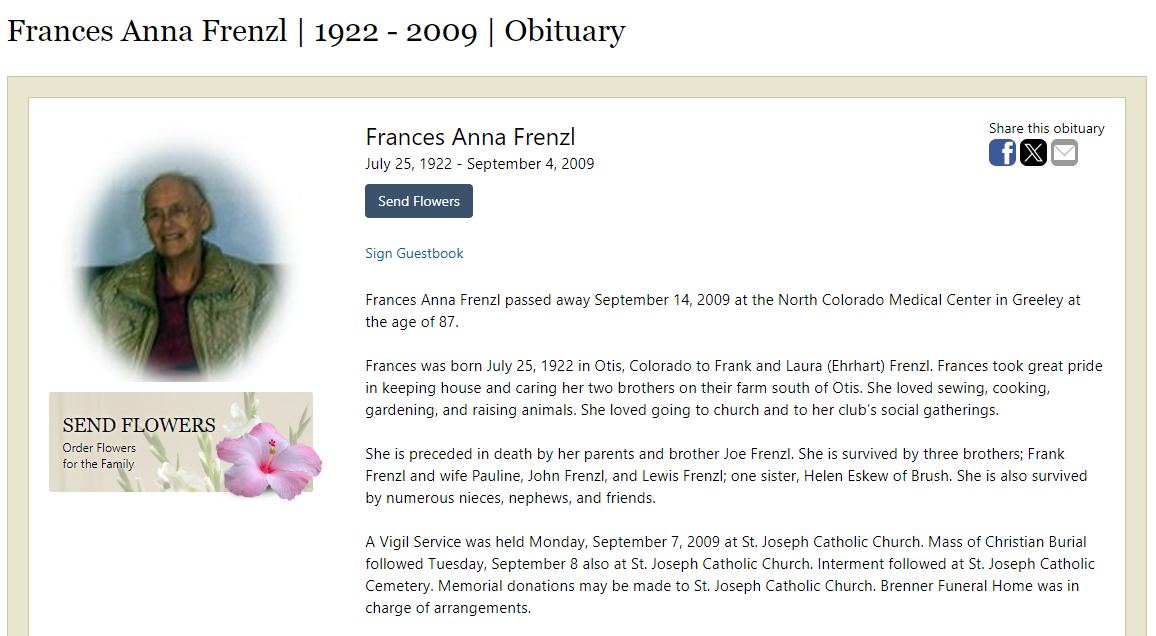

John and Lewis Frenzl were unmarried brothers who farmed Washington and Yuma County, Colorado, ground together their entire adult lives — joined by their unmarried sister Frances, who lived with them until her death in 2009. From a handshake partnership begun in 1961, formalized in a written 50/50 partnership agreement in 1976, through decades of jointly-titled land, shared equipment, and a home they built and lived in together, the brothers operated as one. They had no children. Their estate plan, executed as identical reciprocal trusts in 2000, was built to pass their life's work — after caring for each other — to their nephew Bill Eskew and niece Teresa Imhof, with a standing gift to the Lewis & John Frenzl Scholarship Fund for Washington County graduating seniors.

Two facts from this chapter become the legal spine of the entire case:

- Everything was 50/50 — even when title wasn't. For practical reasons (a 1997 UCC filing, valuation parity), the irrigated half-section stayed 100% in John's name and the homestead stayed 100% in Lewis's name in 2000 — but both brothers treated all of it as a shared 50/50 interest, and the tax record proves it (homestead improvements were booked half to John's trust right up through 2015 — Ch.1/Ch.2). This is why Justin's later "Lewis owned the homestead outright" framing fails.

- John's death made his trust irrevocable. When John died December 15, 2012, the John H. Frenzl Trust became irrevocable under its own Article VII — "the interest of the Beneficiaries is paramount." From that moment, the trust's terms were fixed, its accounting owed to its beneficiaries (Article XVI), and any breach answerable to a court (Article VI). Lewis became Trustee. The watch had begun.

Family voice — getting our bearings We built this chapter early, before we understood what we were looking at — so for a while it was just names, deeds, and old farm equipment. It matters now because it's the measuring stick. When you know that John and Lewis split everything down the middle for fifty years, every later move — the leases Justin wrote himself, the homestead deeded to his own estate, the equipment auctioned without the trust seeing a dime — reads as exactly what it is: a man taking the half that wasn't his.

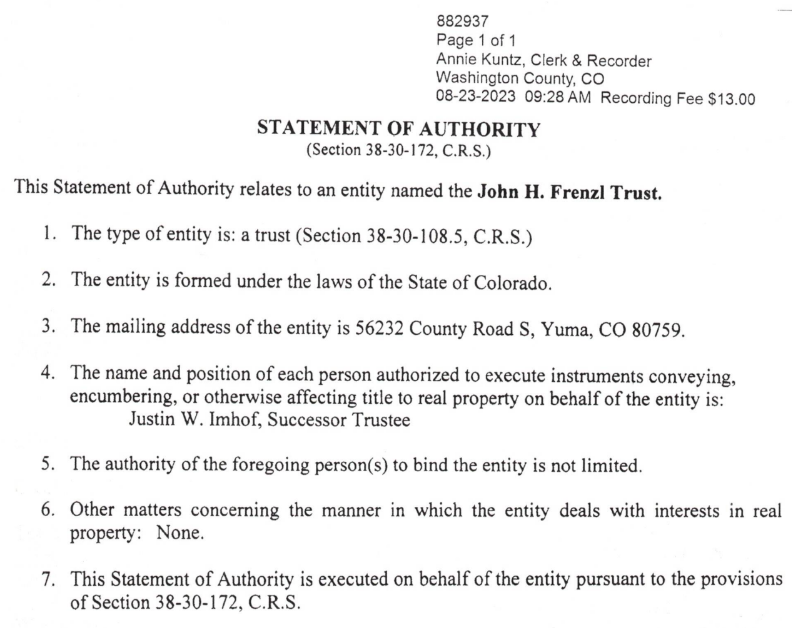

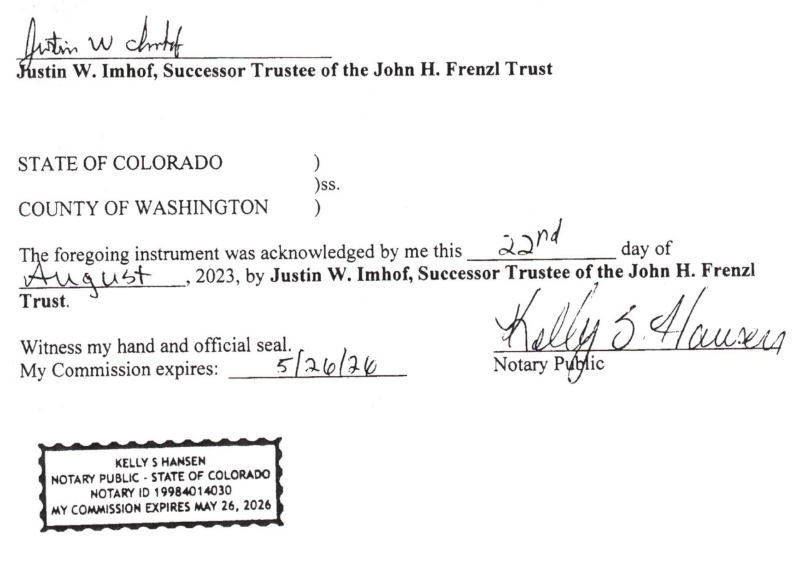

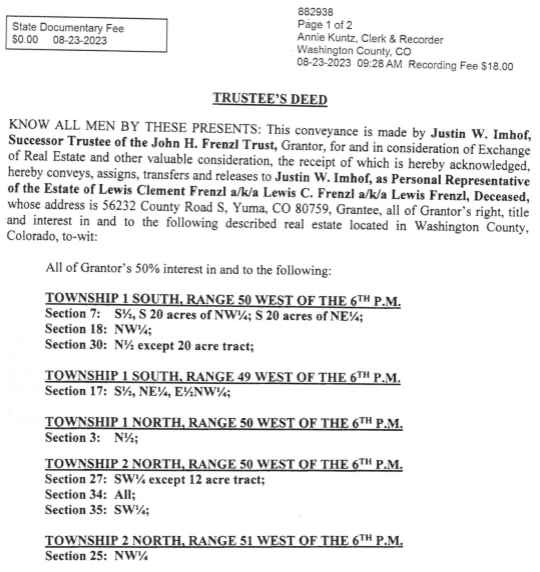

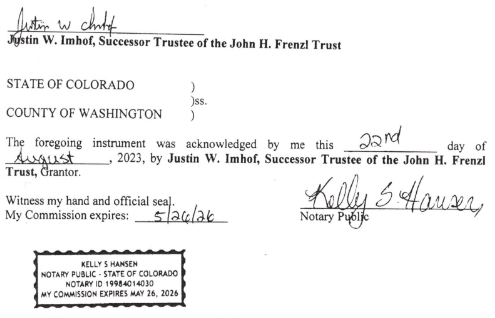

Frenzl Family Tree (Petitioner's Exhibit 1)

Parents: Frank and Laura (Ehrhart) Frenzl. Children: Frances (unmarried), Frank, Joe, John (unmarried, no children), Lewis (unmarried, no children), and Helen (Frenzl) Eskew — the link between the Frenzl and Eskew families.

The line that matters for the trust: Helen's children include Billie "Bill" Eskew and Patty (Eskew) Doyle CO/PJD/PJD; and Teresa (Frenzl) Imhof. Bill Eskew married Karen Gardner; their sons are Landon Eskew and Devin Eskew. Teresa (and Doug) Imhof's children are Justin Imhof and Karie Imhof.

The beneficiary geometry, fixed here: the JHF Trust's remainder runs to Bill Eskew and Teresa Imhof equally — i.e., to the Eskew side (Bill → Landon & Devin) and the Imhof side (Teresa → Justin & Karie). Justin Imhof is not a named beneficiary of the JHF Trust; he is Teresa's son. Every later document that lists "Justin and Karie Imhof" as the beneficiaries (Ch.4's bank agreement) misstates this foundational structure. (Note the deliberate distinction the source flags: William Eskew ≠ Billie Eskew.)

PETITIONER'S EXHIBIT #1 — Frenzl family tree. Doris Dean (Kerst) Imhof (2/8/1931–9/18/2022) married Glen Imhof; Evan Imhof (son of Leslie) is Justin's cousin.

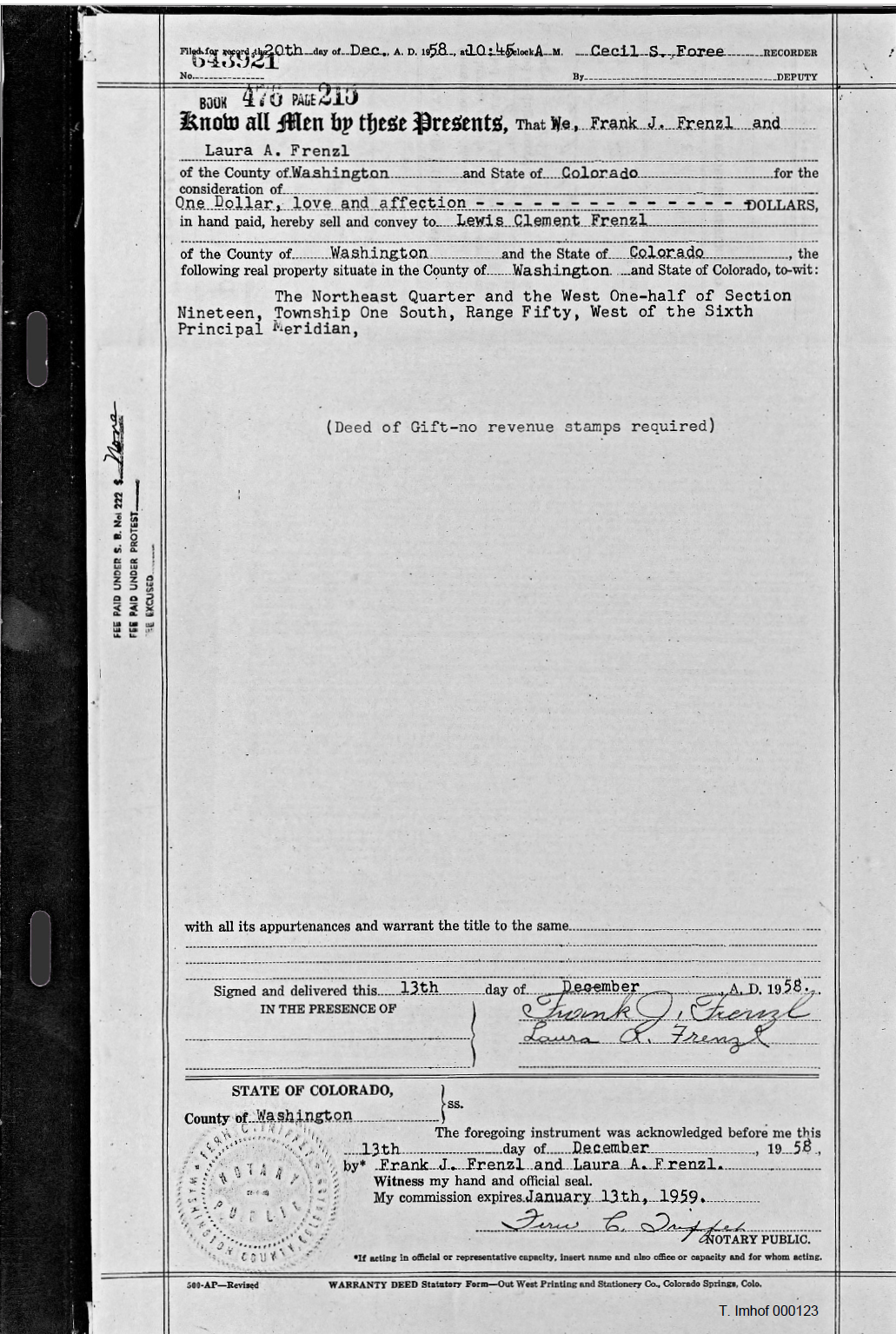

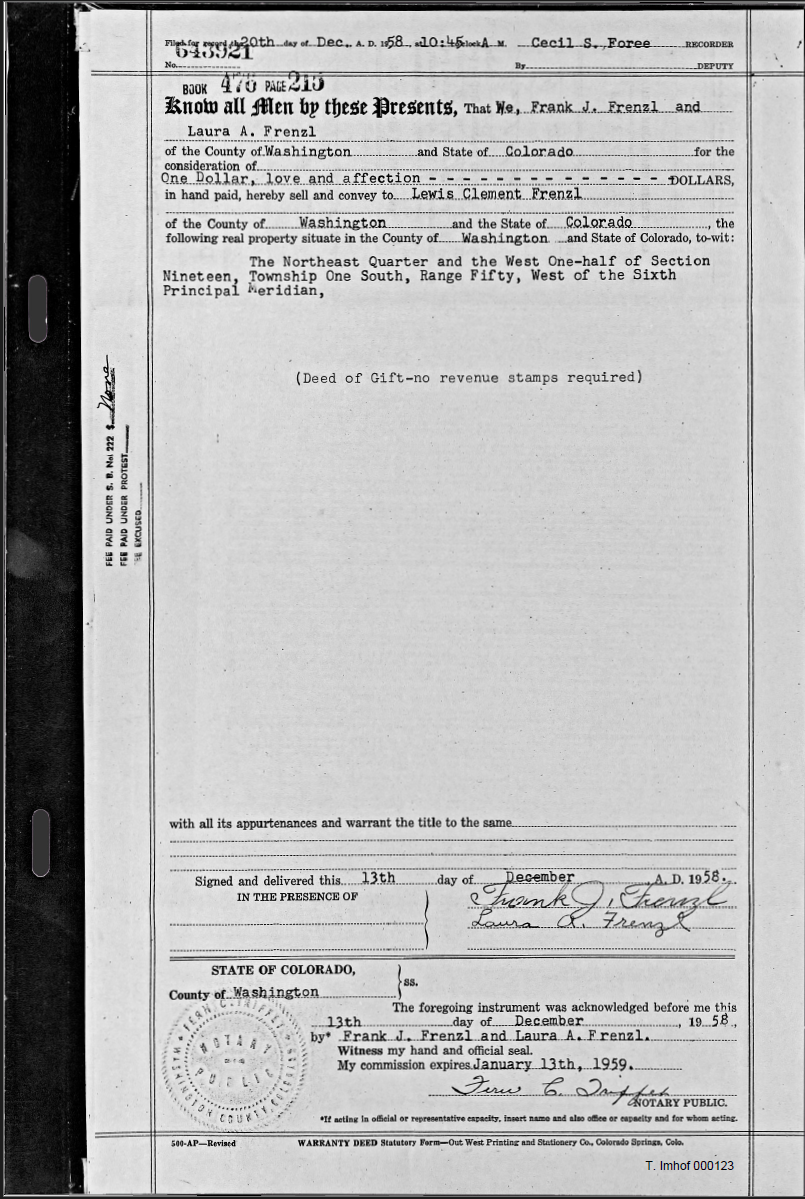

1958 — The Homestead Deeded to Lewis

12/13/1958 — Frank and Laura Frenzl deed the 480-acre "Frenzl Homestead" to Lewis Frenzl. Note that John Frenzl is not mentioned in this document — a title fact that, decades later, Justin would lean on, even though the brothers' entire course of dealing treated the homestead as shared.

12/13/1958 Warranty Deed, Frank & Laura Frenzl → Lewis Frenzl, 480-acre homestead (T. Imhof 000123). Attachments from Sara Wagers email 11/8/2024.

1961 — The Partnership Begins

John and Lewis Frenzl begin working together as a 50/50 partnership, intending to combine their business ventures. (Established in the 1976 agreement's own recital; from JWI*002130.)

Partnership origin recital (JWI 002130) — "conducting business activities in partnership form since 1961."

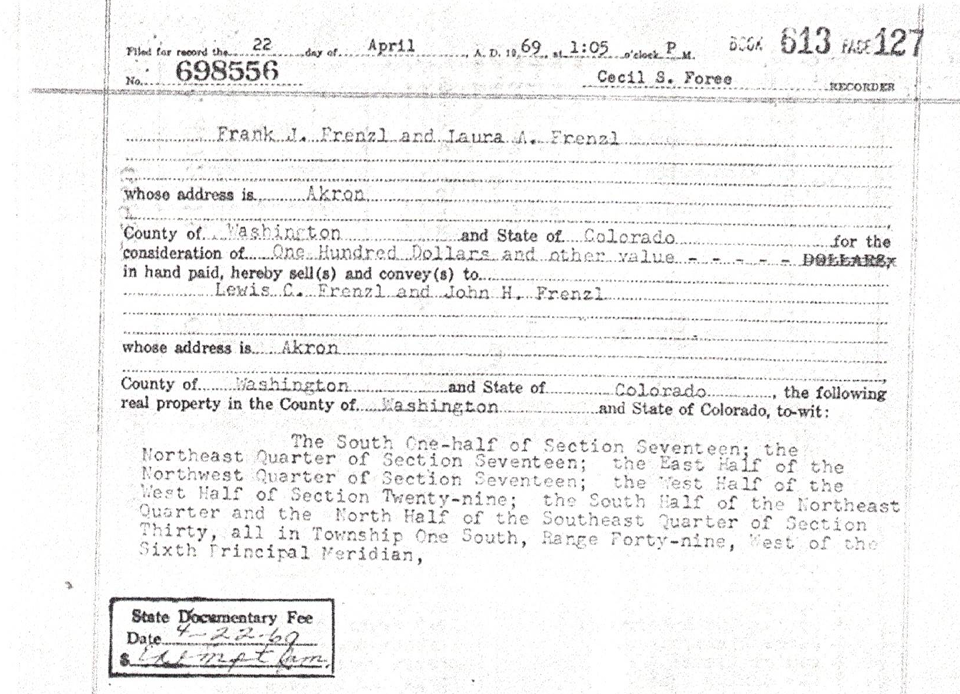

1969 — Parents Convey Land to Both Brothers Equally

4/22/1969 — WaCo REC#698556. Land is conveyed from Frank and Laura Frenzl (parents) to both Lewis and John Frenzl (children) — both names on the document equally. The equal-treatment pattern is on the public record from the start.

PETITIONER'S EXHIBIT #2 — 4/22/1969 deed, parents → both brothers equally. 698556

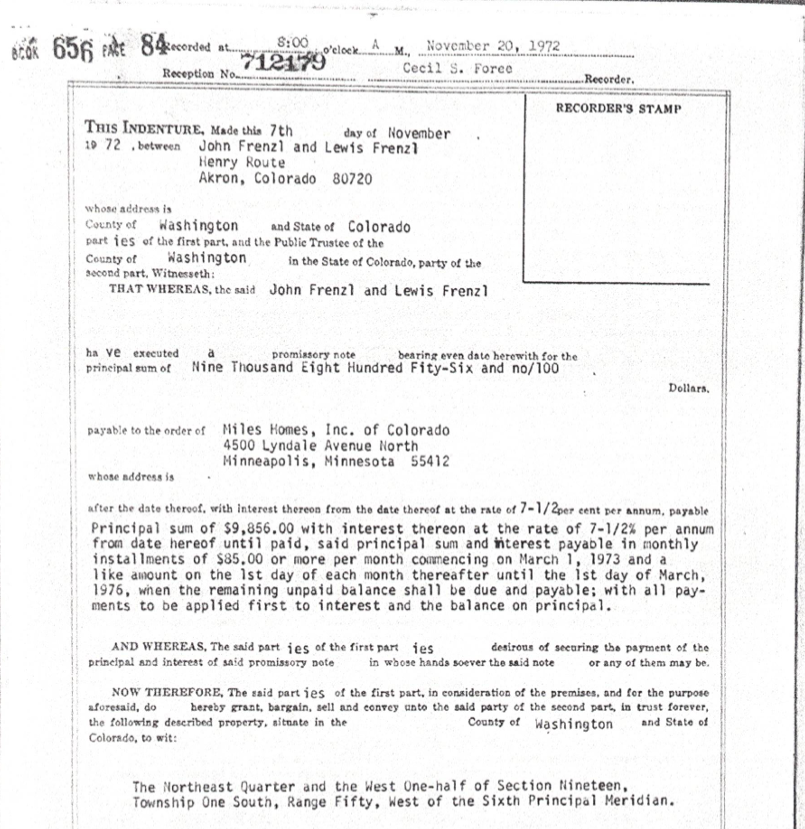

1972 — The Home They Built Together

11/7/1972 — WaCo REC#712179. Both John and Lewis Frenzl execute a promissory note for a new home built on their property — the home they would live in together as unmarried bachelors with no children, alongside their sister Frances (until her 2009 death).

The house both brothers signed for became "Lewis's" on paper — and Justin's in the end. Both brothers signed the 1972 note; both lived there for the rest of their lives. Yet this 480-acre homestead asset, with all improvements, was titled exclusively under Lewis Frenzl's 2015 Estate after the prior trust documents were reworked (Ch.2), and is now solely under Justin Imhof's control as of November 30, 2023 (Ch.3, REC#883505). A house two brothers built and paid for together ended in one great-nephew's hands.

PETITIONER'S EXHIBIT #4 — 11/7/1972 promissory note for the home (REC#712179). Legal: W½ Sec 19, T1S R50W.

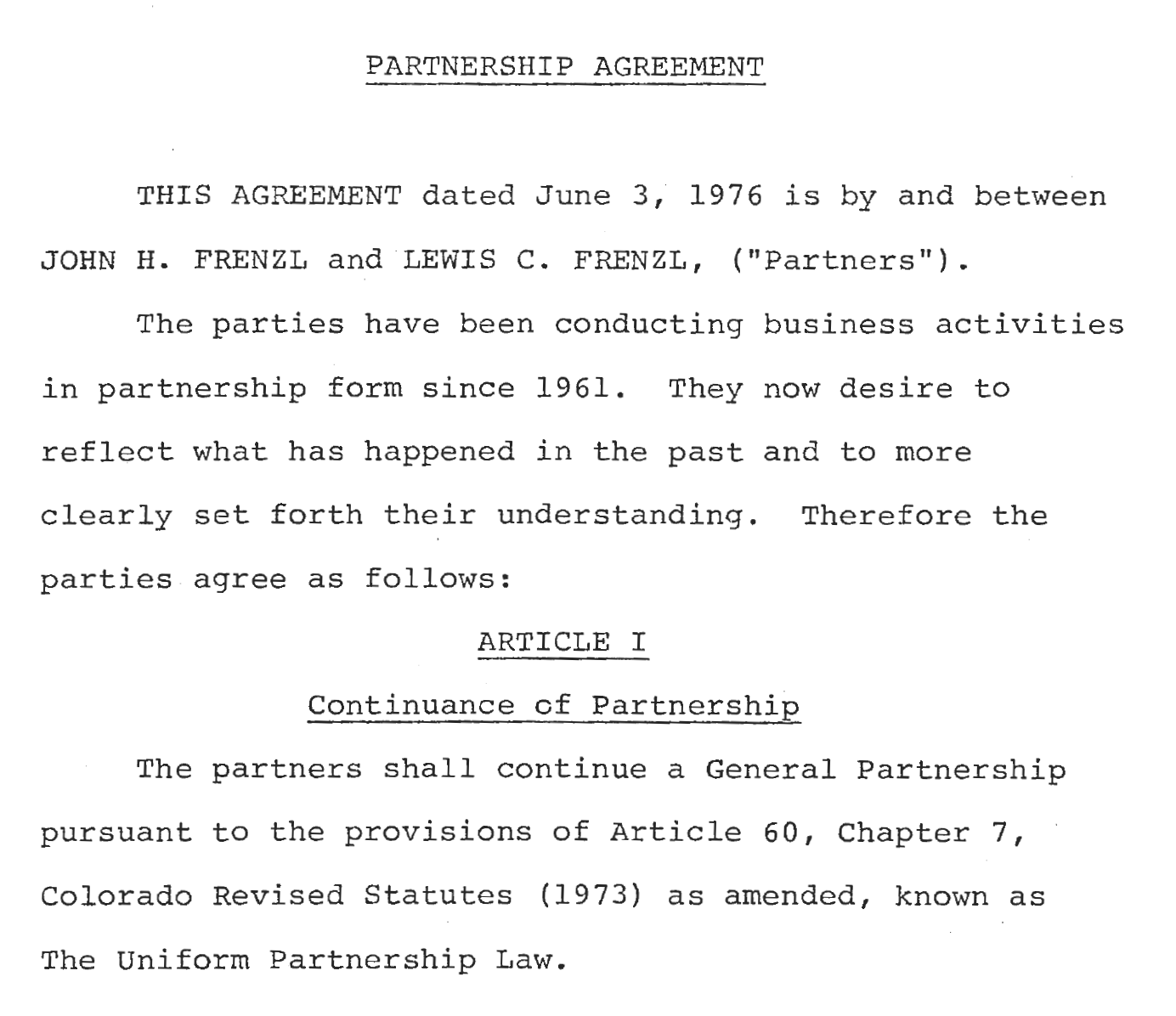

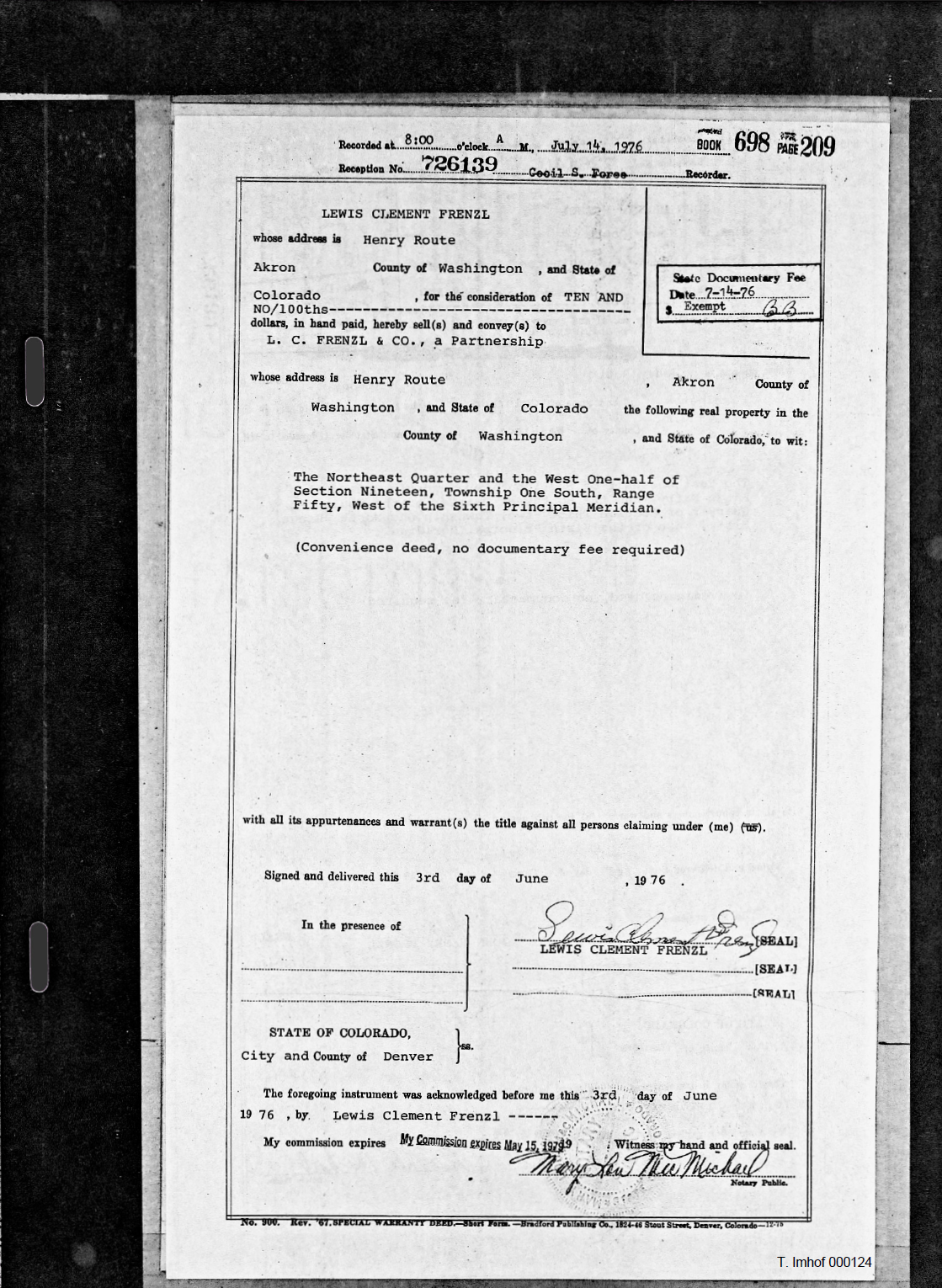

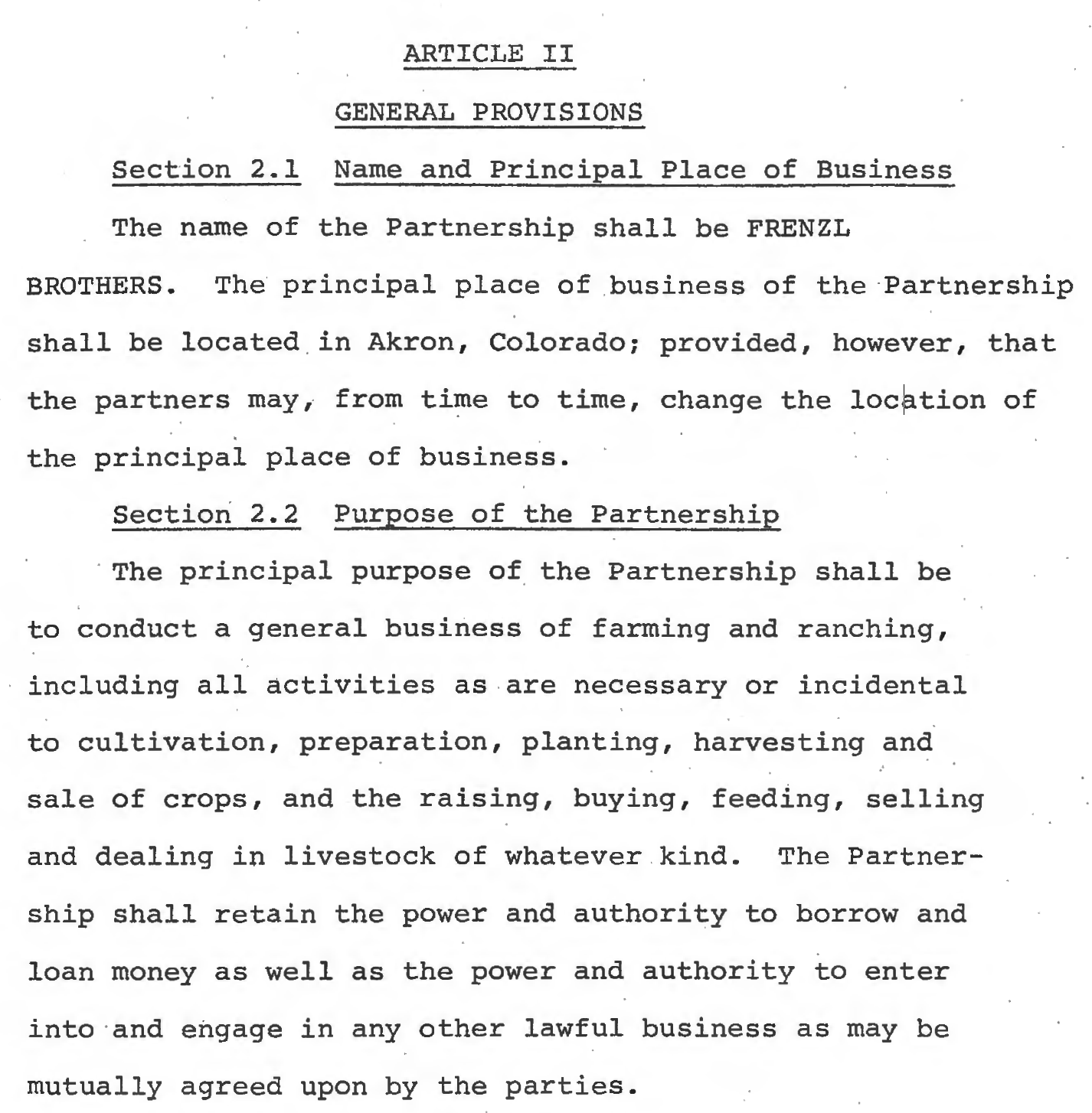

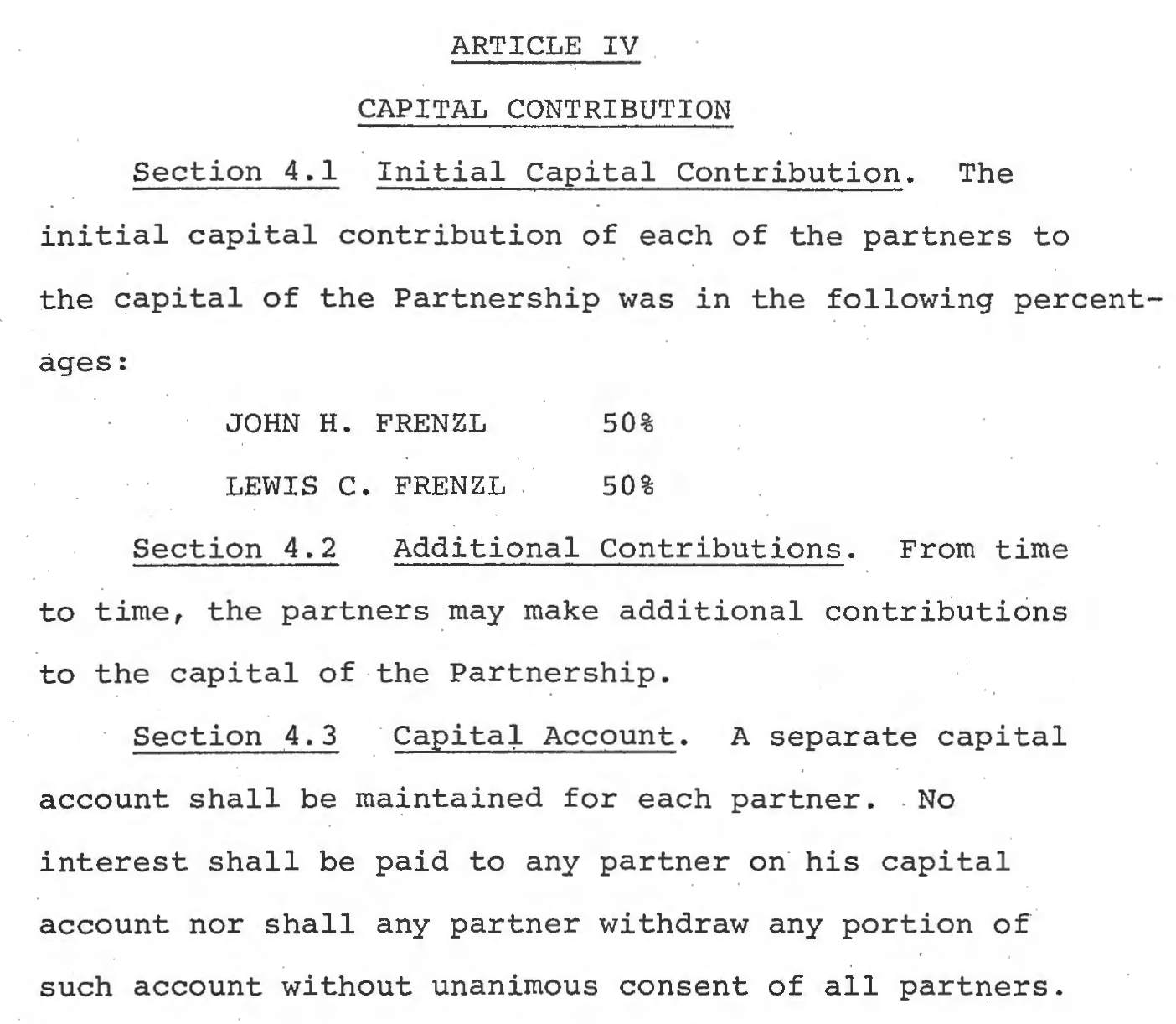

1976 — The 50/50 Partnership Agreement (the Bedrock Document)

6/3/1976 — A single day that defines the operation. Lewis quit-claims the 480-acre homestead from his personal name into L.C. Frenzl & Co., a Partnership, and on the same day the brothers execute a written Frenzl Brothers, LP partnership agreement — formalizing the 50/50 they'd run since 1961. The agreement's own first page: the parties have "been conducting business activities in partnership form since 1961" and "now desire to reflect what has happened in the past."

Key terms (J. Imhof production 2130–2156):

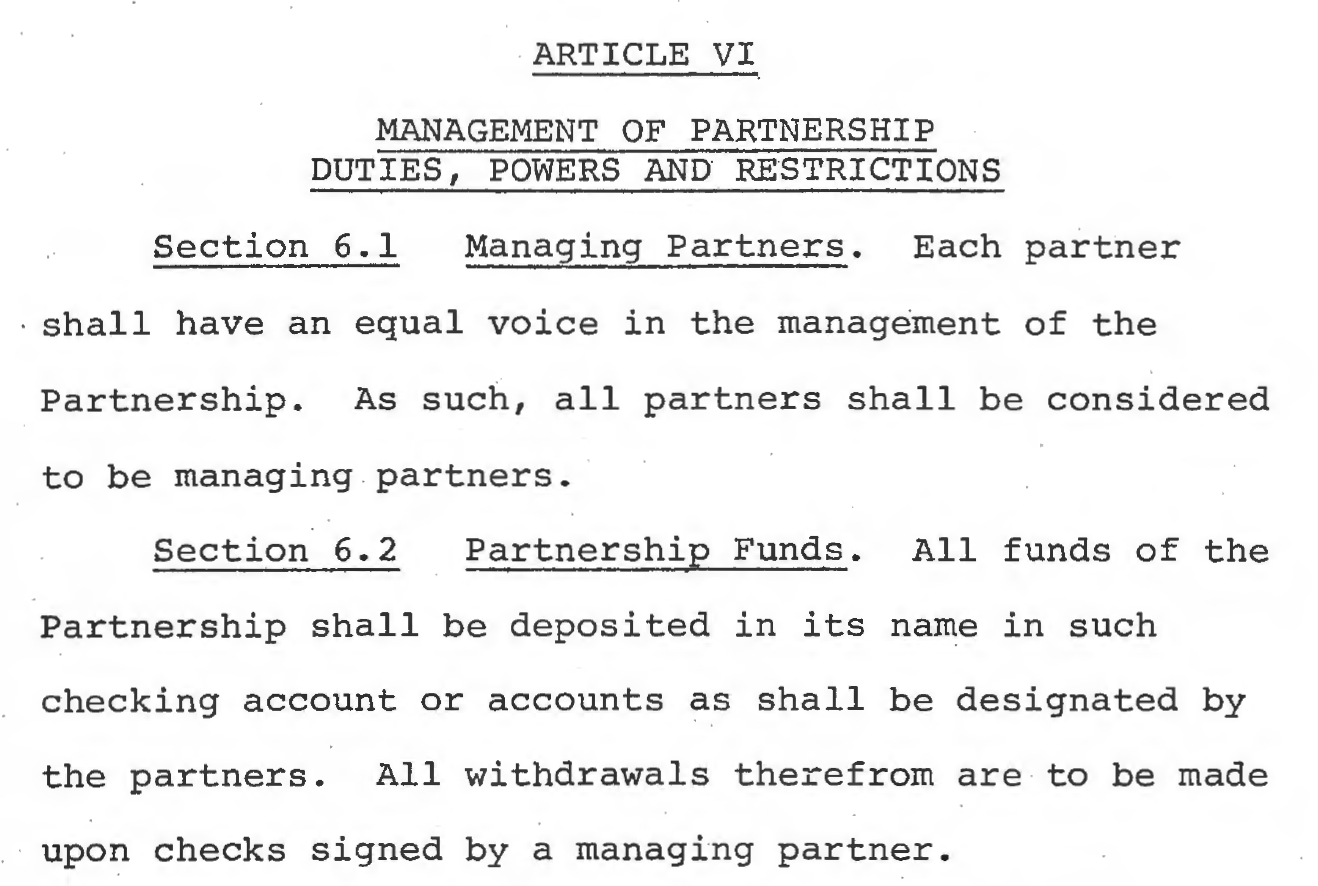

- "Each partner shall have an equal voice in management of the partnership." (2136)

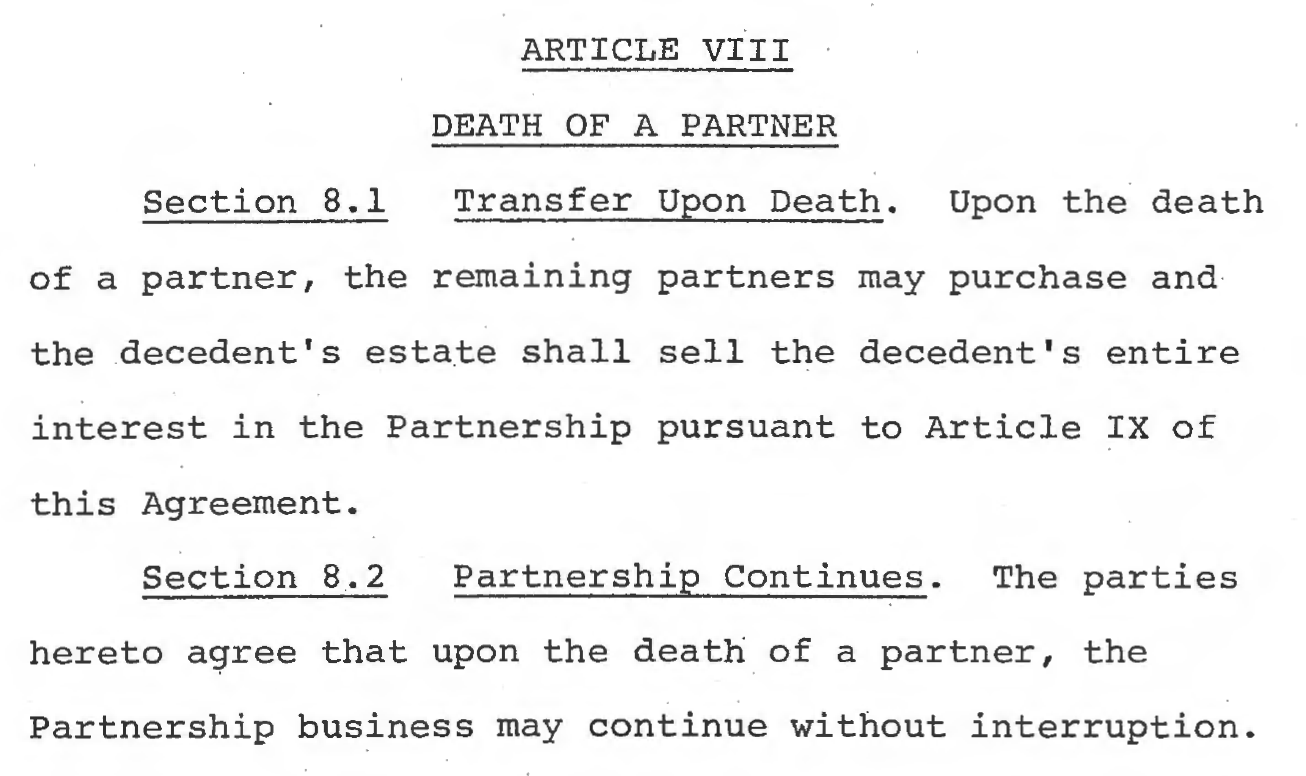

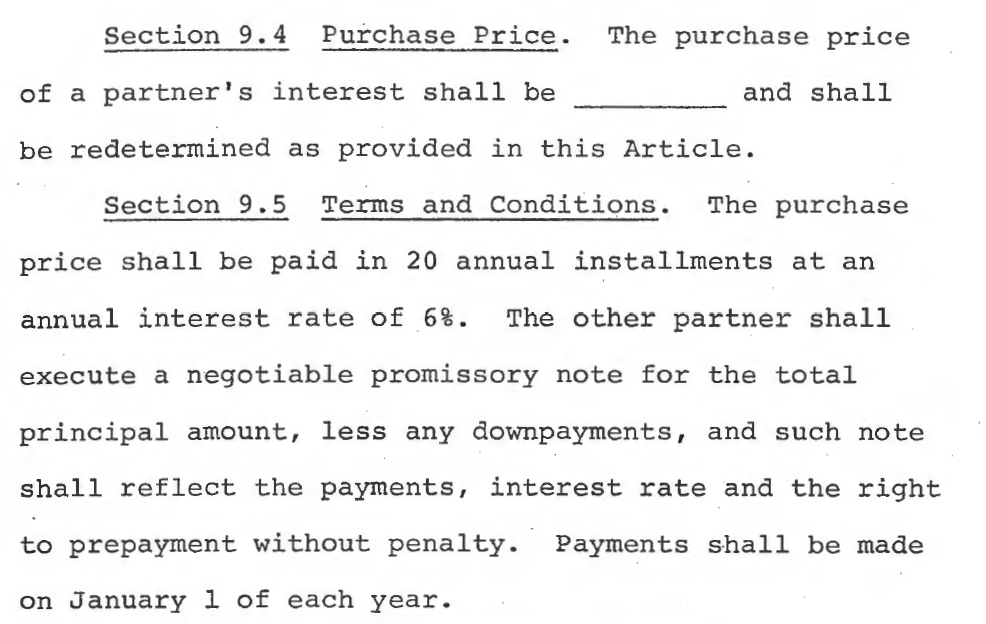

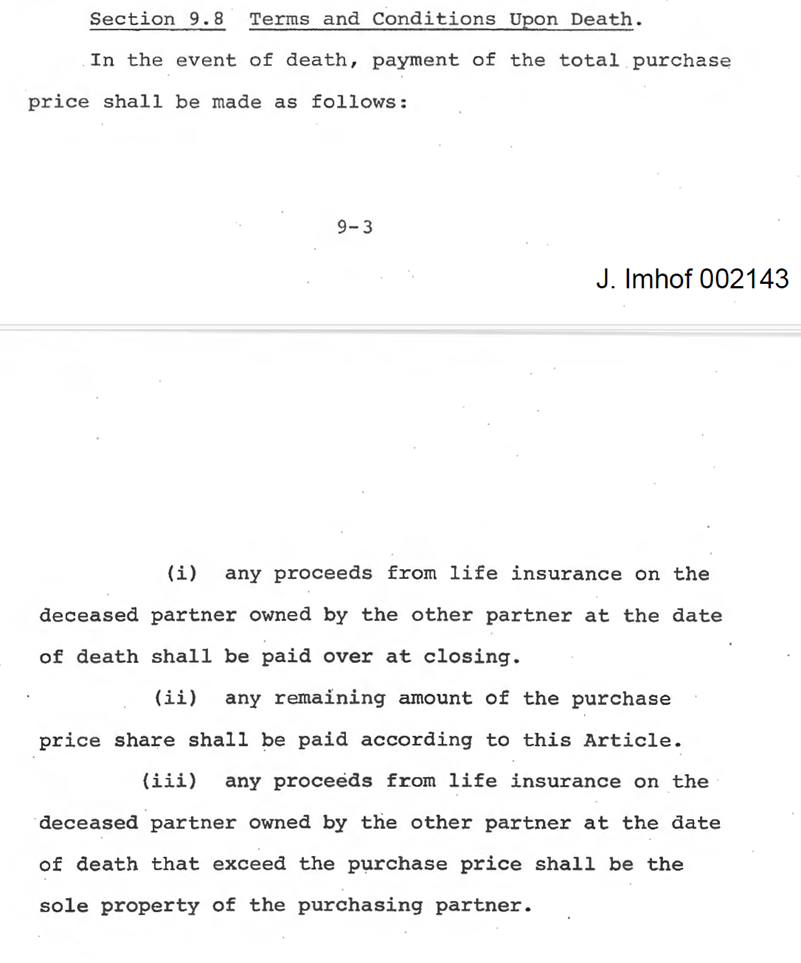

- On a partner's death, the survivor may purchase and the decedent's estate shall sell the decedent's entire interest under Article IX — first-refusal buyout, with an appraisal of assets and treatment of life insurance (2140, 2142–2144). The partnership "may continue without interruption."

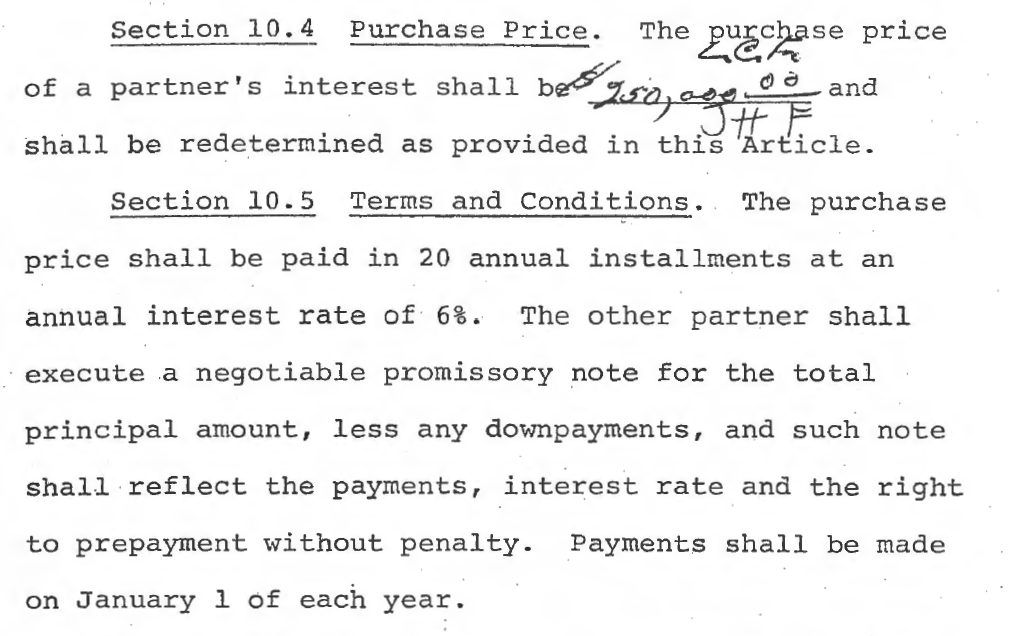

- Article X implies the brothers' collective assets were valued around $500,000 (half required for buyout) — covering the 1972 house, homestead land, the 560 acres from the 1972 transfer, seed, and equipment. (2146)

- Article XI — intent to carry life insurance on each partner. (2150)

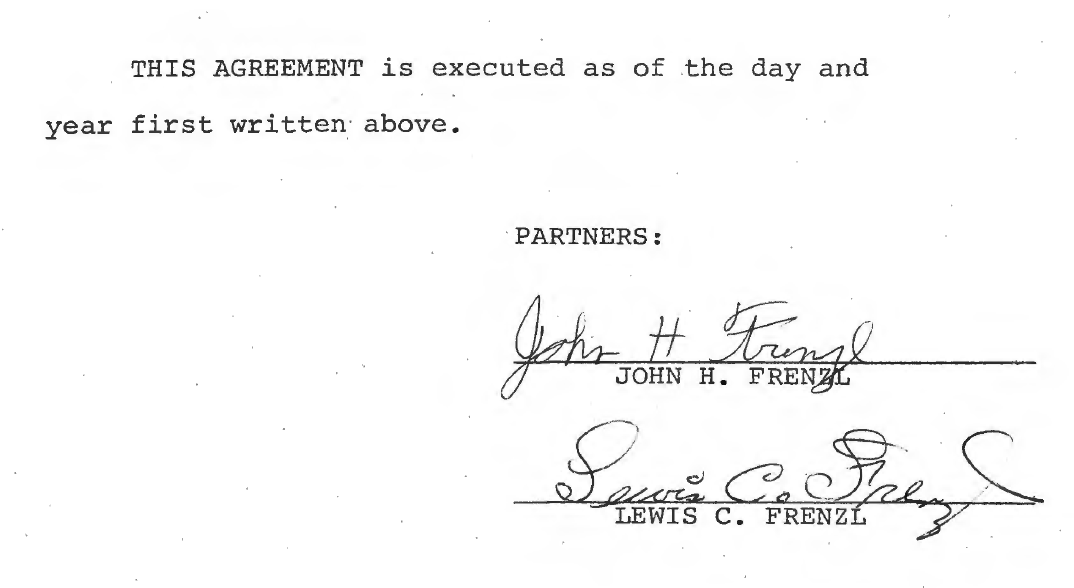

- Signed by both brothers 6/3/1976. (2156)

Why the partnership agreement matters to the fraud. Colorado's Uniform Partnership Law (C.R.S. § 7-60-139) gives a partner defrauded in a partnership the right to a lien on partnership surplus, to stand in creditors' shoes, and to be indemnified by the person who committed the fraud. John's half of Frenzl Brothers flowed, on his death, into the JHF Trust — so the trust inherited John's partnership rights, including these fraud remedies. The 1976 agreement is not just history; it is a live source of the trust's claims.

6/3/1976 Frenzl Brothers LP partnership agreement pages (J. Imhof 2130–2156) + same-day homestead quit-claim into L.C. Frenzl & Co. Articles IX (buyout), X ($500k valuation), XI (life insurance).

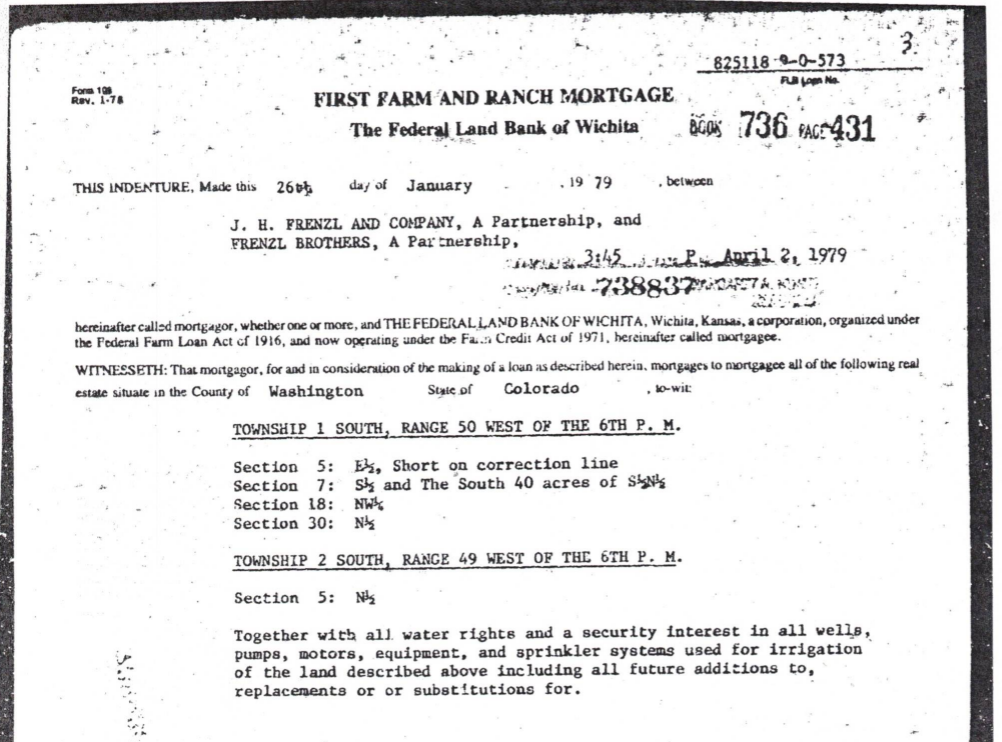

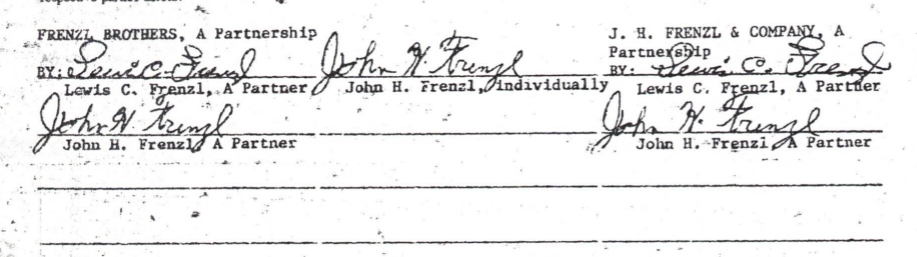

1979 — Joint Land Purchases as Partnerships

1/26/1979 — WaCo REC#738837. 1,445 acres purchased by J.H. Frenzl & Co. and Frenzl Brothers (both partnerships), cosigned by John Frenzl individually; John and Lewis sign for each partnership entity. (Also 4/2/1979, Yuma County land, JHF & LCF signing as partnership.)

PETITIONER'S EXHIBITS #5, #6 — 1/26/1979 (REC#738837) + 4/2/1979 Yuma purchases, both partnerships. 738837

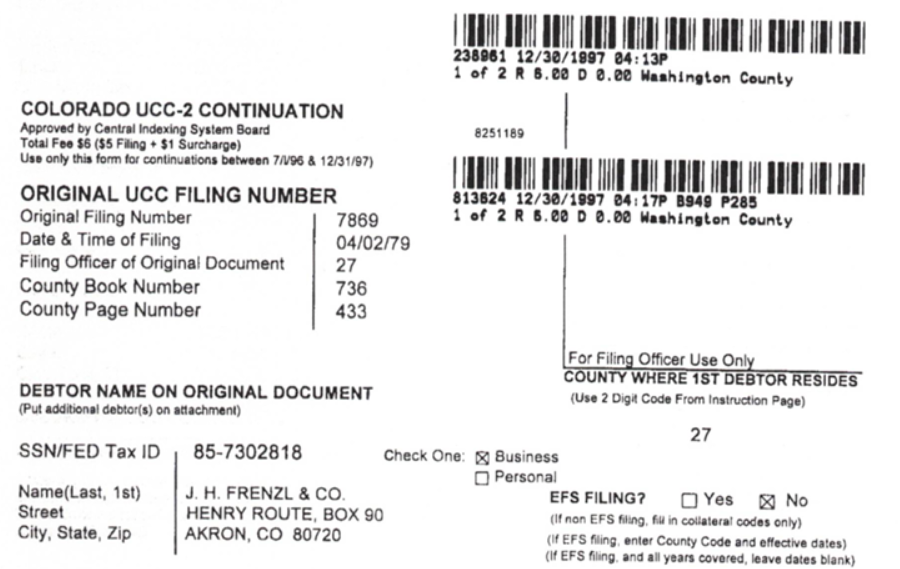

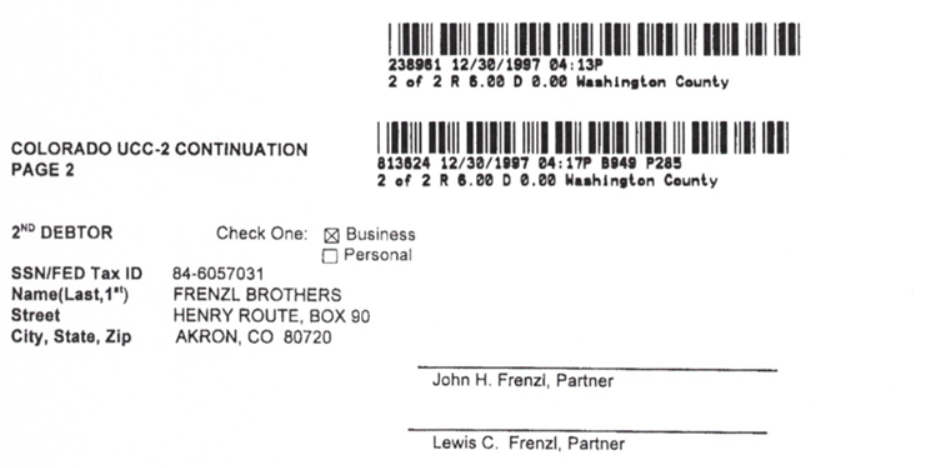

1997 — UCC Filing: Both Brothers as Partners

12/30/1997 — WaCo REC#813624. A UCC filing shows both brothers as partners on the operation's land — the encumbrance that helps explain why, in 2000, the brothers left certain parcels singly-titled rather than re-papering everything.

PETITIONER'S EXHIBIT #7 — 12/30/1997 UCC filing (REC#813624), both brothers as debtors/partners. 813624

2000 — The Reciprocal Trusts (the Structure Lewis Later Revoked)

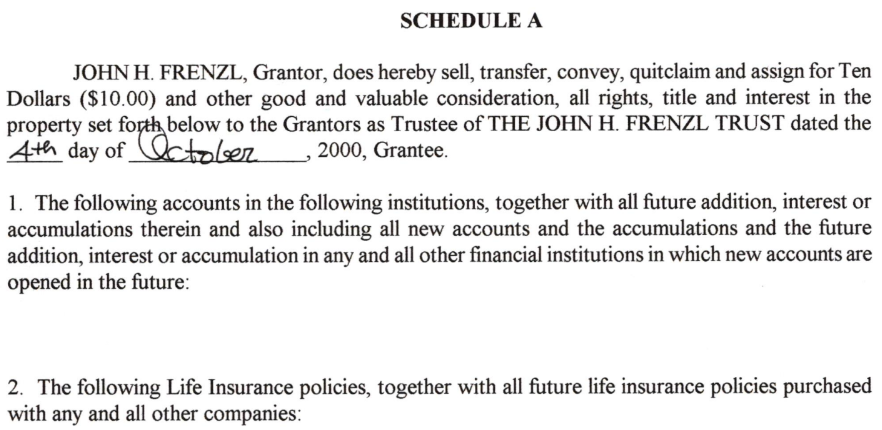

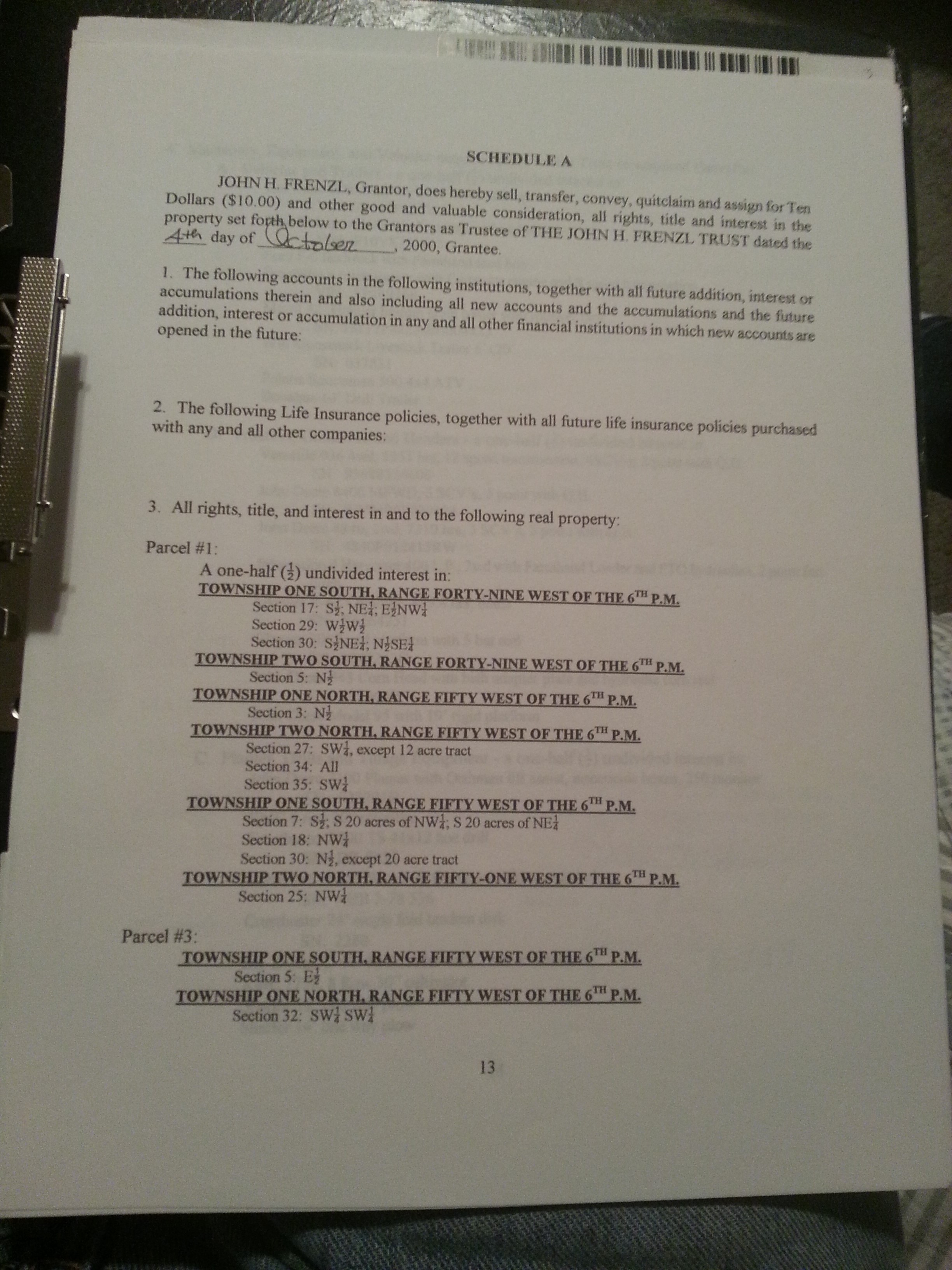

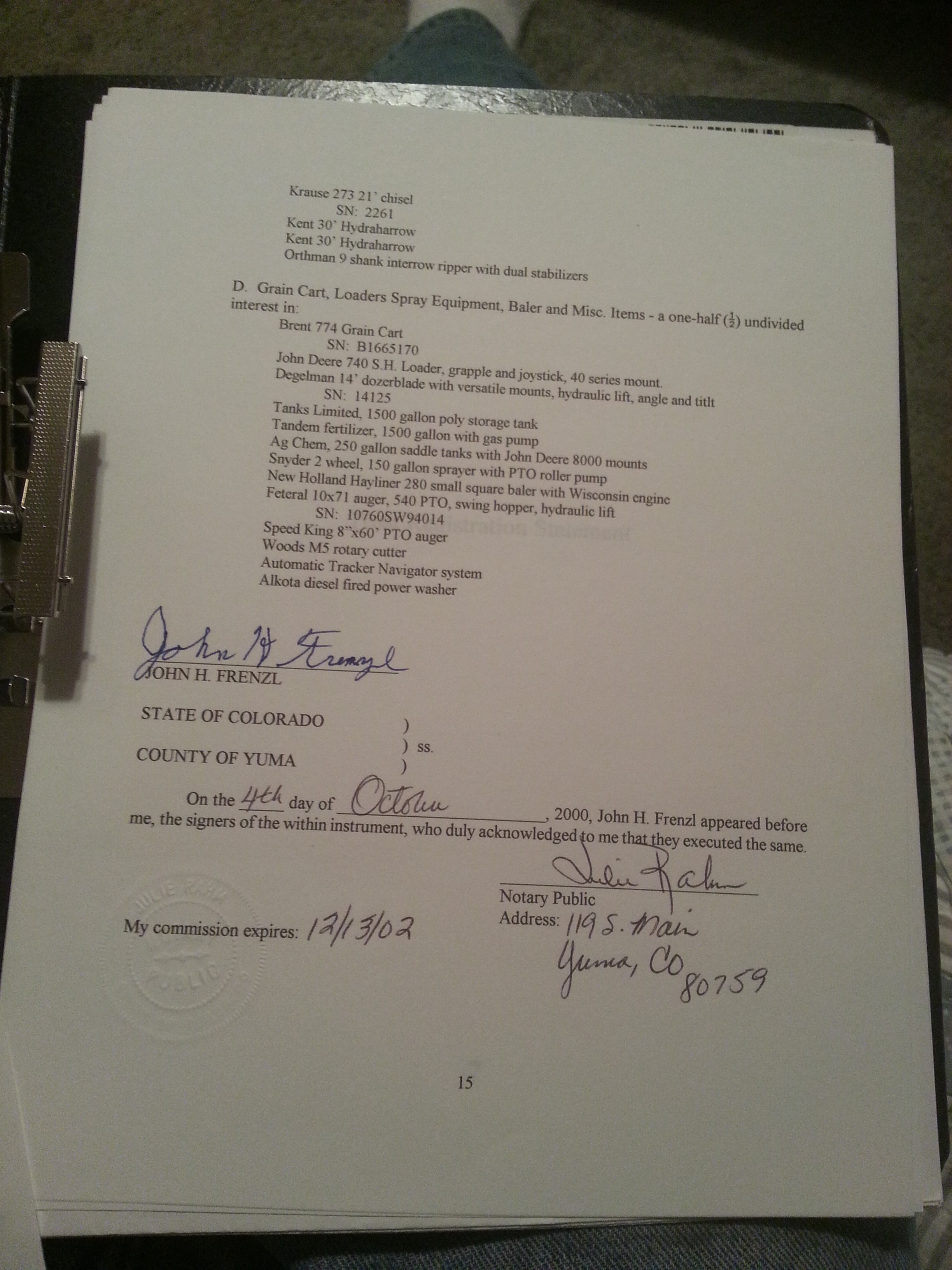

10/4/2000 — Through Yuma trust attorney Judith Shively, John H. Frenzl creates the John H. Frenzl Trust, a Will, and Schedule "A"; Shively creates an identical trust for Lewis the same day — the only difference being the names at the top. Both brothers signed independently, same day. (Notarized by Julie Rahm.)

10/18/2000 — WaCo REC#821185. To split value as evenly as possible without re-papering encumbered parcels, the irrigated half-section stays 100% in John's name and the homestead stays 100% in Lewis's name — but "both brothers continued to treat all property as a 50/50 interest, including the homestead where the two brothers still reside together with their sister Frances."

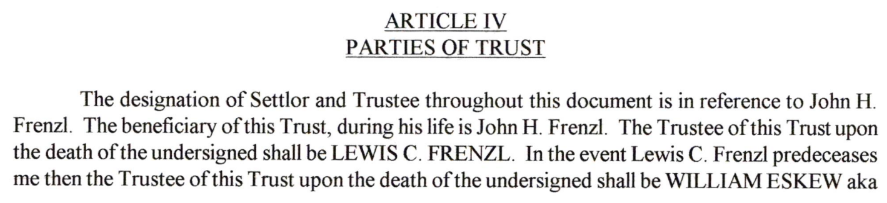

Notable JHF Trust terms (these are the duties later breached):

- Article IV — on John's death, Lewis becomes Trustee; income beneficiaries are Lewis and the Scholarship Fund.

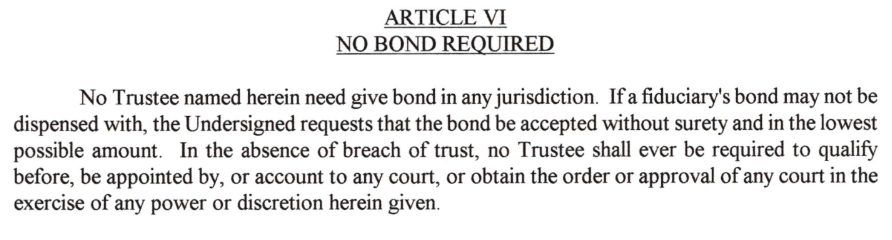

- Article VI — on a breach of trust, the Trustee must account to, obtain approval from, and qualify before a court.

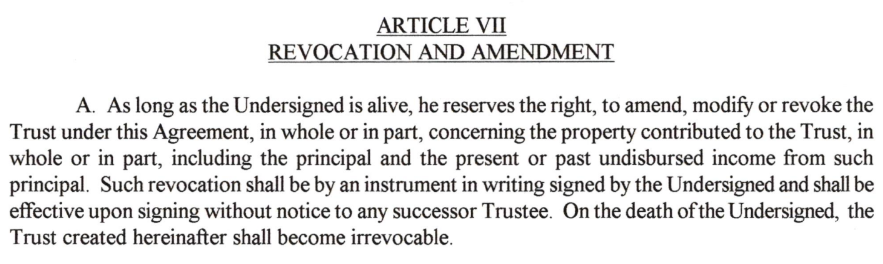

- Article VII — on John's death the Trust becomes irrevocable; "the interest of the Beneficiaries is paramount."

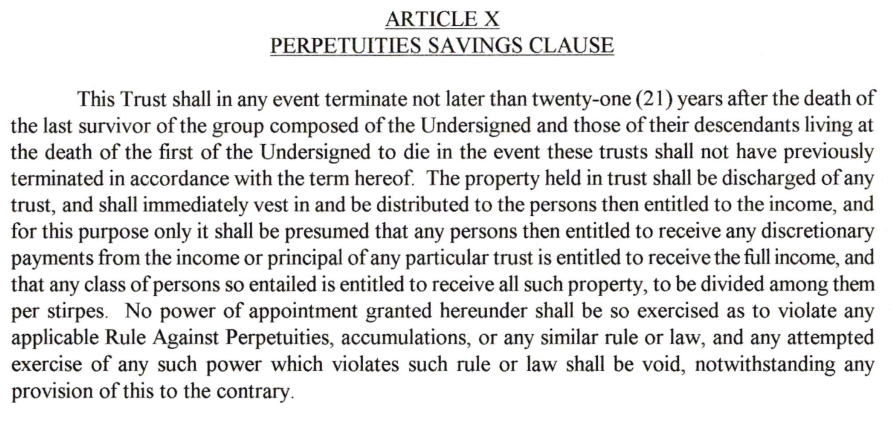

- Article X (perpetuities) — Trust terminates 21 years after John's death (≈12/2033).

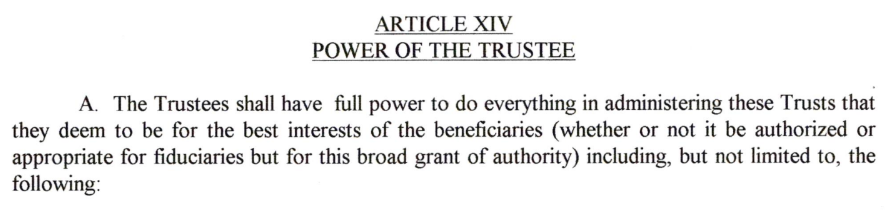

- Article XIV — Trustee powers, but only "within the best interests of the Beneficiaries." (Includes a self-dealing-notwithstanding clause Justin would later lean on.)

- Article XVI — Trustee shall render annual accounts of income and expenses to all Beneficiaries.

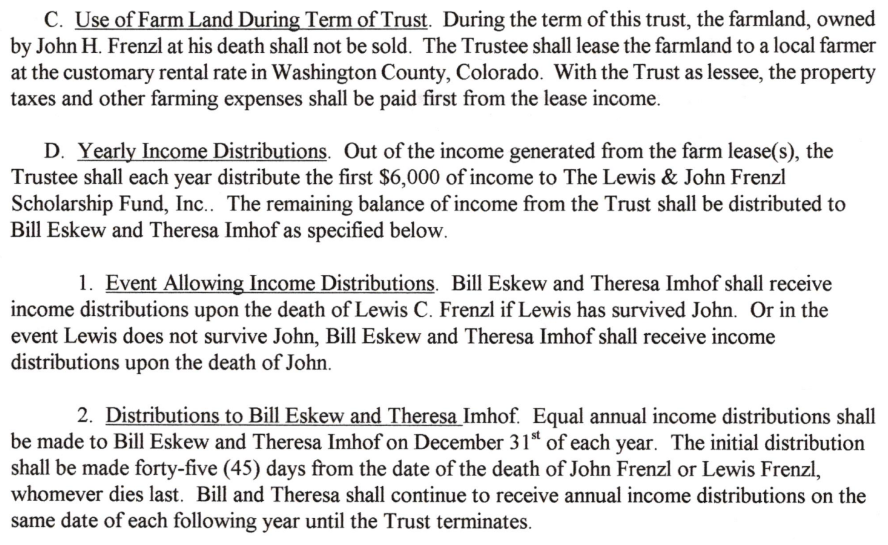

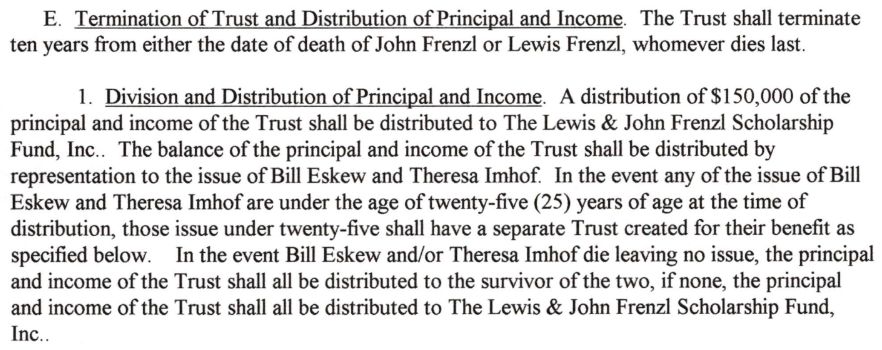

- Article XXII — disposition: first $6,000/yr to the Scholarship Fund, remainder to Bill Eskew and Teresa Imhof; on termination, $150,000 to the Scholarship Fund, balance to the issue of Bill and Teresa.

- Article XXIII — Beneficiaries: Lewis, Bill Eskew, Teresa Imhof. Trustee succession: John → Lewis → Bill Eskew → Teresa Imhof. Children defined: Bill's are Landon and Devin Eskew; Teresa's are Justin and Karie Imhof.

Every later breach has its mirror here. The annual accounting Justin never kept (Article XVI; Ch.4 Hansen admission). The court-accountability-on-breach he engineered around (Article VI; Ch.2 Will absolution clauses). The irrevocability he claimed prevented sales but permitted "trades" (Article VII; Ch.3/Ch.7). The $6k/yr + $150k scholarship he stopped (Article XXII; Ch.3/Ch.9). The Bill→Landon/Devin succession that made the Eskew boys beneficiaries on Bill's death (Article XXIII; Ch.4). It is all written, in 2000, in the document John signed.

PETITIONER'S EXHIBITS #8, #9, #10 — 10/18/2000 deed (REC#821185) + JHF Trust pages. 821185

PETITIONER'S EXHIBITS #14, #15 — JHF 2000 Will & Articles of Trust pages: trustee succession (Lewis; then Bill Eskew & Theresa Imhof), no-court/no-account clauses, Article XVI accounting to beneficiaries, Article XXII disposition (scholarship + Bill/Teresa), life-insurance schedule.

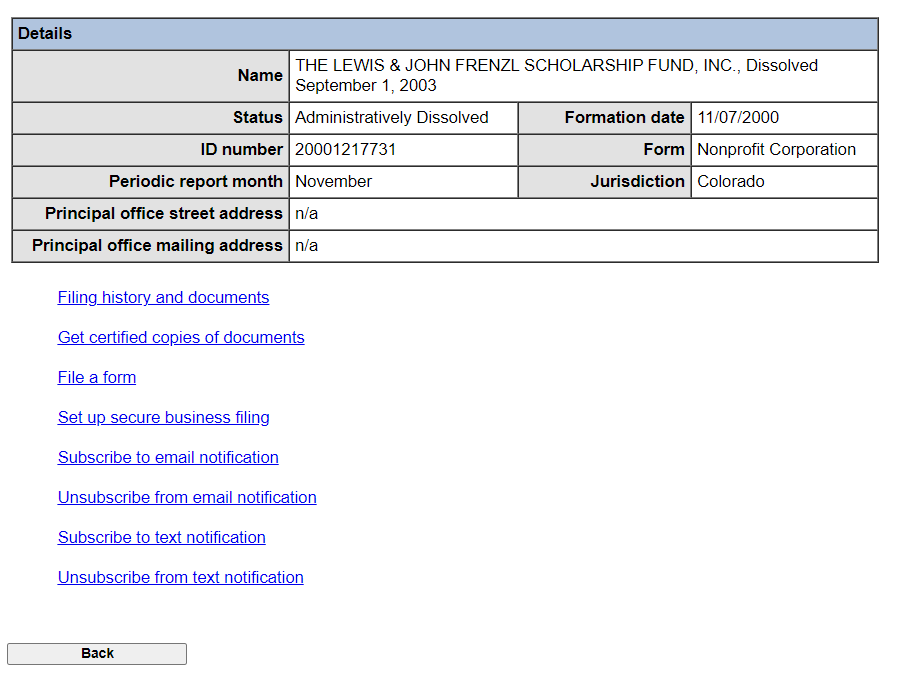

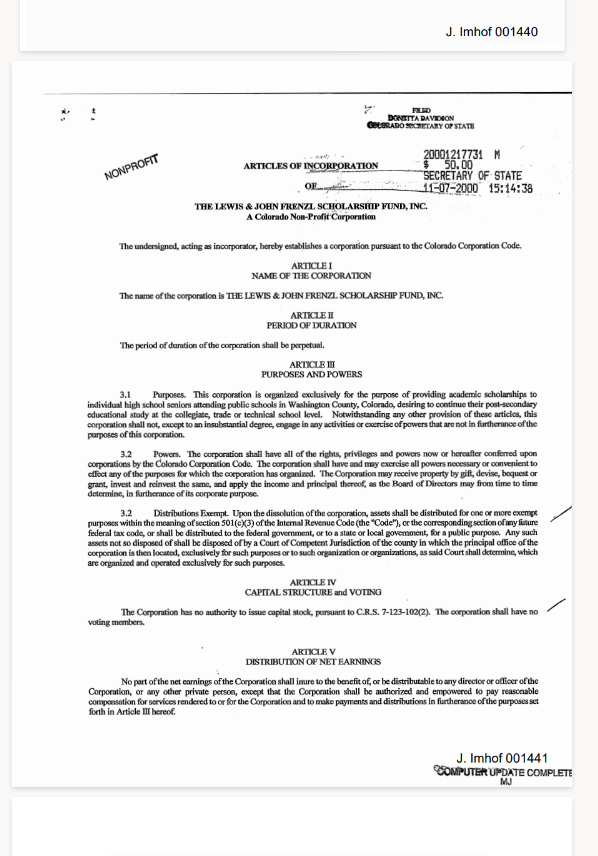

2000–2003 — The Scholarship Fund

The Lewis & John Frenzl Scholarship Fund, Inc. was an ongoing entity (at least 2000–2003), created by the brothers expressly to give back to Washington County high-school seniors pursuing further education — and it is a named beneficiary of the Trust.

9/1/2003 — the Fund is administratively dissolved by the State (a paperwork lapse — two aging farmers not filing annual reports), but it remains a beneficiary of the Trust. Per Kelly Hansen's 5/15/2024 email (#10): the scholarship isn't a current SoS entity; "it appears that Lewis wrote checks from the Trust to fund the scholarship."

Lewis personally funded scholarship checks to five Washington County high schools every year through the last weeks of his life (Ch.2). The administrative dissolution never extinguished the Trust's $6,000/yr and $150,000-at-termination obligations to the Fund — obligations Justin stopped honoring the moment he took over (Ch.3, no 2023 distribution; Ch.9, admitted).

PETITIONER'S EXHIBITS #11, #12 — CO Secretary of State scholarship record (9/1/2003 admin. dissolution) + Hansen Law Response 5/15/2024 (#10).

2003 — Justin's First Land (the Acquisition Pattern Begins)

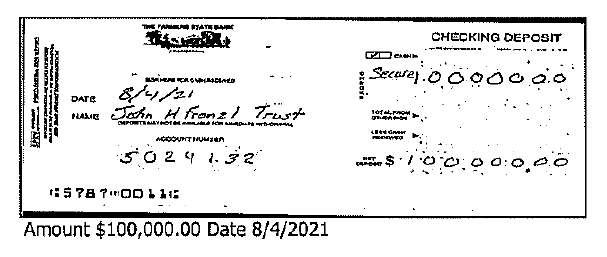

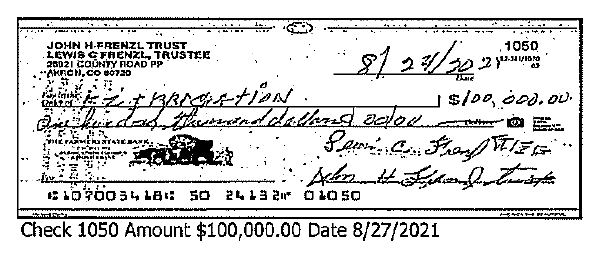

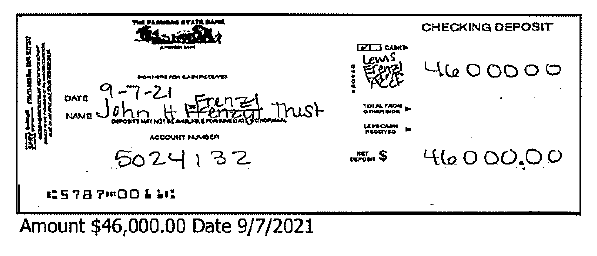

7/25/2003 — YuCo REC#513288, #513289. Justin Imhof purchases 320 acres in Yuma County (NW¼ Sec2, NE¼ Sec3, 5N-48W) from Doris Imhof for $168,000.00 on a twenty-year note. (He retires this note a year early on 12/10/2021 — Ch.2 — the same window he paid the JHF Trust no documented rent.)

7/25/2003 Doris Imhof purchase (REC#513288/513289). 513288 · 513289

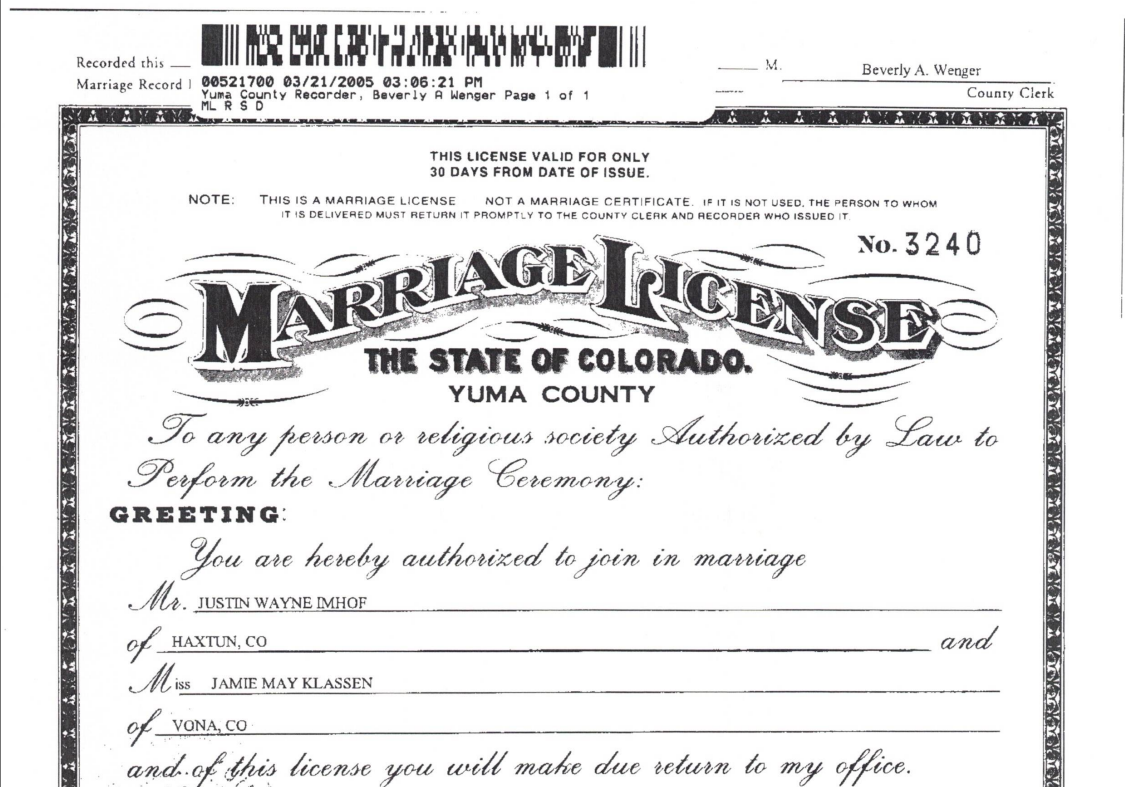

2005 — Justin & Jamie Marry

3/19/2005 — YuCo REC#521700. Justin W. Imhof (Haxtun) marries Jamie M. Klassen (Yuma). (Jamie becomes a shared signatory on Imhof bank documents from 2015 and a co-borrower throughout the later land deals.)

3/19/2005 marriage record (REC#521700). 521700

2012.12.15 — John H. Frenzl Dies; the Trust Becomes Irrevocable

John H. Frenzl passes December 15, 2012. Lewis C. Frenzl becomes Trustee under Article IV. Under Article VII the Trust is now irrevocable — its terms fixed, the beneficiaries' interest paramount, for the ~21-year term ending 2033.

This is the hinge of the entire case. From 12/15/2012 forward: John's half of fifty years of land and equipment sits in an irrevocable trust owed annual accountings (Art. XVI) to beneficiaries Bill Eskew and Teresa Imhof, court-accountable on breach (Art. VI), terminating in 2033 with a $150k scholarship gift and the balance to Bill's and Teresa's issue. Lewis holds it in trust. What Lewis — and then Justin — did with that trust over the next eleven years is the subject of Ch.1 through Ch.10.

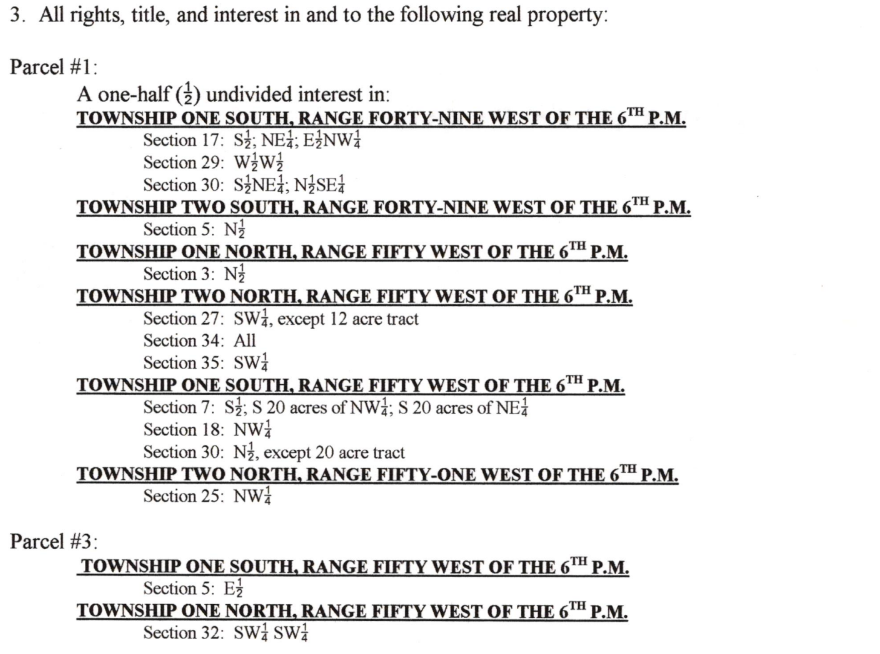

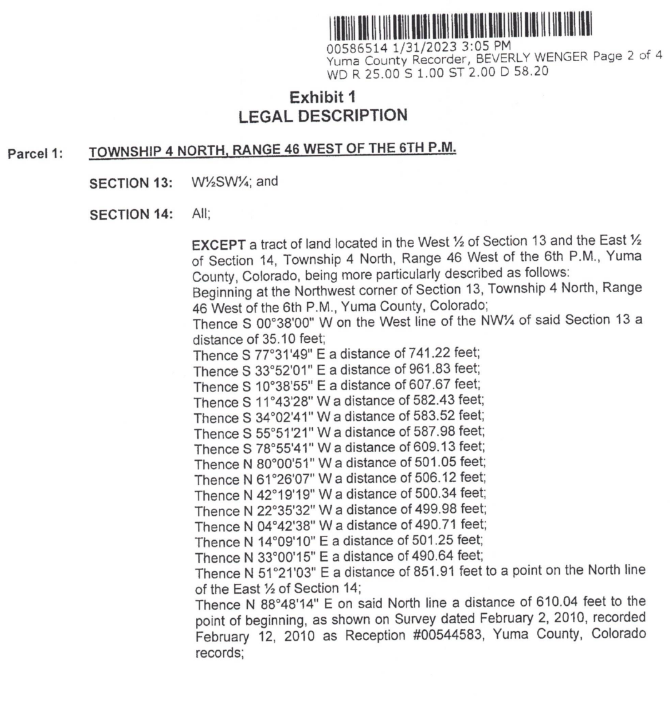

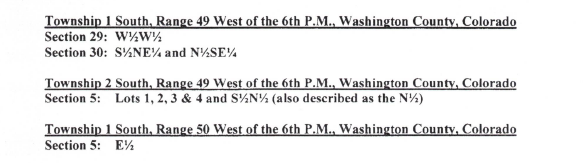

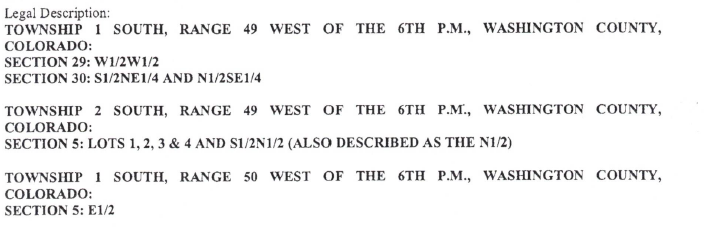

Schedule "A" legal descriptions — Parcel #3, Sec 25 (T2N R51W NW¼), Sec 5, etc. JHF Trust corpus.

9/17/2012 — The Case IH Patriot Sprayer (an Asset That Walks)

9/17/2012 — while John is still alive — a likely 2010–2012 Case IH Patriot sprayer is delivered. That sprayer is later found at Justin's home in 2016. A Schedule A-class asset, half the Trust's, that quietly relocated to the tenant's place.

9/17/2012 Case IH Patriot sprayer delivery; found at Justin's 9/17/2016. !!! Whereabouts/half-interest of the sprayer is a carried-open item through Ch.2's ledgers.

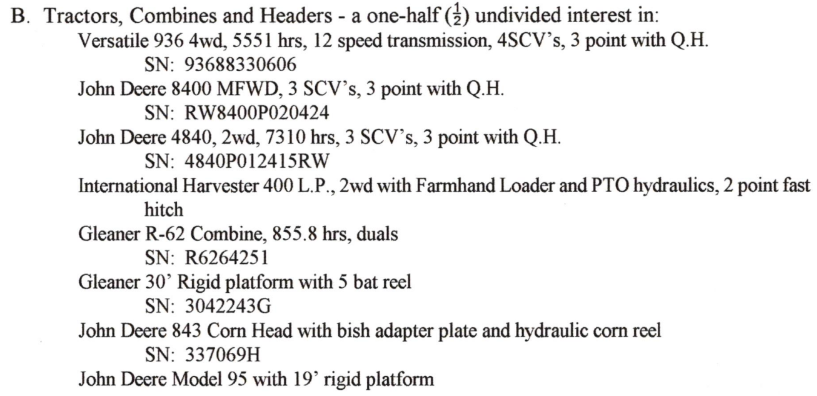

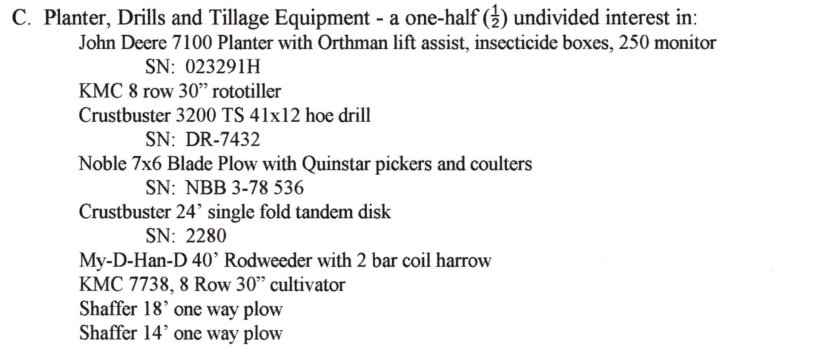

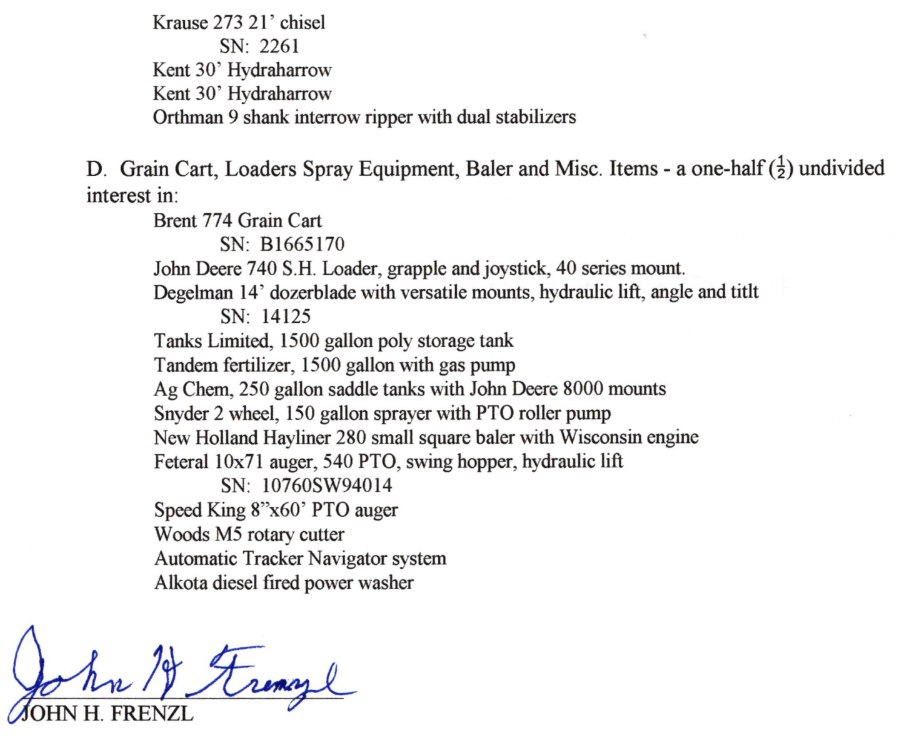

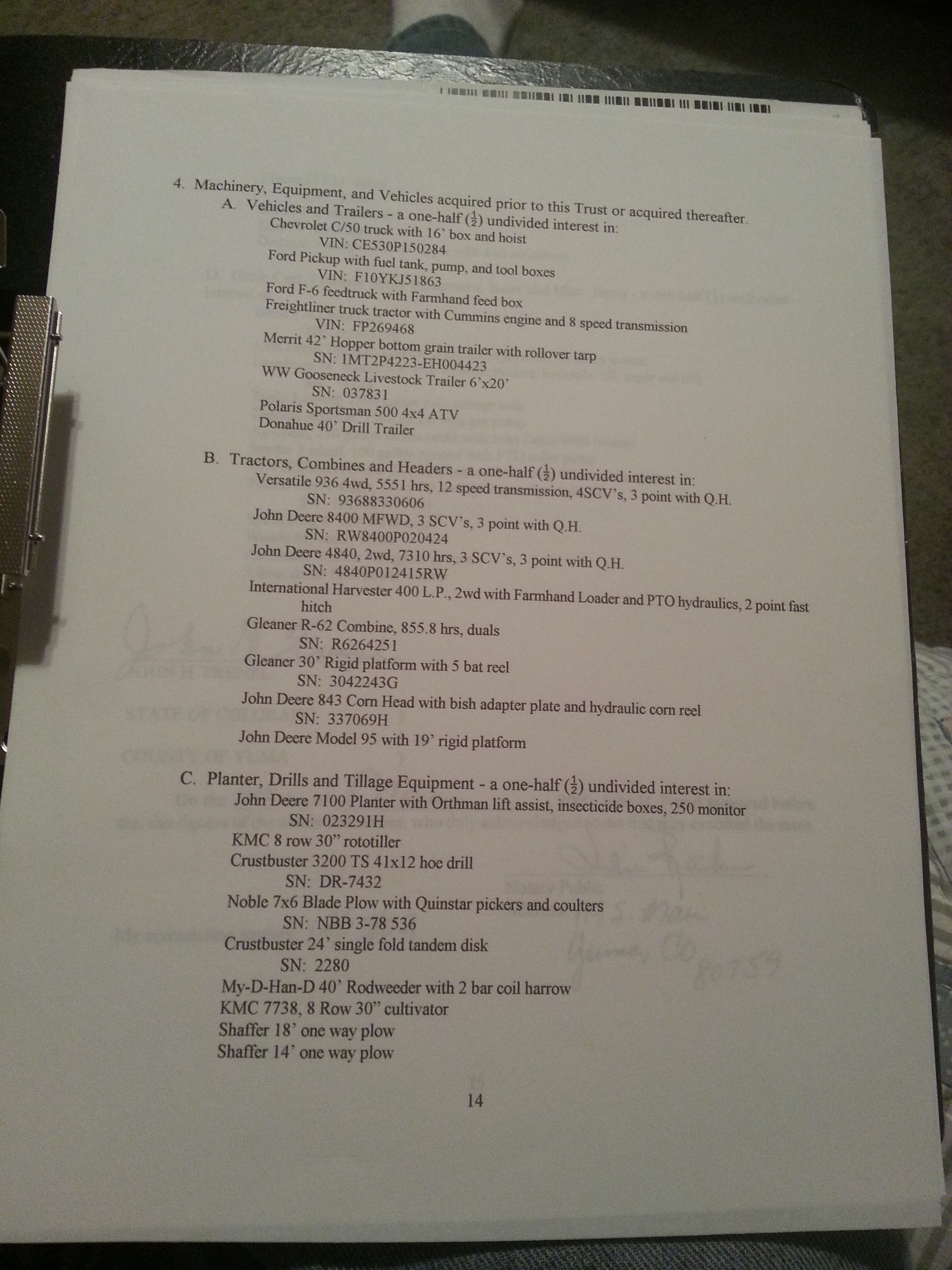

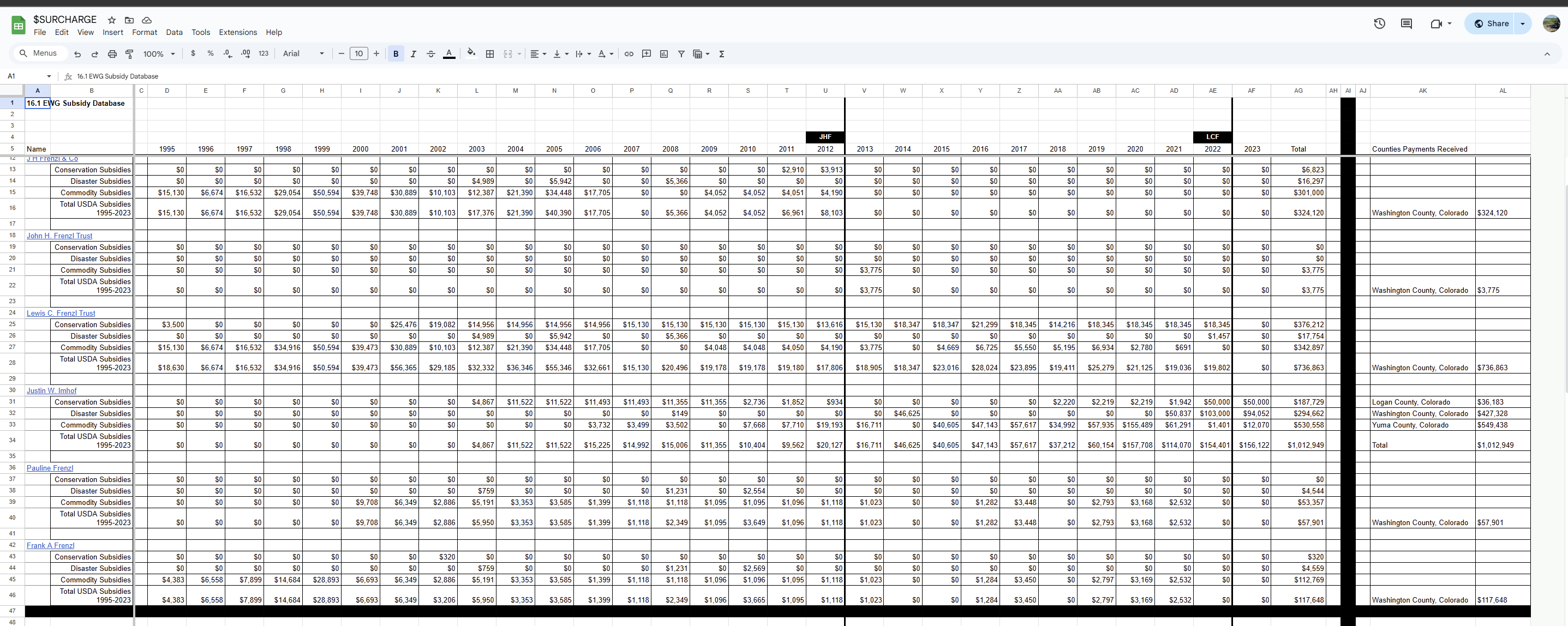

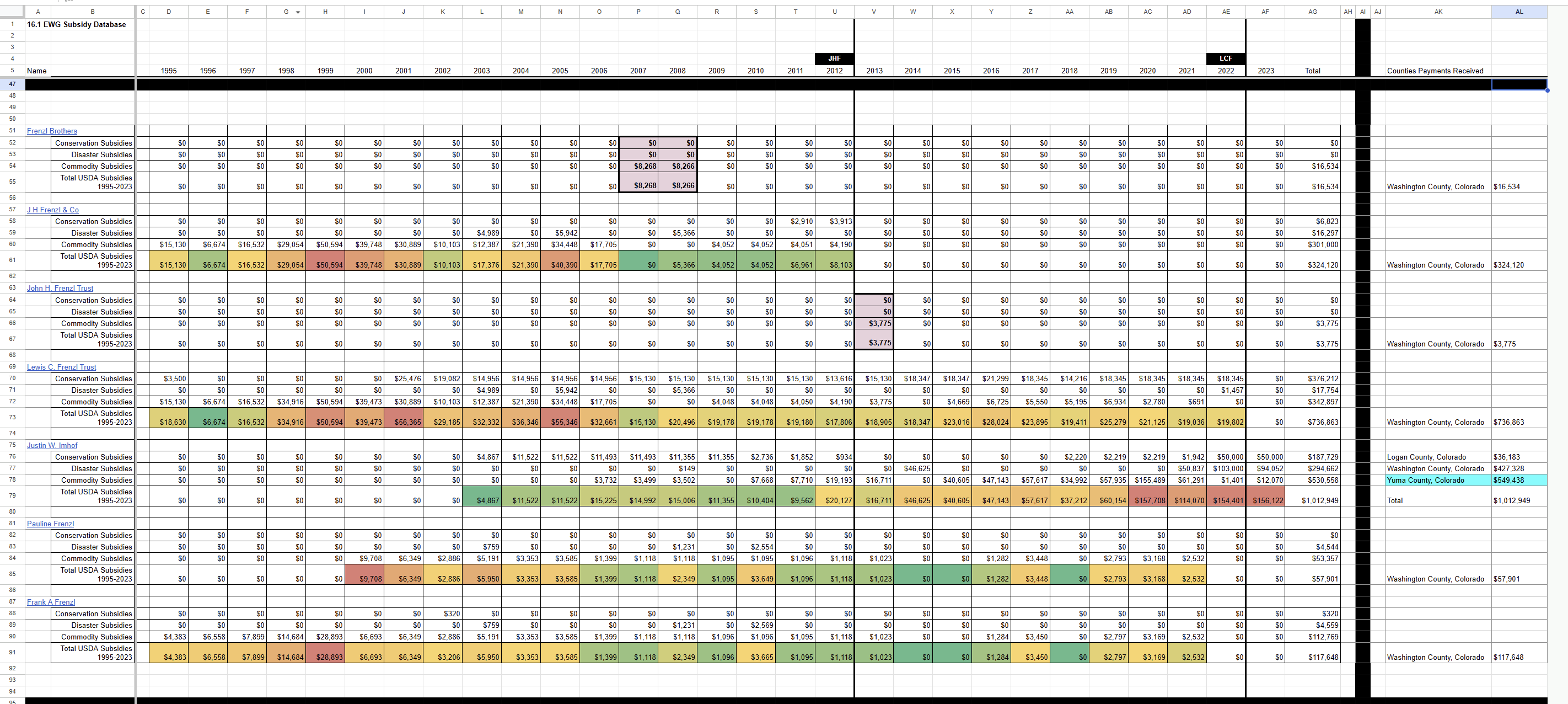

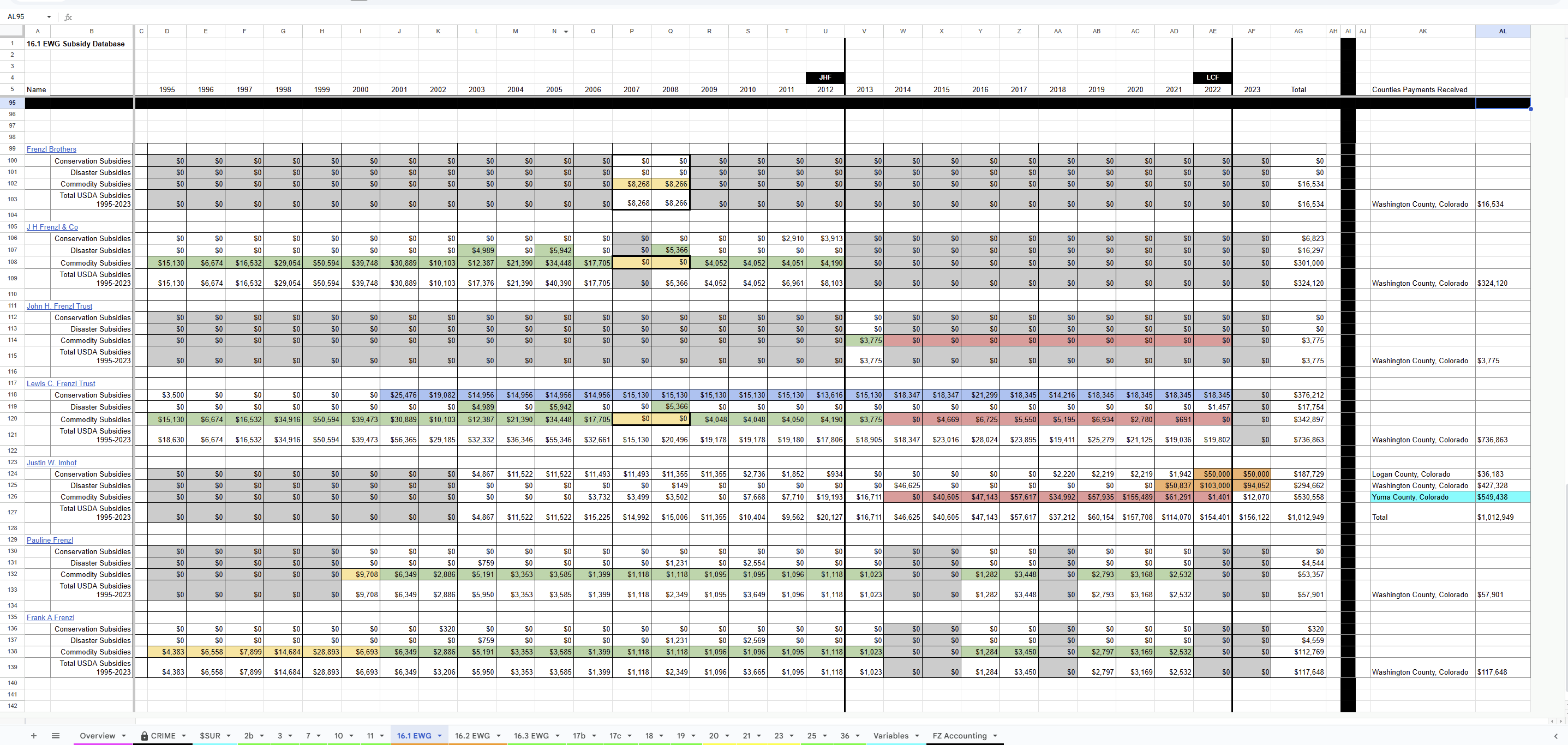

JHF Trust Schedule "A" — The Master Asset List

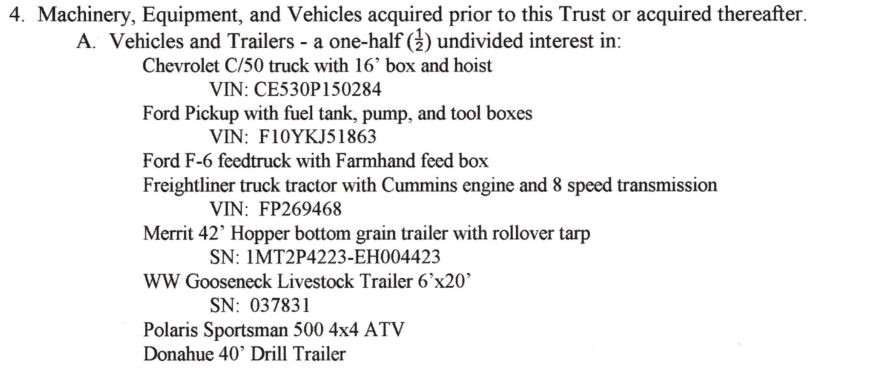

The Trust's corpus (Schedule A) — the list against which every later disposition is measured (the 2013 auction in Ch.1, the BigIron sale in Ch.5, the missing items in Ch.10). Item 4 enumerates a one-half undivided interest in machinery, vehicles, tractors, combines, planters, tillage, grain cart, loaders, and misc. — including the Freightliner truck tractor (VIN …FP269468) and Merritt 42' hopper-bottom grain trailer (SN …EH004423) that resurface in the 2015 title transfers (Ch.2), the 2023 de-insurance (Ch.3), and the 2024 BigIron auction (Ch.5); the Polaris Sportsman 500 Landon photographed in 2015 (Ch.2); the Brent 774 grain cart; and a 1964 Mercury Montclair, 2003 Buick Century, 2013 Ford F-350, and the Case IH Patriot sprayer.

"A one-half undivided interest in" — the words that recur on every line. Schedule A itself states the Trust's interest in the equipment as one-half — the documentary proof that John and Lewis owned the operating equipment 50/50, regardless of which brother's name a title carried. This is the foundation of the "homestead/equipment assets are half John's" theory that Krening confirms under oath in Ch.7. The 1964 Mercury Montclair is the specific missing-asset Landon flags to the successor trustee in Ch.10.

JHF Trust Schedule "A" asset pages (one-half undivided interests). Master list for the auction/BigIron/missing-asset analyses (Ch.1, Ch.5, Ch.10).

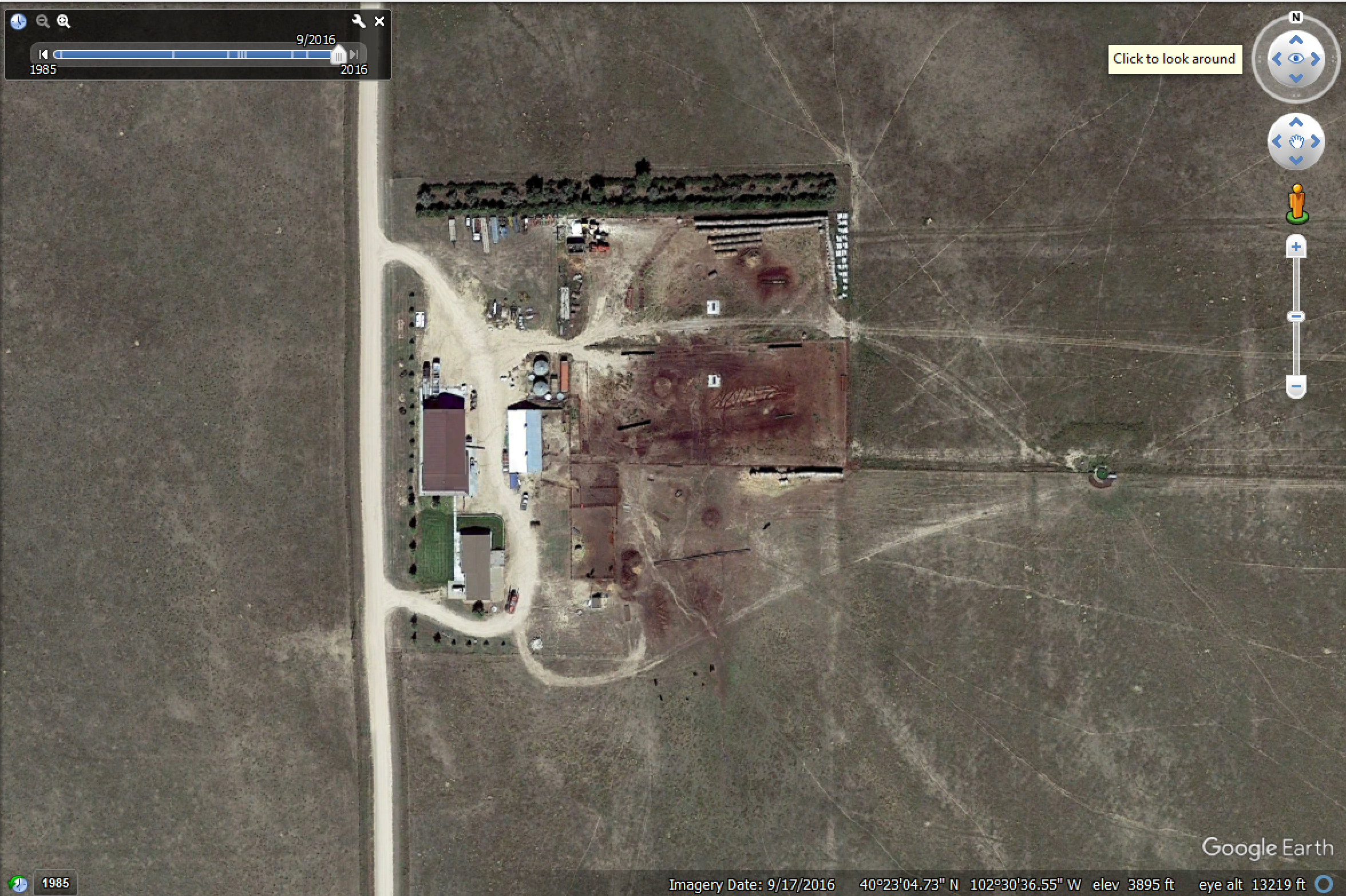

Earth-View of Assets — Aerial Baseline

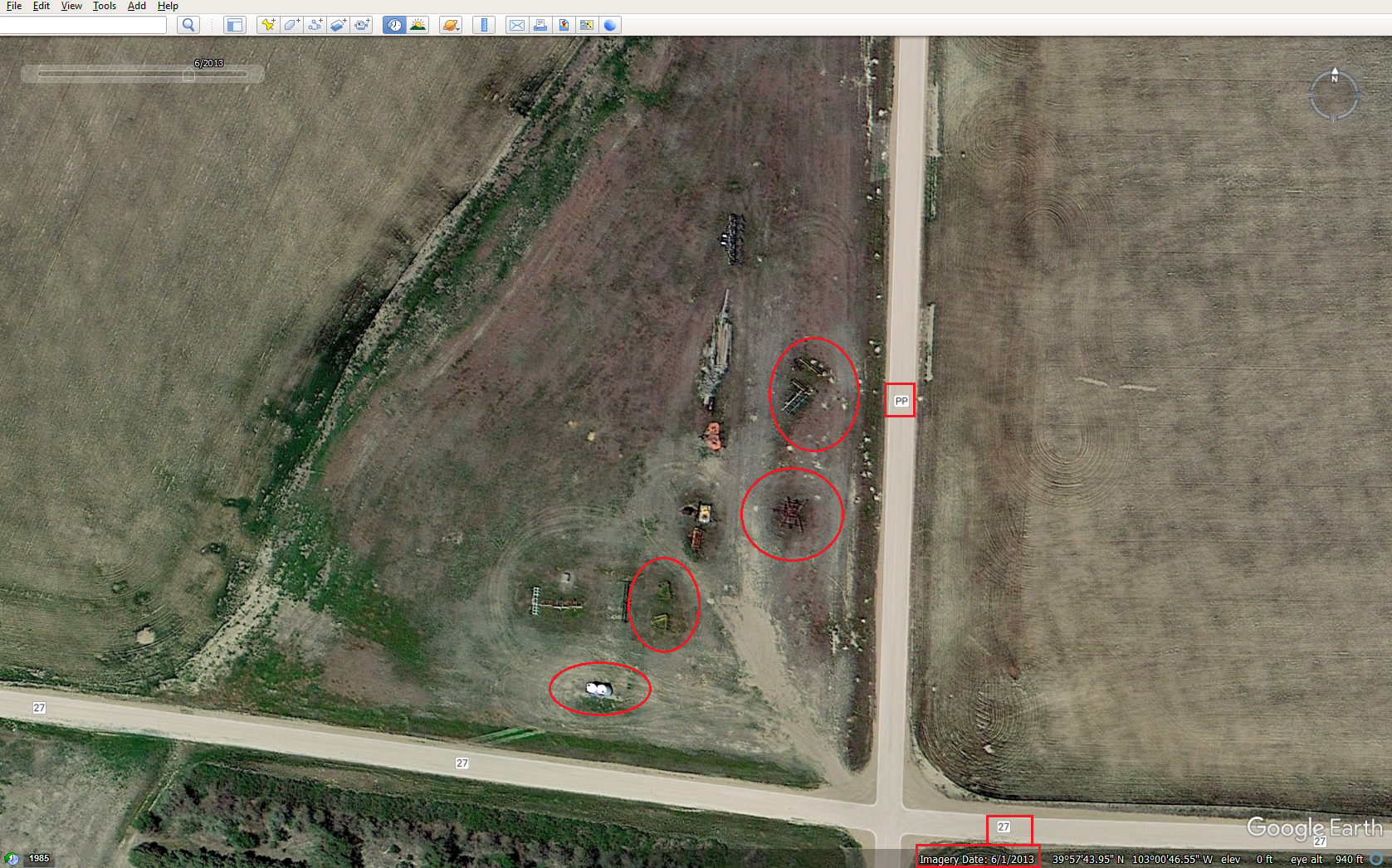

Dated aerial captures establishing the land/improvement baseline before the changes: Homestead (HS) and Yuma-area (YA) views for 2012, 2013, and 2016, plus the Justin-Imhof (JWI) acquisitions in 2016.

Earth-view aerial set (captured 10/14/2024): HS A 2012/2013/2016, YA 2012/2013/2016, JWI A 2016. !!! These are the aerial filenames previously flagged as "unresolved to vault paths" — now resolved to Ch0_image059–067. Pair with the Frenzl.kmz/Frenzl.geojson capture checklist (Ch.2 intro) for a dated before/after set.

Open Foundational Items

- JHF Estate mineral rights: ~427 acres of minerals calculated under JHF's personal name; 427 ac × $25/ac = $10,675.00 (even at half, value Justin intended to keep in the land sale). (Ties to the "no mineral rights" denial Ch.4/Ch.6 and the minerals Justin reserved to himself in Ch.3 conveyances.)

- JHF Estate credits owed: Nebraska Highways $100.00 (and a smaller one) — payments owed back to the JHF Estate. !!! Itemize on the next pass.

Reading Forward → Ch.1

Ch.1 — The Watch (2012.12.15 – 2015.03.13) — opens the day after John's death, with Lewis as Trustee of a now-irrevocable trust. It is the period in which the first cracks appear: the suspiciously small 2012 tax return, the 2013 equipment auction whose proceeds the Trust never received, and Justin's first self-drafted farm leases (backdated to 1/1/2013, terms degrading) — the opening moves of everything that follows.

Production Notes (this draft)

- ⏯ Awaiting Landon's factual verification + caption confirmation. All 67 images placed inline via hash-matched MHT map (

AI/ops/temp/ch0_image_map.txt). - Dollar amounts backslash-escaped throughout (was a flagged inconsistency; now fixed).

- Image notes: the 1976 partnership pages (008–017), the 2000 trust pages (034–048), Schedule A (050–053), and the aerials (059–067) are placed in document order; confirm individual page↔exhibit pairings on review.

- !!! Open / flagged:

- Case IH Patriot sprayer half-interest — carried open

- JHF mineral acreage (~427 ac) and estate credits — verify and itemize

- Aerial set (059–067) — re-pull dated Google Earth captures to match the Frenzl.kmz checklist

- Several REC# wiki-links (698556, 712179, 738837, 813624, 821185, 513288/289, 521700) — confirm the linked instruments exist in the vault

Ch.1 — The Watch (2012-12-15 – 2015-03-13)

Status: Narrative draft v2 (2026-06-13) — upgraded to chapter-consistent format: intro, analysis, inline images (hash-matched via

ch1_image_map.txt), escaped dollar amounts, forward-links. Awaits Landon's factual verification + caption confirmation. Source:_INCOMING/2026.05.16 BarFZ OneNote/exported/Ch.1 2012.12.15-2015.03.13.mhtFrame note: Lewis is now Trustee of John's irrevocable trust. This is the short window where the first cracks appear — a poverty-line tax return, an equipment auction the Trust never banked, and Justin's first self-drafted, backdated, degrading farm leases. The machinery of Ch.2–Ch.10 is assembled here.

INTRO — Lewis Holds the Trust; Justin Starts Drafting

Chapter 1 covers the twenty-seven months between John Frenzl's death and the day Lewis revoked his own trust — the period Lewis stood watch over his brother's irrevocable trust, and the period Justin Imhof began quietly writing himself into it.

When John died on December 15, 2012, the John H. Frenzl Trust became irrevocable with Lewis as Trustee, owing annual accountings to its beneficiaries (Ch.0, Article XVI). On the surface this is a quiet stretch — tax filings, lease paperwork, routine farm administration. Underneath, three patterns that drive the entire case are established:

- The Trust's income vanishes on paper. The 2012 return reports $10,150 of income on a half-interest in ~5,000 acres — a poverty-line number for a working farm — and the trajectory only worsens.

- The 2013 equipment auction never reaches the Trust as cash. Proceeds go to Lewis's personal account; the Trust's half is booked as a depreciable asset and then written off — not received as income.

- Justin drafts his own leases. The first Farm Lease (9/11/2013) and a second, better-for-Justin lease (1/28/2014) are both backdated to 1/1/2013, drafted without independent counsel, with terms that strip the Trust's income and load it with 100% of the infrastructure costs — the template extended in Ch.2's third lease (2017).

Family voice We named this "The Watch" because Lewis was supposed to be the watchman over his brother's half — and for a while he was the only thing standing between the trust and the people circling it. But this is also where, reading backward, you can see the hand that drafted the leases wasn't Lewis's. An 80-year-old farmer didn't write a lease that deleted his own trust's crop-share protections and kept it paying every irrigation bill. Justin did. The watch was already being compromised; Lewis just didn't know by how much.

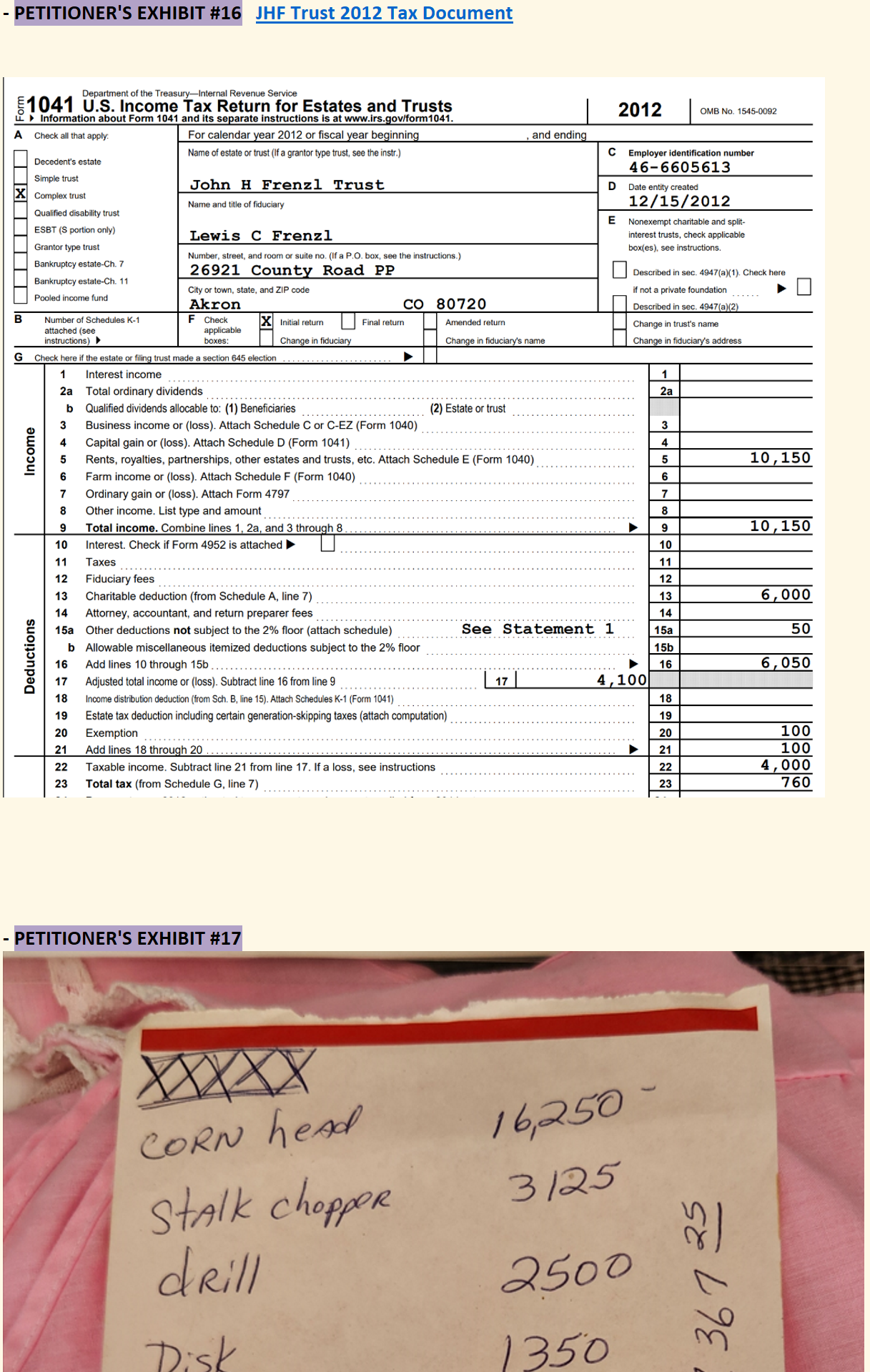

2013.03.23 — The 2012 Return: A Poverty-Line Trust

The prior year's (2012) JHF Trust taxes are filed after John's death. The Trust reports $10,150.00 on Schedule E from the Frenzl partnership; $4,000.00 reaches taxable income; $760.00 in tax is paid.

No explanation has ever been produced for why a half-interest in roughly five thousand acres of active farm and ranch land generated $10,150 in income — 65% below the federal poverty line for the year (Ch.7, Krening deposition prep returns to this exact number). It is the first of the "where did the money go" questions, and it sits at the very start of the trust's life.

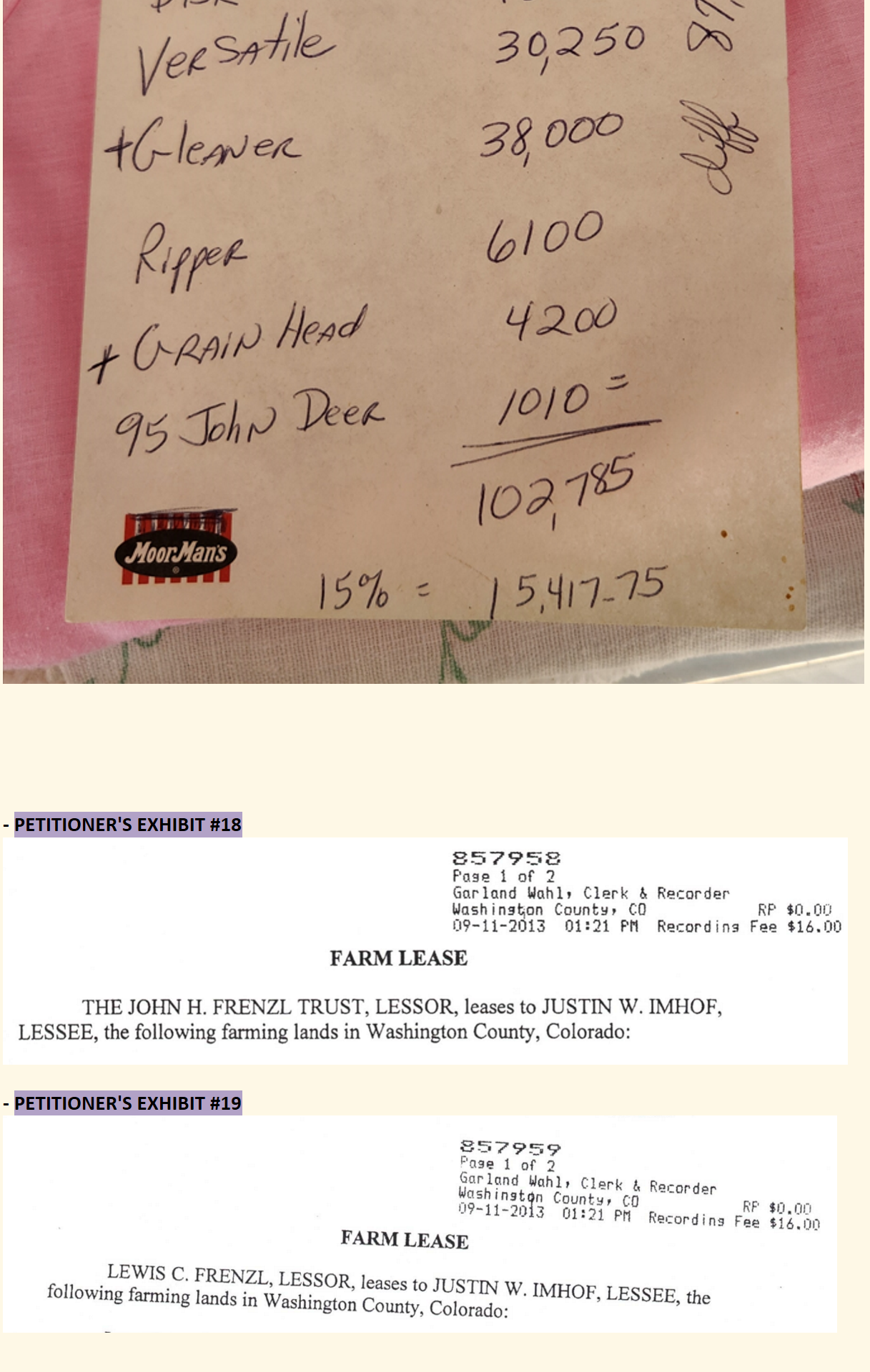

2013 — The Equipment Auction the Trust Never Banked

Johnnie Eskew can attest he attended a 2013 BigIron equipment auction of some Schedule "A" assets. His contemporaneous hand-written list:

| 2013 auction (Johnnie's list) | Amount |

|---|---|

| Total sales | $102,785.00 |

| Auctioneer's 15% cut | −$15,417.75 |

| Net proceeds to Frenzl's | $87,367.25 |

| Half (the JHF Trust's share) | $43,683.50 |

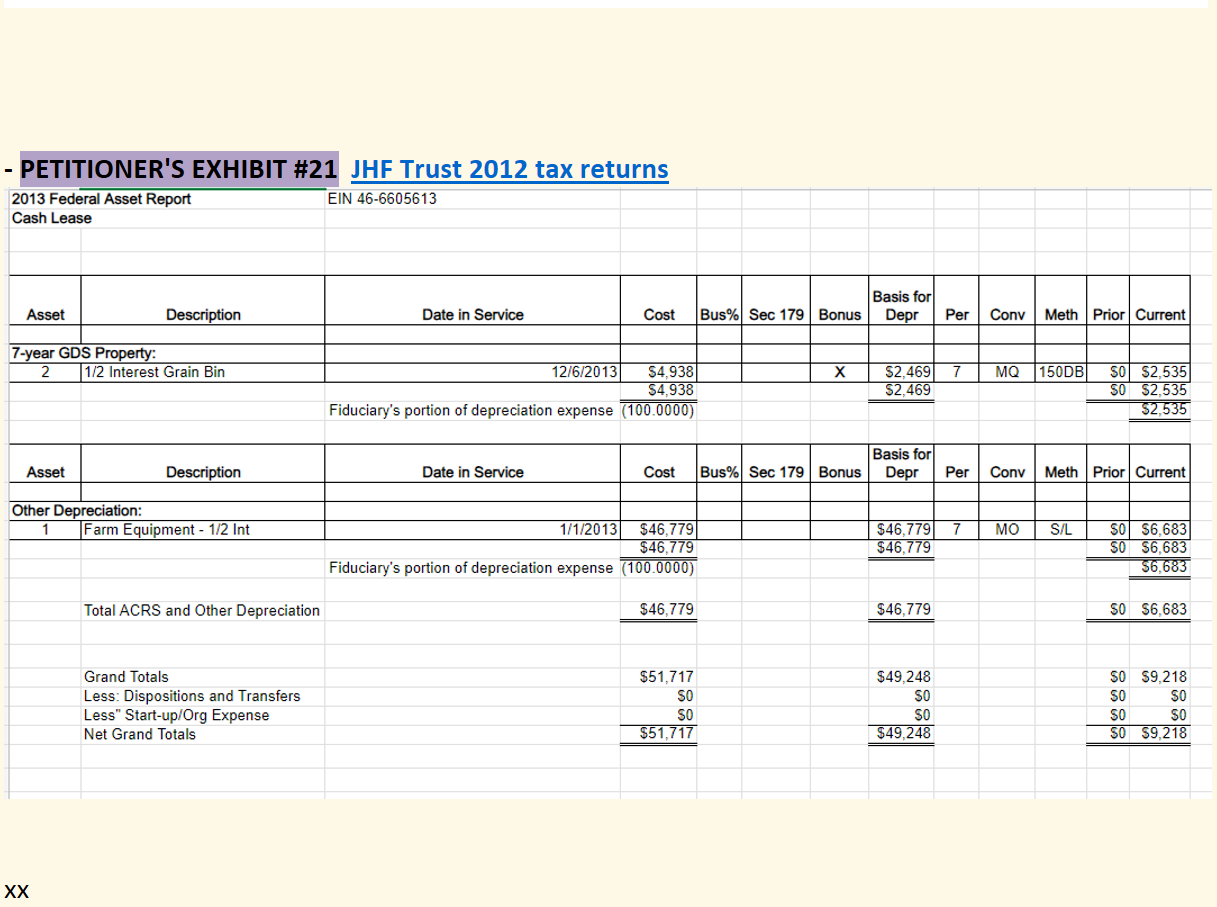

The JHF Trust tax returns instead show 'Farm Equipment – 1/2 Int' booked as an asset for $46,779.00 (the difference likely the preparer using the auctioneer's final invoice vs. Johnnie's partial list).

The auction-income sleight, established here and confirmed under oath later. The auctioneer would have mailed the check to Lewis, who deposited it to his personal account and told his accountant to write half to the Trust. But cash gains on auction sales are income, not assets. Booking the proceeds as a depreciable asset — and then, in the April 2015 filing of 2014 taxes, writing that asset off via IRS Form 4797 ("Sold/Scrapped 1/09/14") — converted real cash the Trust was owed into a paper entry that simply disappeared. (Krening confirms each step of this in Ch.7; the assets that weren't actually scrapped resurface at the BigIron auction in Ch.5.)

PETITIONER'S EXHIBITS #17, #18, #19 — 2013 auction / equipment-disposition documentation; Johnnie Eskew's hand-written tally.

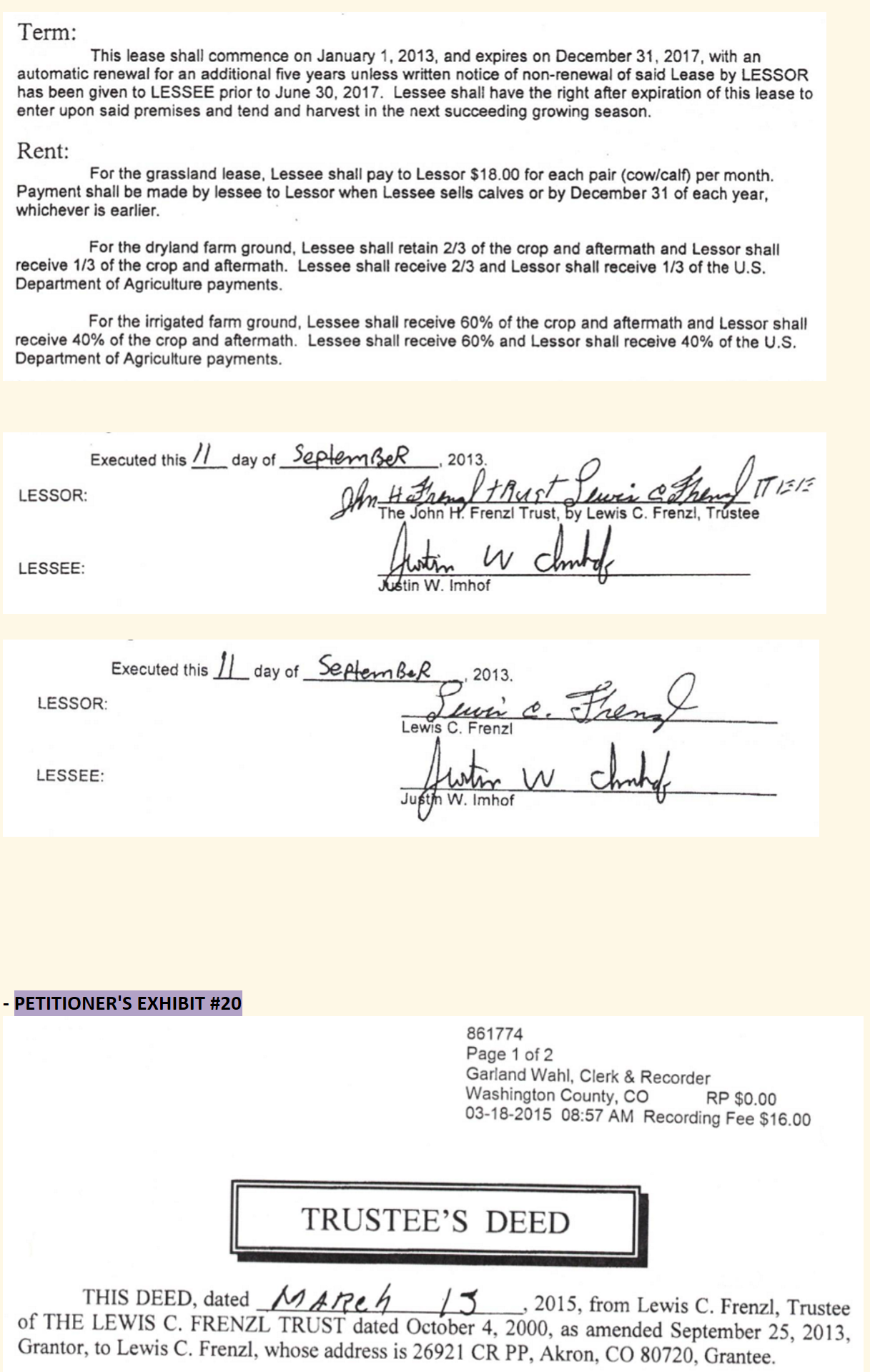

2013.09.11 — The First Farm Leases (Self-Drafted, Backdated)

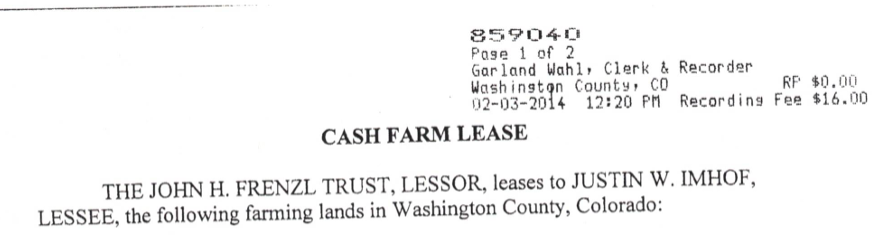

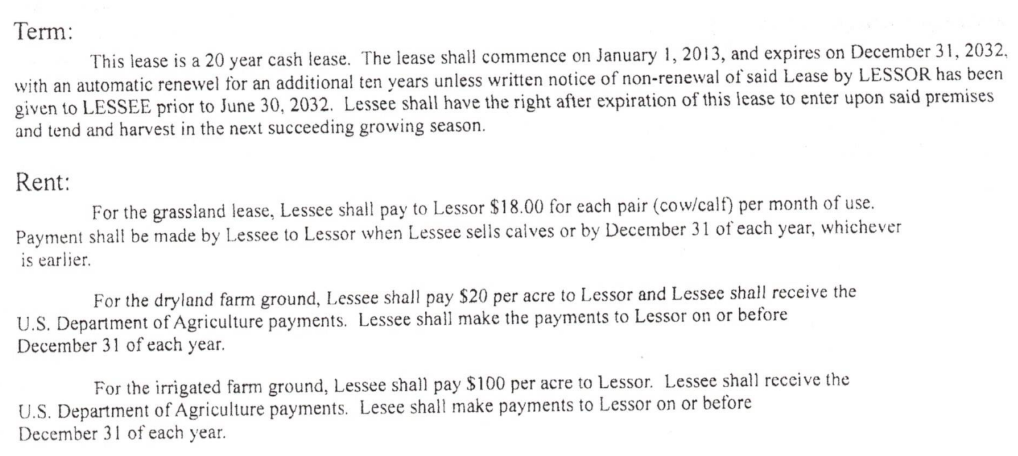

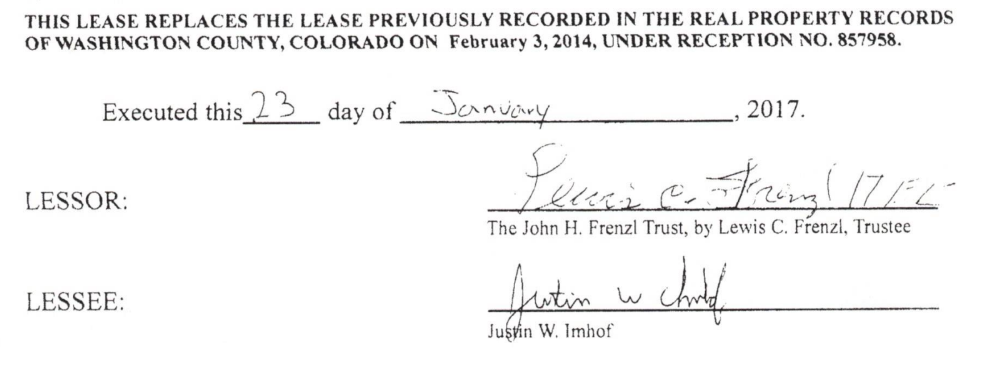

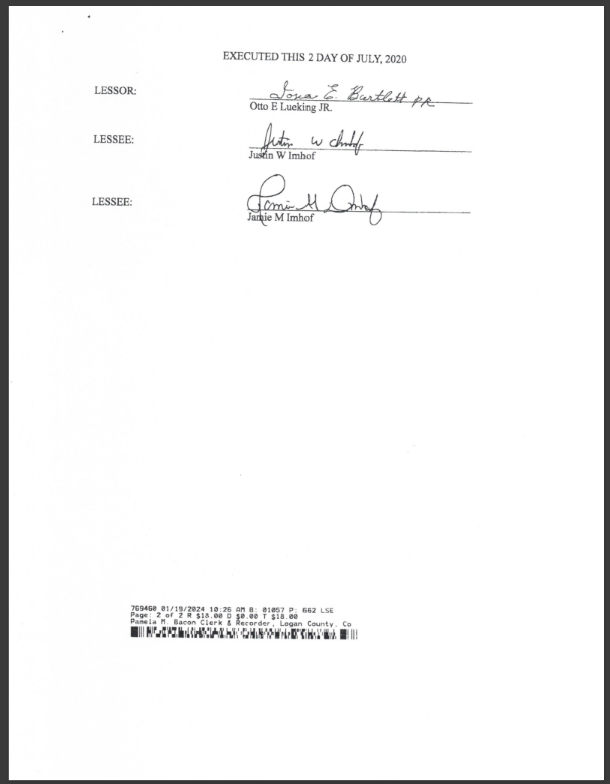

WaCo REC#857958, #857959. Justin Imhof creates and executes two Farm Leases — one between Lewis Frenzl and himself, one between the JHF Trust and himself — for 100% of Frenzl's Washington County land (less 40 acres to Brian Kuntz). Two documents because two entities own the ground separately (50% Lewis's trust, 50% John's now-irrevocable trust). The Cash Farm Lease is backdated to 1/1/2013 — two weeks after John's death — a five-year term with automatic five-year renewal. Rent: Grassland $18/mo per cow/calf pair; Non-irrigated 2/3–1/3 split (USDA pro-rata); Irrigated 60/40 split (USDA pro-rata).

Justin — not Lewis, not an attorney — drafted the leases on both sides of the table. He authored the agreement under which he was the tenant, for land the Trust's beneficiaries depended on for income, with no independent counsel reviewing the Trust's side. The backdating to 1/1/2013 is the first instance of a pattern that repeats on every lease through 2024 (Ch.2's third lease, Ch.3/Ch.4's Lueking and Condon leases).

PETITIONER'S EXHIBIT #22 — first Farm Lease set (REC#857958/857959), backdated 1/1/2013. 857958 · 857959

2013.09.25 — LCF Trust Already Being Amended

WaCo REC#861774. Two weeks after the backdated lease, Lewis Frenzl's substantially-identical 2000 trust has already been partially amended — the first sign of the reworking that culminates in Lewis's full revocation on 3/13/2015 (Ch.2's opening). (The September 2013 amendments are formally recorded/acknowledged in 2015 — Ch.2.)

2013.12.06 — Homestead Asset Booked Half to John's Trust

The 2012/2013 JHF Trust returns put a 'Grain Bin' into service for a ½ interest of $4,938.00 (implied full value $9,876.00).

This is the homestead-half theory in its first instance. A grain bin on the homestead (titled to Lewis) is booked as half the JHF Trust's asset — documentary proof that Lewis himself treated homestead improvements as 50% John's. Krening confirms exactly this inference under oath in Ch.7, and it recurs with the Powerlift Doors and the new grain bin below.

2013.12.31 — Cumulative Breach Ledger (opening)

As of December 31, 2013:

- ☐ No proof the JHF Trust received a 50% split of any equipment-auction proceeds

- ☐ No proof of Justin's lease payment for the 2013 season

- ☐ No proof of the initial $150,000.00 contribution to the Scholarship Fund

2014 — The Second Lease, the Real Tax Picture, and the Acquisitions Begin

2014.01.28 — Second Farm Lease (Better for Justin)

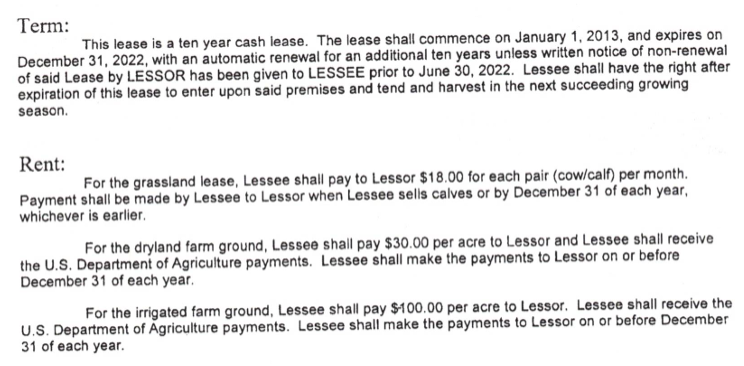

WaCo REC#859040. Just 139 days after the first lease, a second JHF Trust Farm Lease is drafted with terms more favorable to Justin, signed by Lewis as Trustee, still backdated to 1/1/2013 — now a ten-year term with automatic ten-year renewal. The side-by-side degradation:

| Term | First lease (REC#857958) | Second lease (REC#859040) |

|---|---|---|

| Term & renewal | 5 yr + 5 yr | 10 yr + 10 yr |

| Grassland | $18/mo/pair | $18/mo/pair ✅ |

| Non-irrigated | 2/3–1/3 split + USDA pro-rata | $30 flat/acre, Justin keeps 100% USDA ❌ |

| Irrigated | 60/40 split + USDA pro-rata | $100 flat/acre, Justin keeps 100% USDA ❌ |

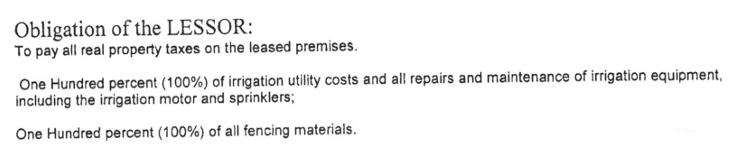

It also strips the Trust's protections — deleting Justin's obligations to transport the Trust's crops, comply with acreage/government programs, split fertilizer/herbicide/pesticide/seed costs (dryland and irrigated), the mutual crop-sale settlement and segregation obligations, and the insurable-interest clause — while leaving the Trust paying 100% of fencing materials and all irrigation utilities, repairs, maintenance, motors, and sprinklers.

Landon and Devin pulled every Washington County farm lease for the prior twenty years and found the customary, overwhelming default is a 2/3–1/3 split — establishing that the Frenzl leases ran sharply below market, in Justin's favor, by design.

PETITIONER'S EXHIBIT #23 — second Farm Lease (REC#859040): $100/acre irrigated, Trust pays 100% of irrigation equipment/motors/sprinklers. 859040

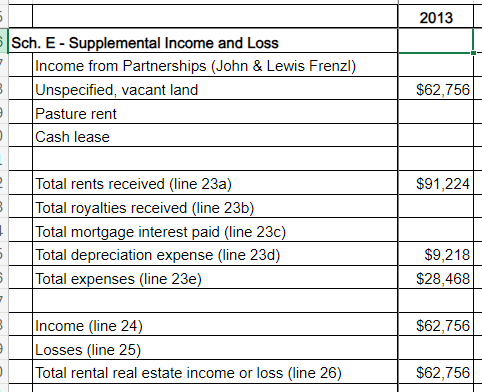

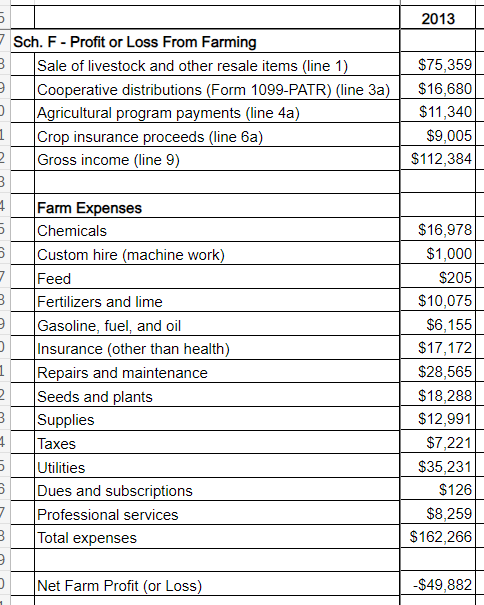

2014.04 — The 2013 Return: What an Honest Year Looked Like

The 2013 JHF Trust return (filed April 2014) — the one full, operating-entity snapshot:

| 2013 (filed 4/2014) | Amount |

|---|---|

| Schedule E rents received | $91,224 |

| Schedule E expenses | −$28,468 |

| Net rents | $62,756 |

| Sch F livestock sales* | $75,359 |

| Sch F co-op distributions | $16,680 |

| Sch F ag-program payments | $11,340 |

| Sch F crop insurance | $9,005 |

| Sch F expenses | −$162,266 |

| Net farm loss | −$49,882 |

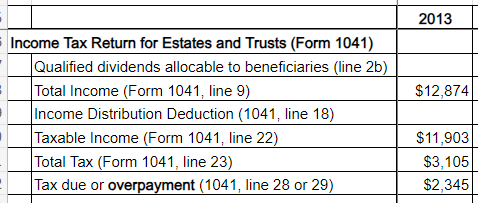

| Total income (1041) | $12,874 |

\On 5/15/2024 Kelly Hansen stated no cattle were ever held by the Trust — yet the Trust's own 2013 return reports $75,359 in livestock sales.*

PETITIONER'S EXHIBIT #24 — 2013 JHF Trust return detail (Schedule E rents, Schedule F farm activity, Form 1041).

2014.03.19 & 10.15 — More Homestead/Joint Assets Booked Half to John's Trust

- 3/19/2014 — 'Powerlift Doors – ½ Int' into service, ½ interest $12,539.00 (implied full $25,078.00). The Quonset doors are on the homestead — booked half to John's Trust.

- 10/15/2014 — 'Remainder of Grain Bin – ½ Int' into service, ½ interest $56,049.00 (implied full $112,098.00). A new grain bin on the sandhills irrigation ground (N½ Sec5-T2S-49W per Google Earth, added June 2013–March 2016) — again booked 50/50.

Three assets in two years — grain bin, powerlift doors, new grain bin — all booked as half the JHF Trust's, all on land or homestead titled to Lewis. The tax record keeps proving the 50/50 reality the brothers always lived by (Ch.0), even as the lease income to the Trust is being engineered downward.

2014.06.02 — Justin & Jamie Buy Their Home

YuCo REC#560598–#560600, #560961. Justin and Jamie purchase their home (SW¼ Sec21, T5N R46W) for $217,500.00 — 10% down, balance financed by Northstar Bank of Colorado — with a first right of refusal on the rest of the quarter-section from Dennis Salvador. (The Salvador relationship and NSBC financing recur in Ch.2's 2015 and 2020 acquisitions.)

6/2/2014 Imhof home purchase (REC#560598–560600, 560961). 560598 · 560599 · 560600 · 560961

2014.12.18 — 2014 Taxes Filed Early (Before the Year Closed)

Melanie Krening completes the 2014 JHF Trust taxes on 12/18/2014 — before the tax year was even over — the filing that writes off the equipment via Form 4797 (above).

2014.12.31 — Cumulative Breach Ledger

As of December 31, 2014:

- ☐ No proof of a 50% equipment-sale split to the Trust

- ☐ No proof of Justin's lease payment for 2013 or 2014

- ☐ No proof of the initial $150,000.00 Scholarship Fund contribution

Washington County lease survey (20 years) — 2/3–1/3 split is the customary default; the Frenzl leases run below market.

Reading Forward → Ch.2

Ch.2 — The Long Drift (2015.03.13 – 2023.01.14) — opens with the act this chapter has been foreshadowing: on March 13, 2015, Lewis fully revokes his own trust and deeds its property back into his name, trading the protective reciprocal structure for an estate controlled by whoever holds the PR appointment. Seven months later a new Will names Justin sole beneficiary. The leases drafted here get a third, twenty-year iteration; the homestead and Section 17 get mortgaged; and the long drift of JHF Trust equity toward the Imhofs begins in earnest.

Production Notes (this draft)

- ⏯ Awaiting Landon's factual verification + caption confirmation. All 15 images placed inline via hash-matched MHT map (

AI/ops/temp/ch1_image_map.txt). - Dollar amounts backslash-escaped throughout (was a flagged inconsistency; now fixed).

- !!! Open / flagged:

- "Melanie Arnold" in the prior draft = Melanie Krening (confirm name; she is the Frenzls' lifelong accountant per Ch.7) — corrected here to Krening

- Lease exhibit pairings (#22/#23/#24) — confirm page↔image matches

- The 9/25/2013 LCF amendment (REC#861774) connects to Ch.2's 3/13/2015 revocation/recording — verify the amendment vs. recording dates

- REC# wiki-links (857958/859, 859040, 560598–560961) — confirm linked instruments exist in the vault

Ch.2 — The Long Drift (2015-03-13 – 2023-01-14)

Status: Narrative draft v2 — analytical pass now runs the full chapter (2015.03.13 → death). Landon's line-by-line factual review is signed off through 2021.12.31; 2022.01.01 → 2023.01.14 has the analysis layer applied (2026.06.13) but still awaits Landon's factual verification. Verify the 2022 facts before this section goes to HTML/court record. Source:

_INCOMING/2026.05.16 BarFZ OneNote/exported/Ch.2 2015.03.13-2023.01.14.mht+SORT_extraction.md+ recorded-instrument OCR pass (2026.06.12) Image note: Asset numbering ≠ MHT part numbering. The OneNote extractor renumbered after image020 and skipped seven JPGs entirely; those were recovered 2026.06.12 asCh2_image118–124.

INTRO

Chapter 2 opens on March 13, 2015 for a precise reason: that is the day Lewis Frenzl's trust quietly becomes an estate.

On that date Lewis executed a full Revocation of "The Lewis C. Frenzl Trust" — the reciprocal trust instrument he and his brother John had signed on the same day, October 4, 2000 — and directed the Trustee to "turn over and deliver to me all property held by you subject to the terms and provisions of the Trust Agreement, together with all accumulations of interest and income." The LCF Trust was not amended. It was not partially restructured. It was fully revoked and fully transferred back into Lewis's individual name. From March 13, 2015 forward, everything Lewis owned would pass not through the protective reciprocal trust structure the brothers built together, but through whatever testamentary instrument was put in front of him next — which arrived seven months later, on October 13, 2015, in the form of a new Will naming Justin W. Imhof as the recipient of effectively everything.

Devin's note This chapter must denote that the LCF Trust was also FULLY transferred — and that it was Lewis's own hand that penned these changes, despite coercion. The Revocation is signed by Lewis C. Frenzl personally and notarized (John Curt Penny, Notary, 3/13/2015). The hand on the pen was Lewis's. The architecture, the timing, and the sole beneficiary of every change were not.

The chapter then runs while this new instrument was in place, all the way through January 14, 2023 — the day of Lewis Frenzl's death. These eight years are the densest documented period of breach activity in the case. The operative instruments are recorded liens, renegotiated lease terms, bank account transfers, tax filings, and UCC records. Read together, they show a systematic transfer of JHF Trust equity toward Justin and Jamie Imhof, executed incrementally through legal instruments that each, in isolation, could be characterized as routine estate administration — but in sequence form a coherent extraction.

Key structural events of this chapter:

- 2015: Lewis fully revokes the LCF Trust and deeds its property back into his own name; mortgages JHF Trust land to fund JWI's personal real estate purchase; executes a new Will naming JWI as sole beneficiary

- 2016: JWI and TJI placed as signatories on the JHF Trust bank account; the account is cleared the same week

- 2017: Third Farm Lease further degrades JHF Trust rental terms; document errors indicate JWI prepared it without attorney review

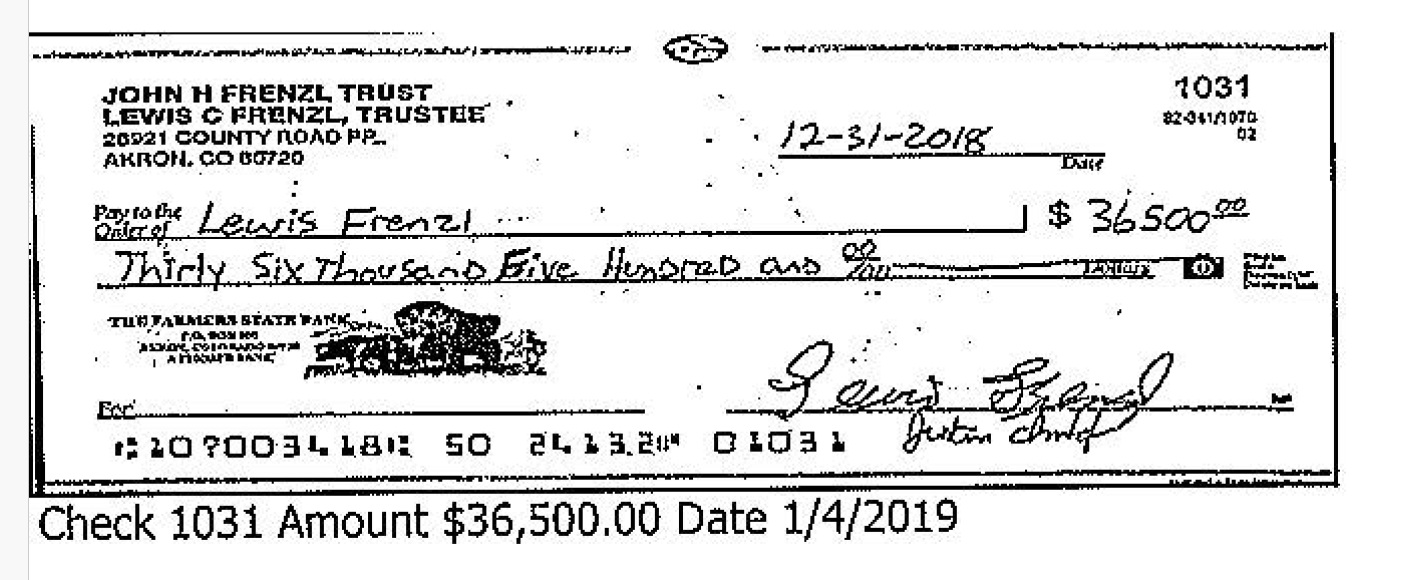

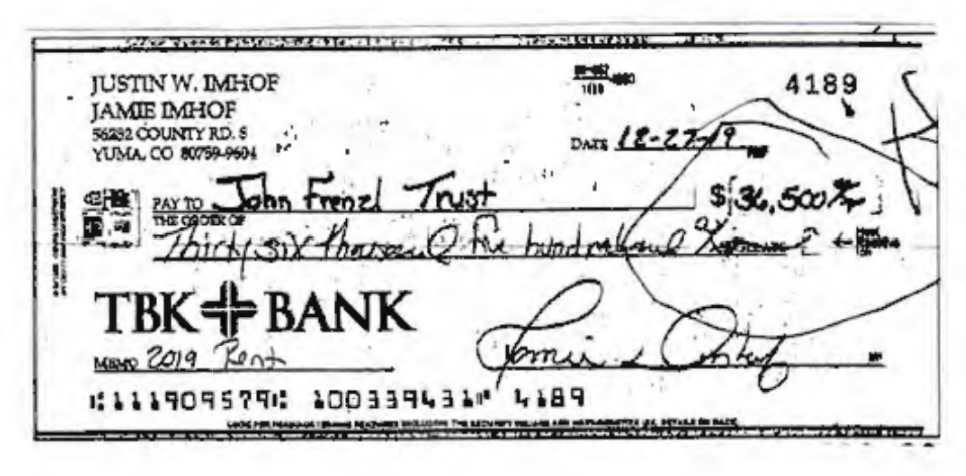

- 2018: Lewis imposes an account lock-out order requiring two signatures for withdrawals over $500

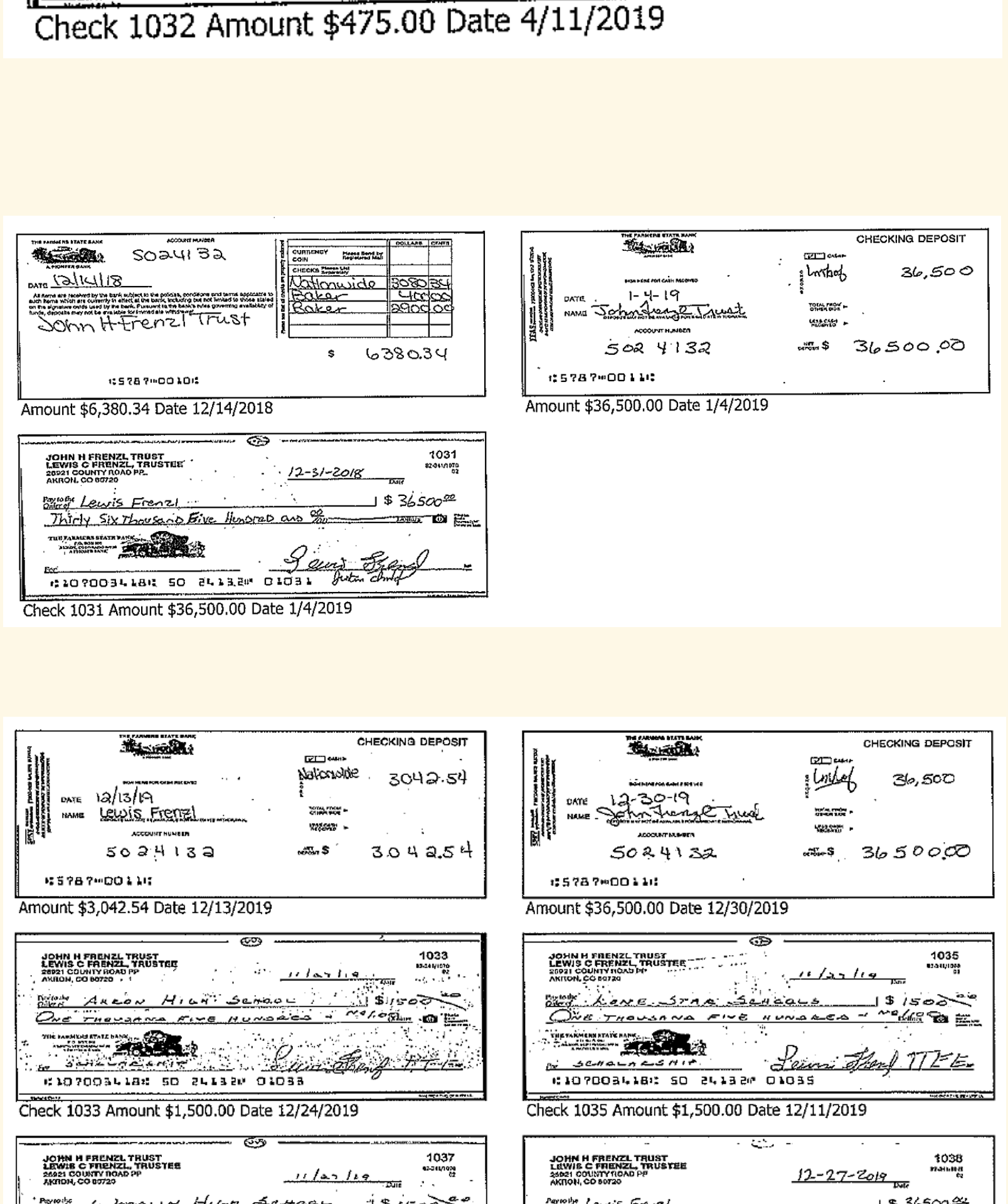

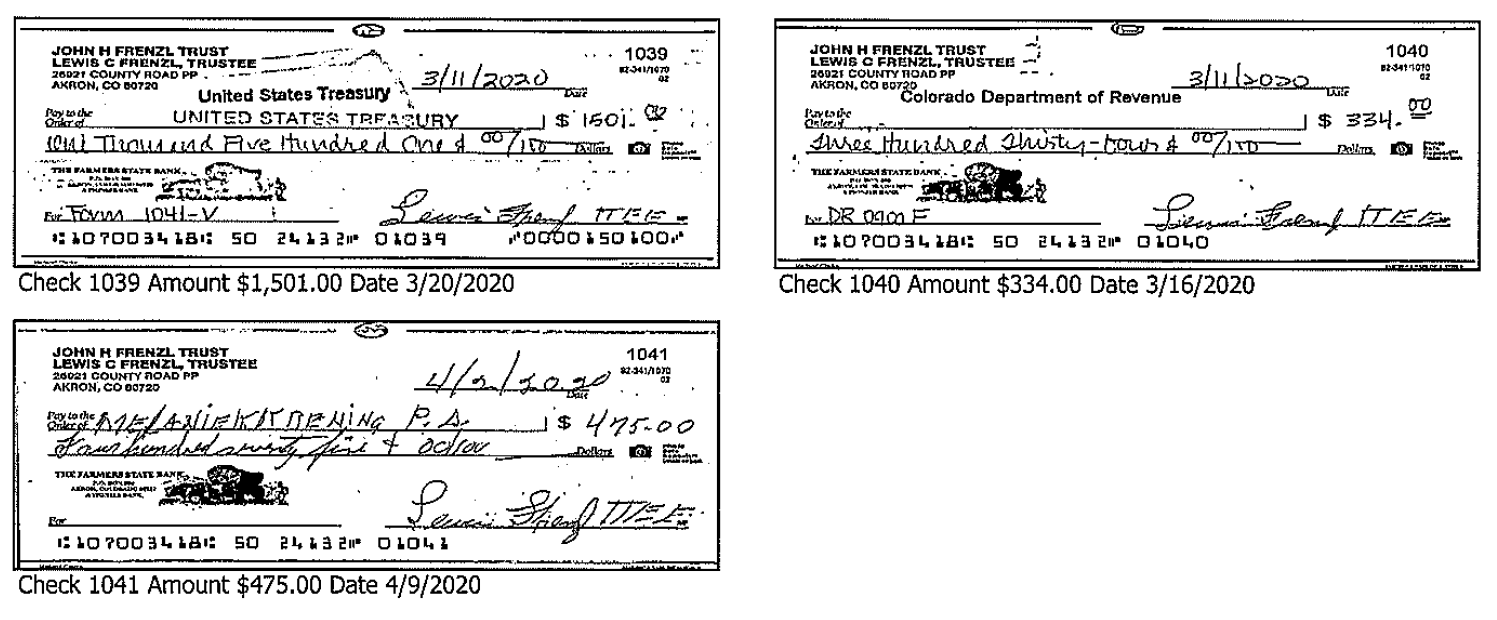

- 2019–2020: Recurring $36,500 check cycles with disputed signatures; JWI acquires personal real estate while JHF Trust rent goes unpaid; the Trust's checking balance begins a long, documented dwindle

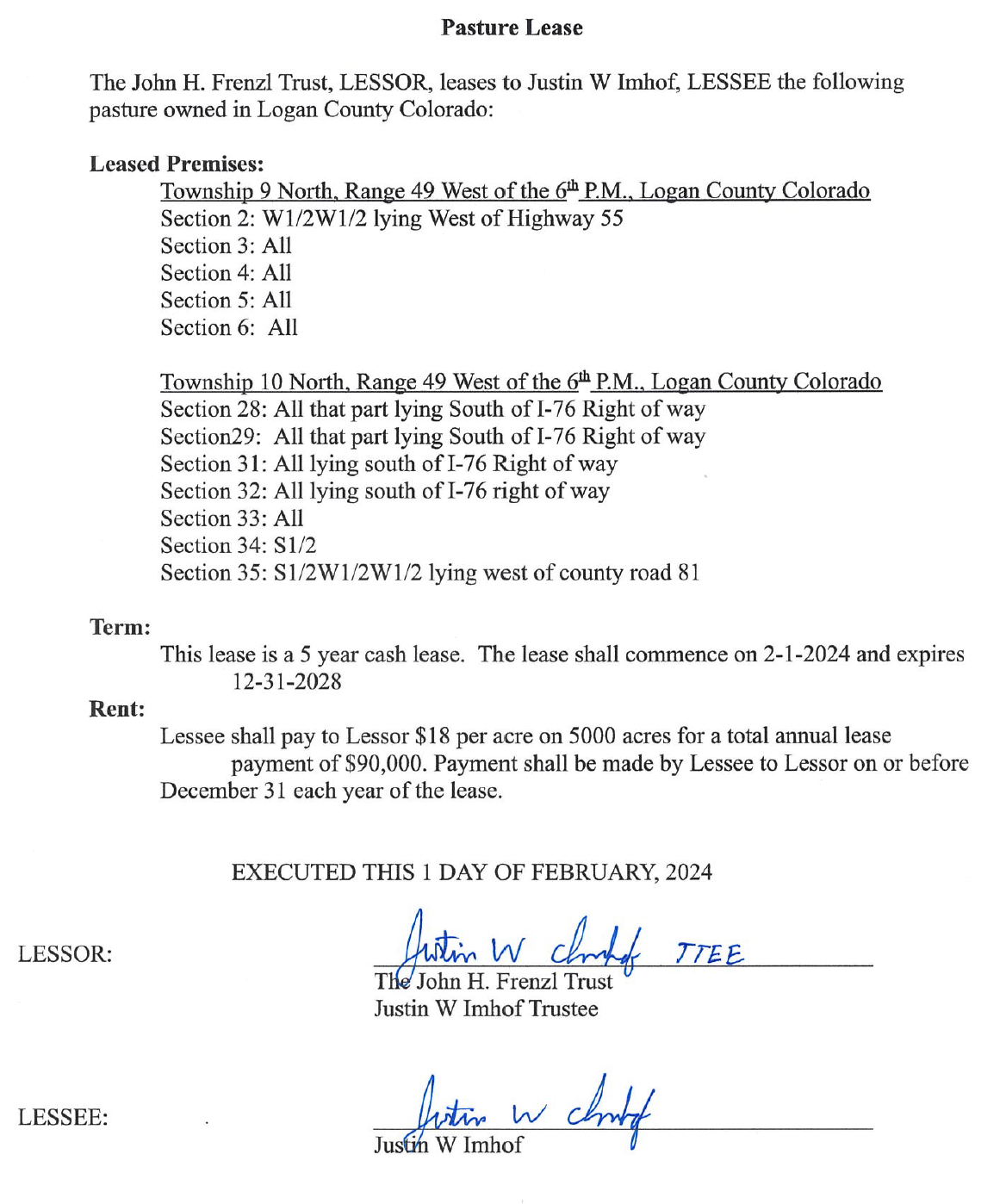

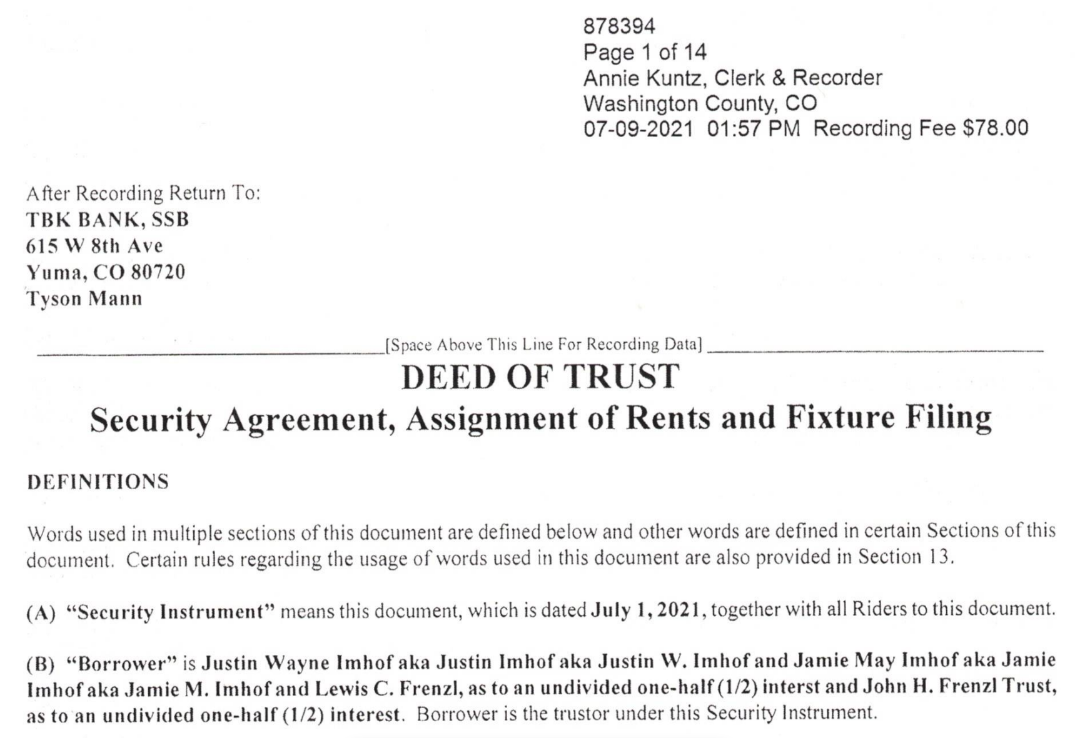

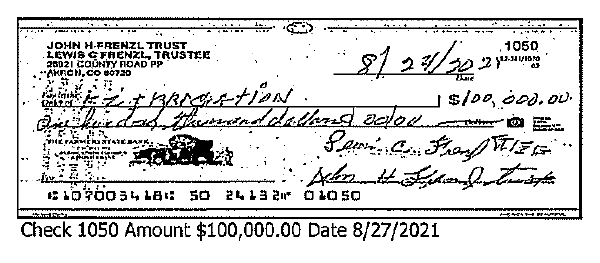

- 2021: $850,000 mortgage on six parcels — four borrowers including the JHF Trust; $146,000 in new pivot irrigation paid through the Trust; NSBC release of the Section 17 lien — $335,000 in mortgage satisfaction never credited to the Trust

- 2022: Lewis maintains the trust's scholarship obligations until weeks before his death

- 2023.01: Bank account address changed to JWI's address; Lewis dies January 14

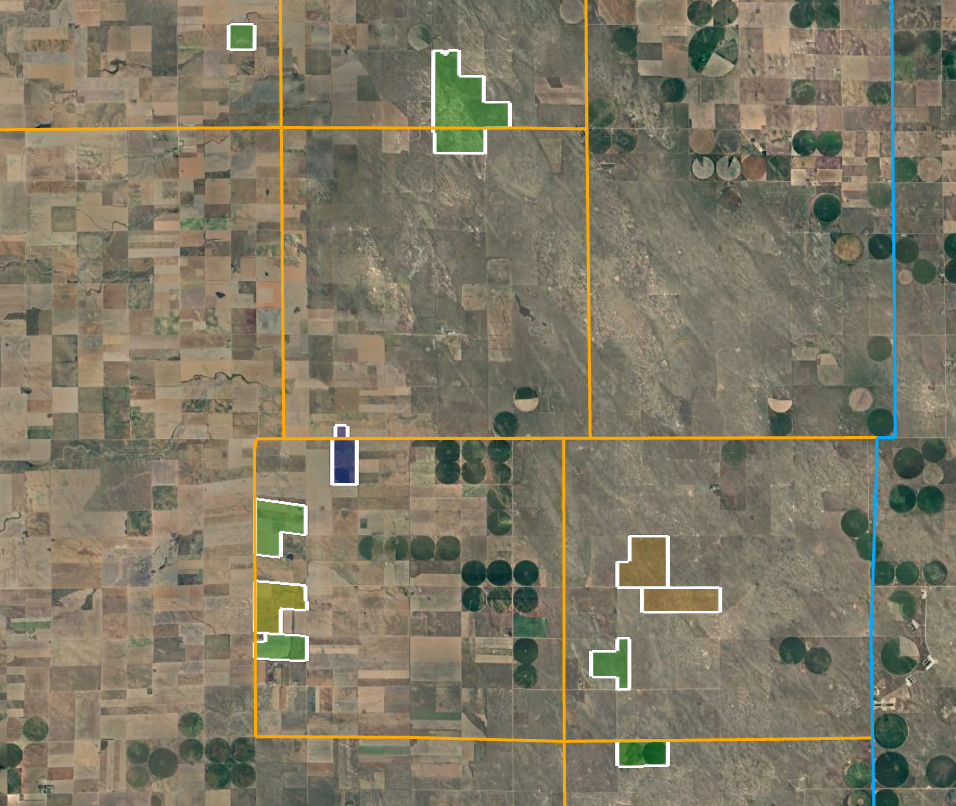

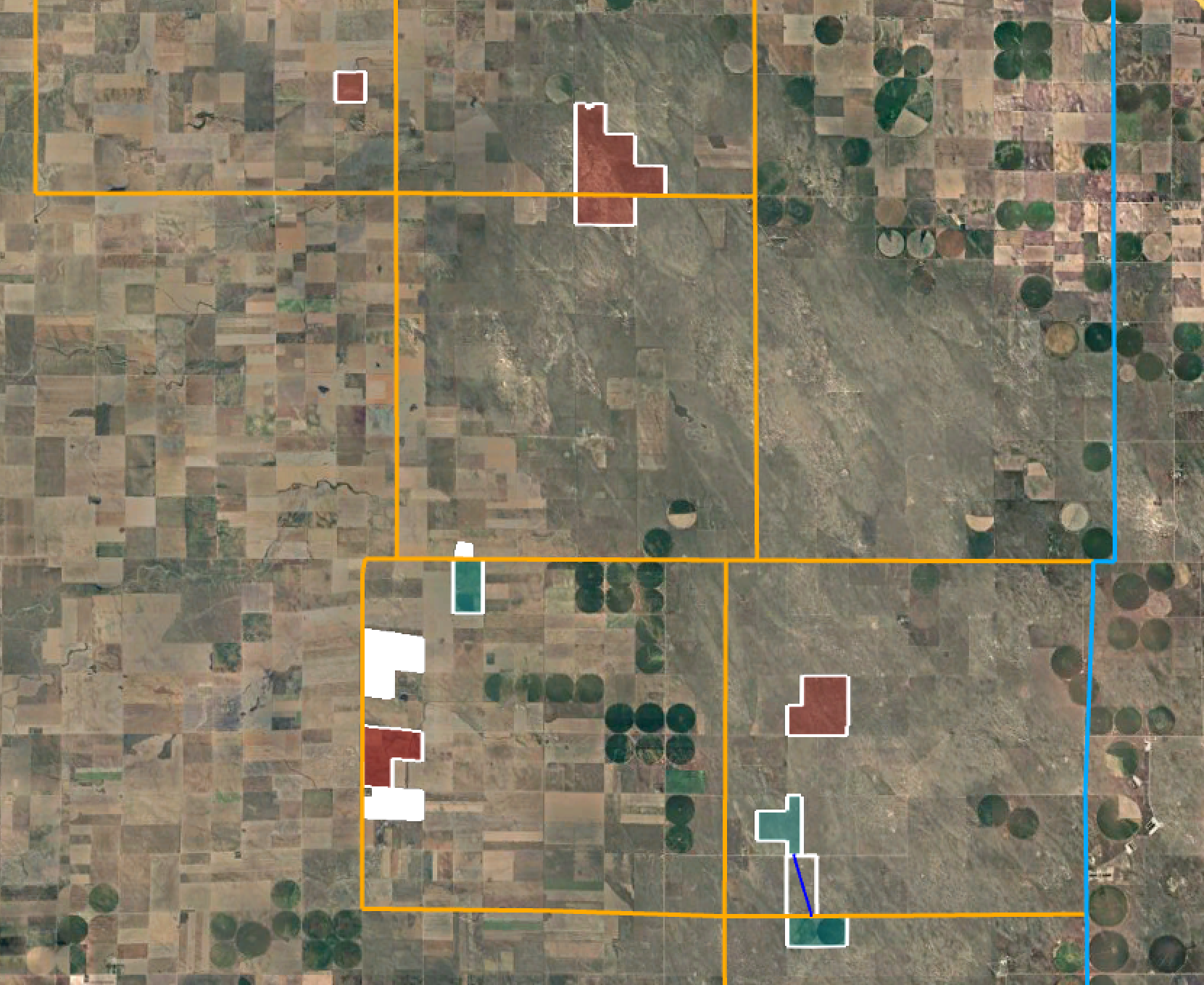

Land Footprint — Map Exhibits

The land changes in this chapter need to be shown spatially, over time. Source geometry is in the vault: Media/Earth/Frenzl.kmz (8 polygons, now also parsed to Media/Earth/Frenzl.geojson — one unified file, all geometry intact). The eastern polygon cluster (centers ~39.91–39.97 N, −102.89 W) is the Section 17 / Section 20–21 block at the heart of the 2015 mortgage transaction.

Aerial captures needed from Frenzl.kmz (Google Earth screenshots, dated imagery where possible):

- Ch.2-open footprint — all Frenzl WaCo/YuCo/LoCo holdings as of 3/13/2015

- Section 17 (NE¼, E½NW¼, S½ — Sec17-1S-49W) with the 2015-mortgaged boundary highlighted

- Sec 20 NE¼ + Sec 21 N½ — the three quarter-sections JWI/Jamie purchased 4/17/2015, shown bounded against Section 17

- Stock tank / well additions on Section 17 (June 2013 vs March 2016 historical imagery)

- Sandhills grain bin addition, N½ Sec5-T2S-R49W (June 2013 vs March 2016)

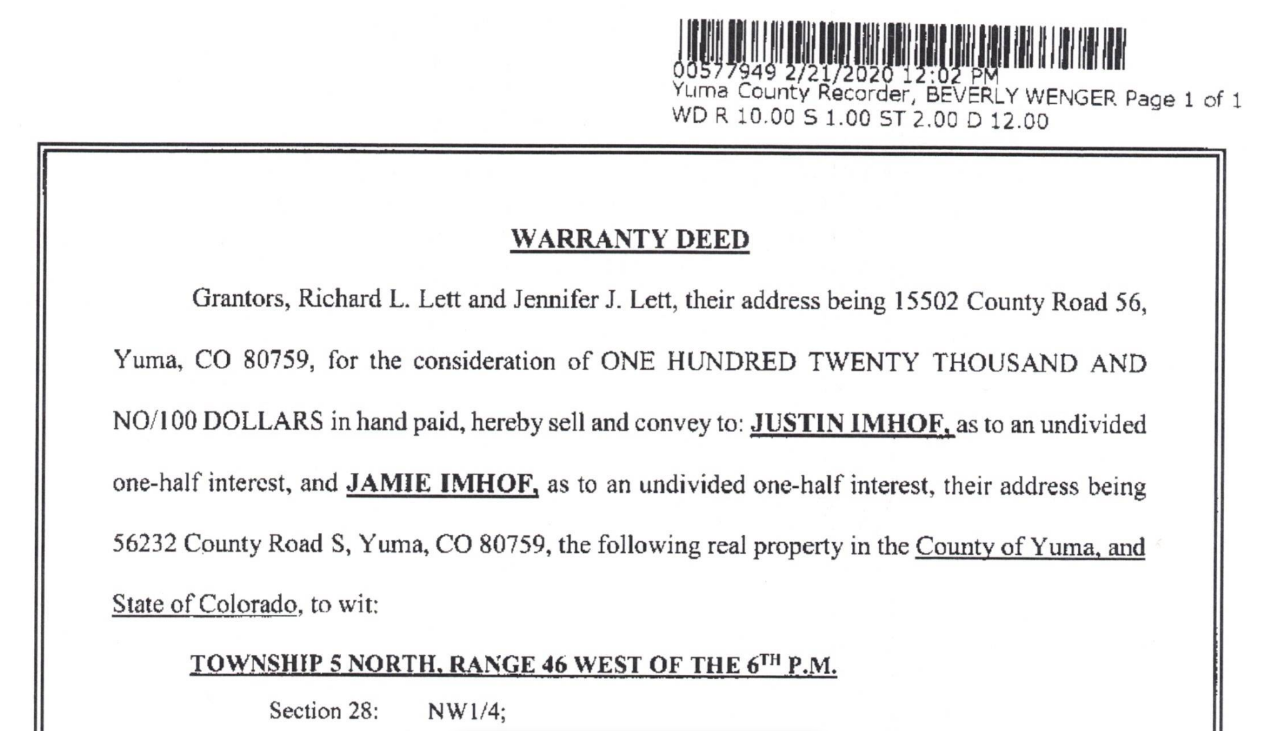

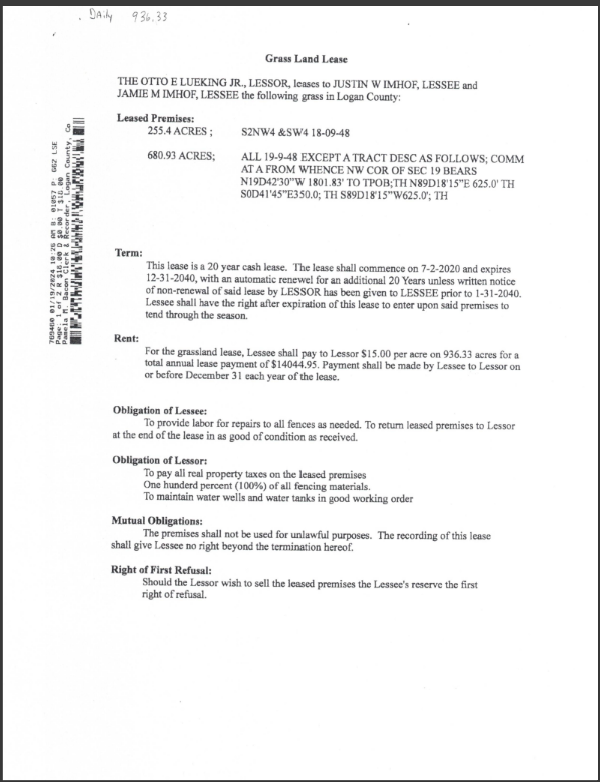

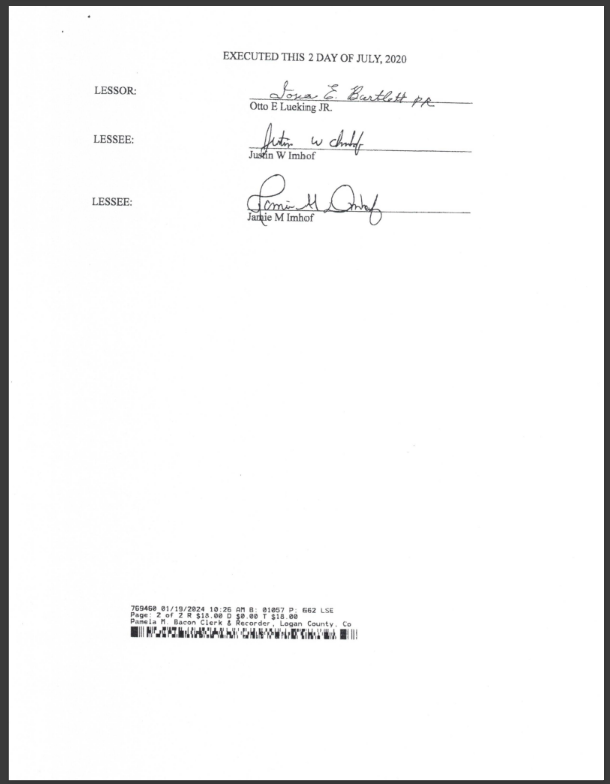

- 2020 acquisitions: Lett NW¼ Sec28-5N-46W, Lueking W½ Sec7-9N-48W, Salvador W½SW¼ Sec28-5N-46W

- Ch.2-close footprint — title state at 1/14/2023, before the Ch.3 transfers

2015 Petitioner's Exhibits (chapter-opening set)

PETITIONER'S EXHIBIT #20 — (caption pending Landon review)

PETITIONER'S EXHIBIT #20 (cont.) — (caption pending Landon review)

PETITIONER'S EXHIBIT #26 — (caption pending Landon review)

PETITIONER'S EXHIBIT #27 — (caption pending Landon review)

PETITIONER'S EXHIBIT #13 — (caption pending Landon review)

2015 instrument screenshot set (pending captions)

The OneNote 2015 page carried a fifteen-image run parked between the exhibit labels and the 3/13/2015 text — document strips and screenshots supporting the 2015 entries (deeds, tax-return rows, subordination passages). Landon: caption and redistribute these to their entries on review.

Caption pass — likely candidates: REC#861774/861775 deed views, Trust Revocation pages, 2015 tax return asset rows, REC#862059–66 instrument excerpts.

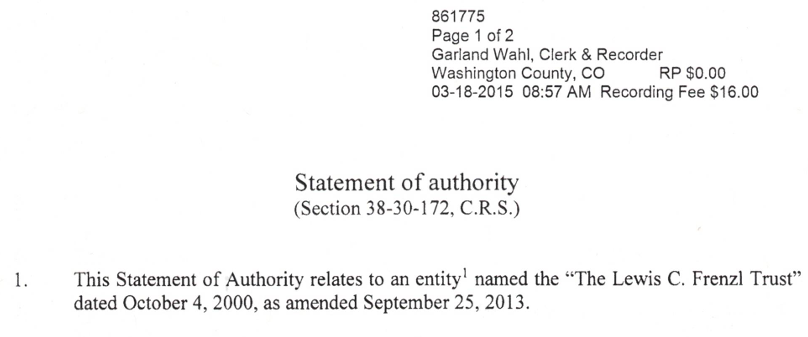

2015.03.13 — The LCF Trust Becomes an Estate

Instrument 1 — Revocation of Trust (un-recorded; produced in KSH files as LCF Trust Revocation 2015.pdf)

Two years and three months after John Frenzl's death, Lewis Frenzl executes a complete revocation of "The Lewis C. Frenzl Trust" dated October 4, 2000, as amended September 25, 2013:

"I, Lewis C. Frenzl... as Grantor of 'The Lewis C. Frenzl Trust' ('Trust Agreement') dated October 4, 2000, as amended September 25, 2013... do hereby revoke the powers and trusts created and conferred by Grantor in that Trust Agreement... I hereby direct you, as Trustee, to turn over and deliver to me all property held by you subject to the terms and provisions of the Trust Agreement, together with all accumulations of interest and income."

Signed by Lewis C. Frenzl, notarized by John Curt Penny (Notary ID 20094030839). The document's internal file reference reads "4646.000 - Frenzl - Revocation of Trust, 3/12/2015 1:40 PM" — a one-day discrepancy against the 3/13 execution date.

Instrument 2 — WaCo REC#861774

The same day, Lewis deeds all LCF Trust property — held since the October 4, 2000 Trust documents — back into his own name as an individual. The reciprocal trust structure that John and Lewis maintained through the entirety of their farming partnership is, from this date, dismantled on the Lewis side. There was no issue in the twelve years the brothers held reciprocal trusts; a couple of years after John's death, something became a problem that needed this action.

Instrument 3 — WaCo REC#861775

Also the same day, Lewis formally records and authorizes the September 25, 2013 amendments to his Trust. The initial amendments were executed nine months after John's death; the acknowledgement of those changes is recorded eighteen months after that. The only beneficiary to have received any documented benefit from these changes is Justin W. Imhof.

LCF Trust Revocation 2015.pdf (2024.05.15 KSH Files Provided) · 861774 · 861775

2015.04 — JHF Trust Tax Filings

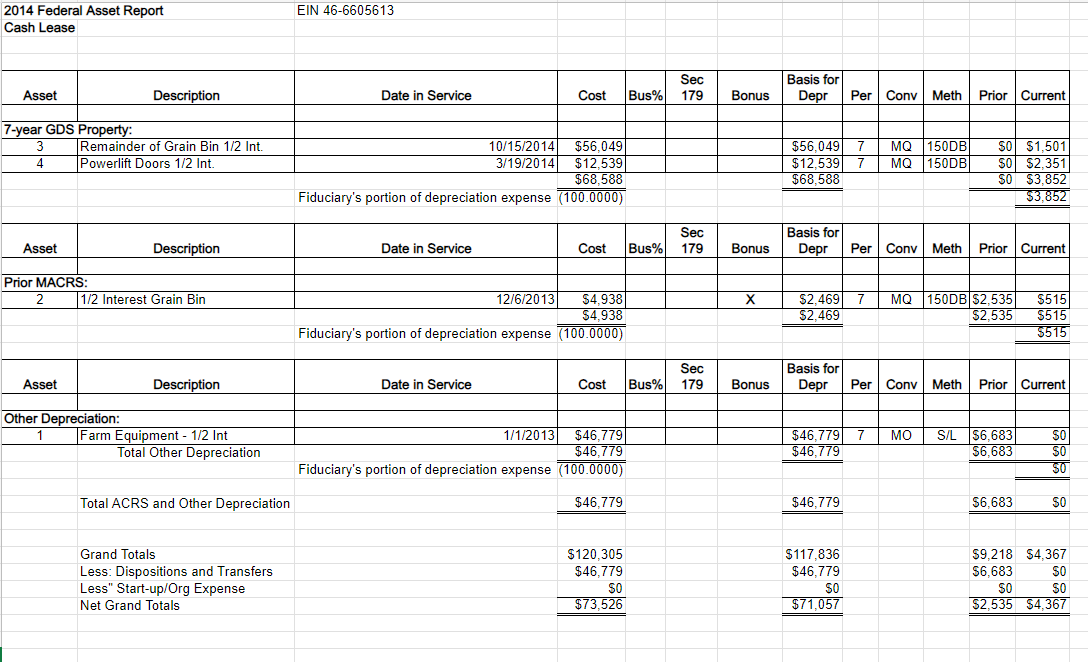

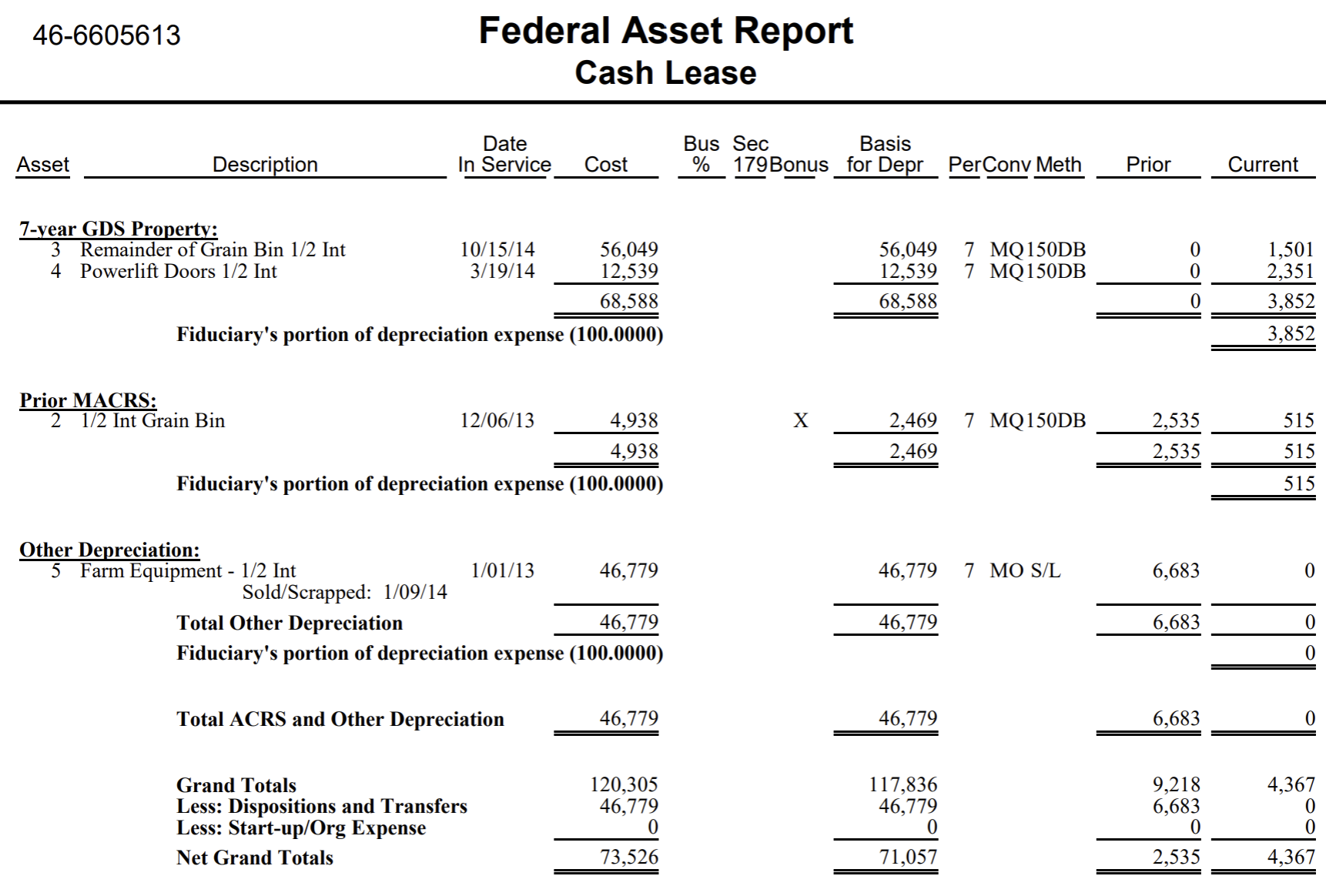

2015.04.10 — Melanie Krening finalizes JHF Trust tax returns. An IRS Form 4797 is filed, and the '1/2 Equipment Interest' asset ($46,779.00) is written off the Trust's books.

Callback to Ch.1 — the 2013 auction proceeds were never cash to the Trust. Ch.1 documented the 2013 equipment auction: total sales $102,785.00, auctioneer's 15% cut $15,417.75, net proceeds $87,367.25 — of which the JHF Trust's half would be roughly $43,683. The assets sold at that auction were not delivered to the Trust as cash proceeds. Instead, the Trust's half-interest was logged on the books as an asset — "Farm Equipment – 1/2 Int," $46,779.00 — and then, in this April 2015 filing, disposed of via Form 4797. The Federal Asset Report entry reads "Sold/Scrapped 1/09/14." Cash gains on auction sales are income, not assets; booking the proceeds as a depreciable asset and then writing that asset off accomplished a quiet devaluation of the Trust: the equipment left, the paper entry left, and no corresponding deposit has ever been identified in the JHF Trust account.

2015.04.15 — JHF Trust tax returns show a 'Well' placed into service for $31,450.00. No parcel location is specified in the returns.

2015.05.17 — JHF Trust tax returns show 'Stock Tank Concrete' placed into service for $17,753.00. No location is specified. Google Earth satellite imagery shows a stock tank was added to Section 17 (Sec17-1S-49W) between June 2013 and March 2016, with well-worn cattle paths and new concrete perimeter visible.

JHF 2015 Tax Returns · JHF 2014 Tax Returns (KSH files) — Form 4797 / Federal Asset Report

⏸ HARD STOP — What the Tax Record Actually Shows, 2009 → 2019

This subsection breaks the timeline on purpose. The fraud in this case did not begin with a deed — it begins in the tax record, and the tax record goes dark at exactly the moment control consolidates. Read this before continuing to 4/17/2015.

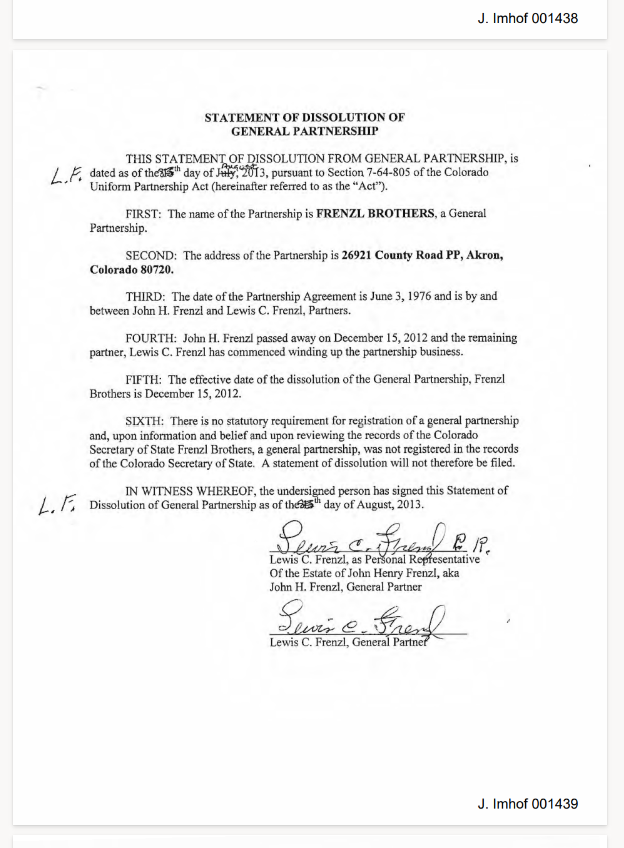

2009–2012 — Frenzl Brothers (the partnership baseline)

The brothers' operation filed as a true partnership — Frenzl Brothers (Form 1065), the 1961 arrangement formalized in the 1976 partnership agreement. The vault holds the complete Frenzl Brothers tax file for this era: 2009 return and amended return, financial statements, 1099s, pre-audits, 2010–2013 returns, and the partnership dissolution paperwork (CO/BarFZ/2009 Frenzl Brothers Files/Frenzl Brothers Tax File.pdf). This is the baseline of what an honest year on this land looked like: two partners, real revenue, real distributions, real 1099s.

Deep-extraction pass on the Frenzl Brothers 1065s (2009–2013) — pull gross receipts and partner distributions year-by-year to set the baseline revenue this land actually produces. The file is in the vault; the numbers belong in this table.

2012 — John's death; the Trust's first return

John dies 12/15/2012. The JHF Trust's first return (filed 3/23/2013 by Melanie Krening) reports $10,150 of Schedule E partnership income, $4,000 taxable, $760 tax paid — for an entity that owned one-half of roughly five thousand acres of active farm and ranch ground. No explanation has ever been provided for why the number is this small.

2013 — the last year the Trust looks like a farm

The 2013 return (filed April 2014) is the one honest-looking snapshot of the Trust as an operating entity:

| 2013 (filed 4/2014) | Amount |

|---|---|

| Schedule E rents received | $91,224 |

| Schedule E expenses | −$28,468 |

| Net rents | $62,756 |

| Sch F livestock sales* | $75,359 |

| Sch F co-op distributions | $16,680 |

| Sch F ag program payments | $11,340 |

| Sch F crop insurance | $9,005 |

| Sch F expenses | −$162,266 |

| Net farm loss | −$49,882 |

| Total income (1041) | $12,874 |

\On 5/15/2024 Kelly Hansen stated no cattle were ever held by the Trust — yet the Trust's own 2013 return reports $75,359 in livestock sales.*

2014 — the equipment vanishes on paper

Filed early, 12/18/2014, before the tax year closed. The Form 4797 / Federal Asset Report disposes of "Farm Equipment 1/2 Int" — $46,779.00 — marked "Sold/Scrapped 1/09/14." No corresponding cash deposit to the Trust has been identified. The 2013 auction money passed through someone's hands; the Trust's books only ever saw the asset entry and its deletion.

2015 — assets in, no depreciation statements

The 2015 return (filed 3/18/2016) books $74,609 of new infrastructure into the Trust — Well $31,450, Stock Tank Concrete $17,753, Sprinkler Tires $6,400, Building Repairs $15,271, Fencing $4,135 — none with a parcel location specified, and strangely, no MACRS depreciation statements attached. The Trust is paying to improve land and buildings while its lease income terms are being renegotiated downward (Ch.1, and see 1/27/2017 below). Improvements that benefit the tenant's operation are being capitalized into the landlord Trust — the Trust pays, JWI farms.

2016–2019 — the record goes dark

From the 2016 tax year forward, no JHF Trust tax filings have been produced for 2016, 2017, 2018, or 2019. This is precisely the window in which:

- Teresa Jo Imhof holds appointment as Personal Representative (named PR in Lewis's 2015 Will, and PR of record for the estate machinery) and is controlling the show, and

- Justin W. Imhof is the hand making the agreements and signing the documents — the third Farm Lease (1/27/2017), the bank signature cards (8/3/2016), the account drawdown (8/7/2016), the diverted rent check (11/28/2016).

Both are highly culpable, and the division of labor is itself probative: the person with fiduciary-adjacent authority (TJI as PR, as account signatory) directing structure, and the person with the operational benefit (JWI as tenant, as account signatory) executing instruments. A trust that owns thousands of acres does not lawfully produce zero filings for four consecutive years. The dark window is where the draining documented in the rest of this chapter happened without even a paper shadow.

Frenzl Brothers Tax File.pdf · JHF 2012 Tax Returns-ish KSH set: JHF 2012/2013/2014/2015 Tax Returns.pdf · Melanie Krening subpoena production (2024.10.11)

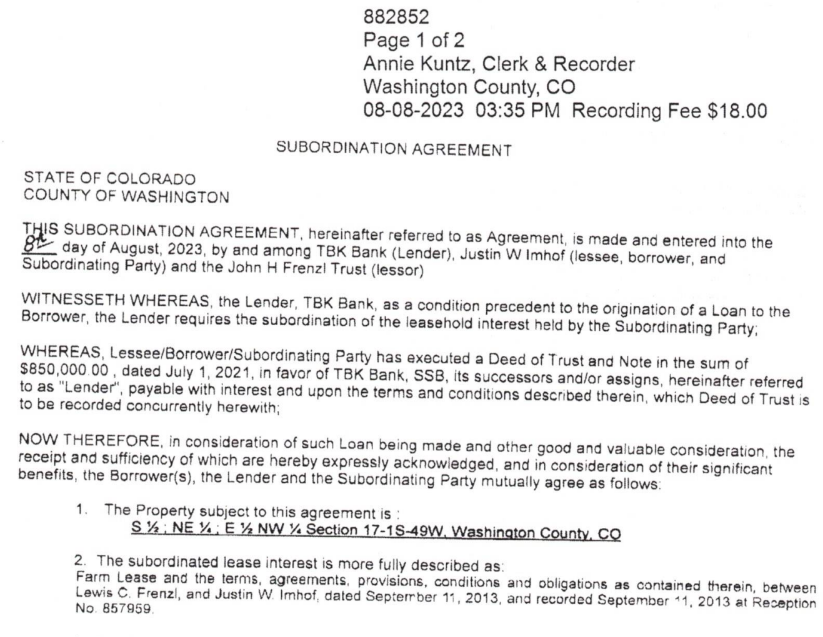

2015.04.17 — Section 17 Mortgage ($335,000)

WaCo REC#862059–#862066

One month after deeding himself his own Trust property back into his personal name, Lewis Frenzl — as Trustee for the JHF Trust and individually — mortgages free-and-clear land in NE¼, E½NW¼, S½ of Sec17-1S-49W against a $335,000.00 loan from Northstar Bank of Colorado (NSBC). The proceeds are directed to Justin and Jamie Imhof's purchase of grassland.

The land they bought sits directly against the land that paid for it. The purchase (REC#862059, grantor Donna J. Dressel) conveys NE¼ Sec 20 and N½ Sec 21, T1S R49W — three quarter-sections (480 acres) of additional grassland directly south of and bounded to Section 17, the very property mortgaged to fund the deal. The KMZ geometry shows the purchased block sharing the boundary line with the Section 17 ranch ground. This was not a diversification purchase; it was an expansion of the same contiguous block — paid for with the Trust's equity, titled solely to Justin and Jamie Imhof as joint tenants.

And the doc fee says it wasn't a down payment — it was the whole price. REC#862059 recites $10 "and other good and valuable consideration," but carries a Colorado documentary fee of $33.50. At the statutory $0.01 per $100 of consideration, that implies a purchase price of $335,000 — exactly the amount mortgaged against Section 17. The "down payment" framing in the family's earlier understanding was generous: the implied numbers show JHF Trust collateral funding the entire purchase price of land the Trust would never own a foot of.

The transaction's recorded instruments:

| REC# | Instrument | Effect |

|---|---|---|

| 862059 | Warranty Deed (Dressel → JWI & Jamie, JTWROS) | Three quarter-sections, Sec20 NE¼ + Sec21 N½, adjoining Sec17 |

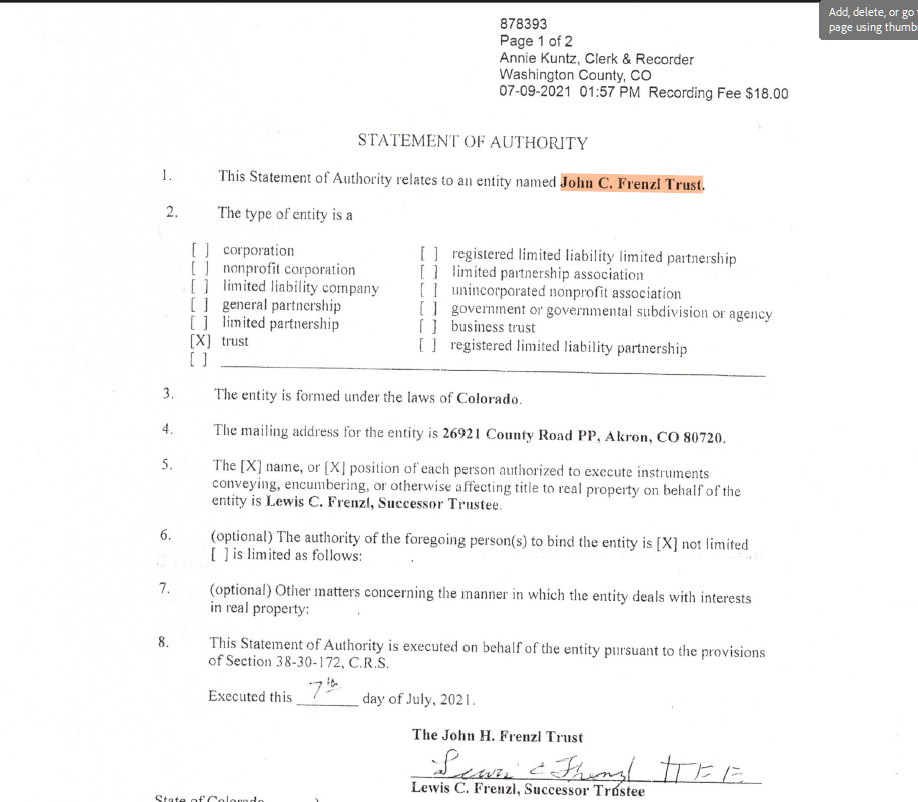

| 862060 | Statement of Authority | Lewis Frenzl signing authority for the JHF Trust |

| 862061 | Easement | Access to the new JWI/Jamie property through and across Frenzl land |

| 862062 | Deed of Trust (JWI & Jamie) | Lien on their newly purchased land |

| 862063 | Deed of Trust (JHF Trust ½ + LCF ½) | The $335,000 loan against Section 17; variable rate; maturity 3/31/2035 |

| 862064 | Subordination Agreement (LCF) | Lewis's lease interest subordinated to NSBC |

| 862065 | Subordination Agreement (JHF Trust) | The Trust's lease + security interests subordinated to NSBC |

| 862066 | Subordination Agreement (JHF Trust) | The Trust's interest in the first Farm Lease [REC#857958] subordinated as to Section 17 rents |

What "subordination" means, and what it did here

A subordination agreement is a contract in which a party holding an existing right — a lease, a lien, a security interest — agrees that someone else's claim will be paid or enforced first. If the borrower defaults, the subordinated party stands behind the lender in line: their lease can be extinguished by foreclosure, and their security interest collects only from whatever is left. Lenders demand subordination precisely because an existing lease or lien would otherwise survive foreclosure and reduce the collateral's value.

Applied here, the OCR of REC#862065 shows the JHF Trust gave up its protective position in its own land:

"NSBC'S LIEN. The Superior Indebtedness is or will be secured by the Real Property... from JOHN H. FRENZL TRUST and LEWIS C. FRENZL to NSBC... As a condition to the granting of the requested financial accommodations, NSBC has required that NSBC's Lien be and remain superior to the Subordinated Lease."

"Justin and the JHF Trust each represent and acknowledge to NSBC that the JHF Trust will benefit as a result of these financial accommodations from NSBC to Justin, and the JHF Trust acknowledges receipt of valuable consideration for entering into this Subordination."

"The JHF Trust also subordinates to NSBC's Lien all other Security Interests in the Real Property held by the JHF Trust, whether now existing or hereafter acquired."

"AUTHORITY. The JHF Trust represents and warrants that it has authority to execute this Subordination..."

Three observations, stated factually:

- The "benefit" recital is false on its face. No benefit to the JHF Trust from financing Justin and Jamie Imhof's personal land purchase has ever been identified, and no "valuable consideration" received by the Trust has ever been produced. The recital exists because the lender's form requires it; signing it made the Trust warrant something that was not true.

- The Trust subordinated everything, prospectively. Not just the lease — all security interests, "now existing or hereafter acquired." The Trust's ability to protect its own half of Section 17 was signed away as a package.

- REC#862063 contains a cross-collateralization clause: the Deed of Trust secures "all obligations, debts and liabilities... of either Grantor or Borrower to Lender... whether now existing or hereafter arising, whether related or unrelated to the purpose of the Note." The Trust's land became standing collateral for the Imhofs' general borrowing relationship with NSBC, not just this note.

Document irregularity — false instrument submitted to lender

Justin provides NSBC with the first Farm Lease [REC#857958 — term 1/1/2013–12/31/2017] as proof of lease for this transaction. But the second, renegotiated Farm Lease [REC#859040 — term 1/28/2014–12/31/2022, which superseded REC#857958] is the operative lease on this date and is not disclosed to the bank. A materially different lease was submitted as documentation than the lease actually in effect — meaning false documents were submitted to a federally-related lending transaction.

Devin's note "This is something that neither of us — or at least I — never seemed to have caught in the review of the documents. How fucking wild. JWI commits yet another unlawful act."

862059 · 862060 · 862061 · 862062 · 862063 · 862064 · 862065 · 862066 · 857958 · 859040 — OCR pass 2026.06.12

2015.07.12 — Case IH Quadtrac 450

Karie Imhof posts a picture of a Case IH 450 Quadtrac pulling a Brent grain cart (not the Brent 774 being searched for). Johnnie Eskew recalls Justin almost lost the QuadTrac to the bank and Lewis Frenzl helped bail him out. Mae still worked at the bank in Otis and saw him on the "sheets." Justin ultimately sold the tractor to get out from under it.

Karie Imhof Facebook, 7/12/2015 — Case IH 450 QuadTrac with Brent grain cart. (facebook.com/keimhof22)

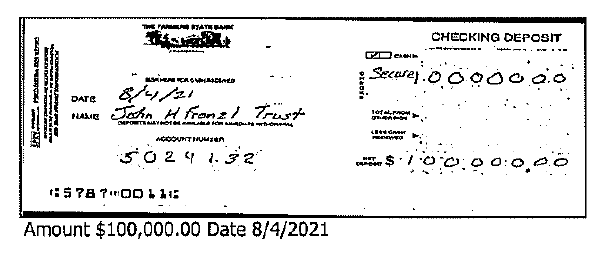

2015.07.14 — Hart Meeting / Annuity Change

JWI and LCF visit Mark Hart (JHF/LCF financial advisor) and change Athene to Nationwide. LCF states this purchase of a $64,322 annuity constitutes approximately 2.2% of LCF's net worth.

$64,322 ÷ 0.022 = $2,923,727.27 implied net worth.

Mark Hart meeting notes / Hart deposition — confirm date and content

2015.09.17 — Frenzl Brothers Vehicle Titles

- Title Number 27E116597 issued to Lewis Frenzl: 1985 Freightliner FLC Semi Truck (VIN: 1FUPYKY89FP269468, CO Plate: 283HXK)

- Title Number 27E116598 issued to Lewis Frenzl: 1984 Merritt Equipment Grain Trailer (VIN: 1MT2P4223EH004423, CO Plate: 688HHK)

Both assets transferred out of Frenzl Brothers (Business ID: 000143496265, 26921 County Road PP, Akron CO 80720).

There is no tax information showing that any consideration of value was given to the JHF Trust for these transfers. Frenzl Brothers was a 50-50 partnership; on John's death his partnership interest flowed to his estate and, under the pour-over will, to the JHF Trust. Half of these titled assets carried JHF Trust value out of the partnership with no payment, no 1099, and no tax entry recognizing the Trust's side of the transaction.

2024.11.08 email from SGR — title records

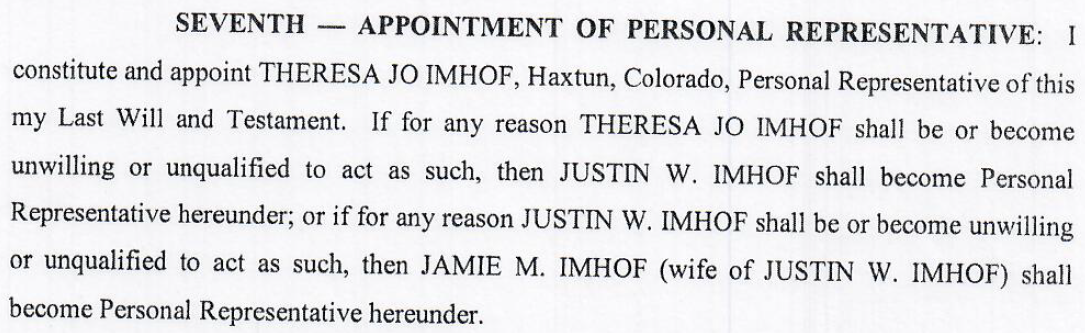

2015.10.13 — Lewis Frenzl's New Will

First, the structural point: a trust is not an estate

Because Lewis revoked his trust on 3/13/2015, everything he owned at death would now pass through probate — and the difference matters:

- A trust (C.R.S. Title 15, Article 5 — Colorado Uniform Trust Code) owns property continuously. At the settlor's death there is no court process: the successor trustee administers under § 15-5-801 et seq., owes beneficiaries duties of loyalty and impartiality, and under C.R.S. § 15-5-813 owes a duty to inform and report to beneficiaries. John's side stayed in trust — which is why the JHF Trust's beneficiaries (the Eskew family) hold enforceable information rights that this case is built on.

- An estate (C.R.S. Title 15, Article 12 — probate administration) is controlled by a Personal Representative appointed by the court. The PR's powers are broad (§ 15-12-711), supervision is minimal in unsupervised administration, and once the estate closes, the PR's control ends with distribution. Whoever is PR effectively is the estate while it is open.

- Under C.R.S. § 15-5-602, a settlor may revoke or amend a revocable trust while living — and at the settlor's death a revocable trust becomes irrevocable. By revoking entirely, Lewis traded a structure with built-in beneficiary oversight for one controlled by whoever held the PR appointment. That person, under the new Will: Teresa Jo Imhof.

To Devin's question — revocable or irrevocable? The 2015 Will itself never uses either word for the trusts it creates. The only appearance of "irrevocable" in the document set is in the Revocation instrument's Article VII: "On the death of the Undersigned, the Trust created hereinafter shall become irrevocable." Testamentary trusts (trusts created by a will) are inherently irrevocable once the testator dies — there is no one left who can amend them. An estate itself is neither revocable nor irrevocable; it is simply an administration process. So the practical answer: nothing in the new structure was revocable by anyone but Lewis, and after 1/14/2023, nothing in it was revocable at all.

What the Will does

Three years and two months after John Frenzl's death, Lewis executes a new Last Will and Testament revoking all prior wills and codicils. Key provisions:

- All personal household effects — jewelry, clothing, furniture, furnishings, guns, silver, books, art, automobiles — to Justin W. Imhof

- All residue and remainder of Lewis's property distributed to Justin W. Imhof

- Jamie M. Imhof (JWI's wife, mentioned eight times) named remainder beneficiary on JWI's death; a separate trust is created for her benefit, of which she is sole Trustee

- Teresa Jo Imhof named Personal Representative; JWI successor PR; Jamie M. Imhof second successor PR

- JWI designated sole Trustee of the residuary trust created for his own primary benefit

- Trustee given full discretion over income and principal; no court oversight; no reporting obligation

The trust-multiplication structure

The Will doesn't create one trust — it contemplates a family of them:

- The residuary trust for Justin W. Imhof (he is sole Trustee of his own trust)

- A separate trust for Jamie M. Imhof (she is sole Trustee of her own trust)

- Separate trusts for each descendant of Justin W. Imhof under age 25 — plural by its own terms

- The Will's FIFTH clause additionally directs that any principal distributable to any beneficiary "shall not be distributed outright... but shall instead be held IN TRUST"

With Justin, Jamie, and their children each carrying a trust, five or more sibling trust entities under common family control is a fair reading of the architecture — a structure in which value can be appointed, distributed, and re-trusted between entities that all answer to the same kitchen table, with no outside beneficiary holding information rights over any of them.

Succession clause — confirmed against the document

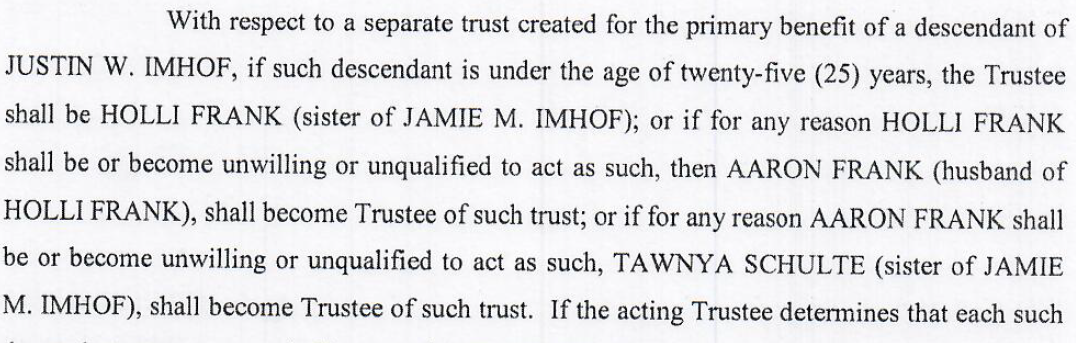

Landon's recollection was that the Holli/Aaron/Tawnya chain governed the LCF trust if Justin were disqualified. The OCR confirms a narrower reading. The chain appears on page 5 and applies only to trusts for Justin's under-25 descendants:

"With respect to a separate trust created for the primary benefit of a descendant of JUSTIN W. IMHOF, if such descendant is under the age of twenty-five (25) years, the Trustee shall be HOLLI FRANK (sister of JAMIE M. IMHOF); or if for any reason HOLLI FRANK shall be or become unwilling or unqualified to act as such, then AARON FRANK (husband of HOLLI FRANK), shall become Trustee of such trust; or if for any reason AARON FRANK shall be or become unwilling or unqualified to act as such, TAWNYA SCHULTE (sister of JAMIE M. IMHOF), shall become Trustee of such trust."

For the main residuary trust, JWI is sole Trustee; for Jamie's trust, Jamie is sole Trustee. The PR chain is Teresa → Justin → Jamie. At no point does trusteeship or representation leave the Imhof/Frank/Schulte family circle.

The absolution language — confirmed verbatim

Landon's recollection that prior trustees are forgiven their acts is confirmed, in three separate clauses:

TENTH: "No successor Trustee shall be obligated to examine the accounts, records and acts of the previous Trustee or any allocations of the Trust estate, nor shall such successor Trustee in any way or manner be responsible for any act or omission to act on the part of any previous Trustee."

TWELFTH: "The Trustee shall be under no obligation to inquire into the acts or the accountings of the Personal Representative, but shall be entitled to receive assets delivered to it as the entire corpus of the Trust estate."

SIXTEENTH: "No one dealing with the Trustee need inquire concerning the validity of anything done by it or see to the application of any money or property transferred by it or upon its order."

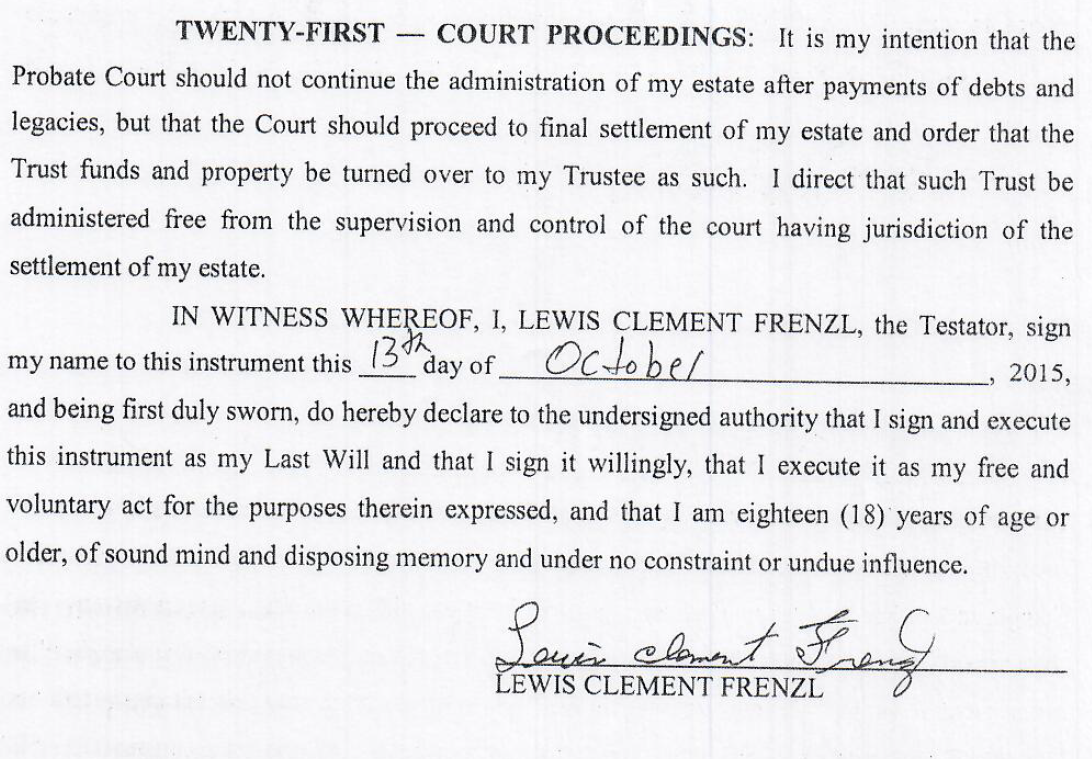

Plus the anti-court directive: "It is Lewis Frenzl's wish and desire that in making a division of my property... the same shall be done without the intervention of any court, and that no report of any kind be made to the court."

Read together: no court, no reports, no successor review of predecessor conduct, no third-party duty of inquiry — an instrument engineered so that no one would ever be obligated to look.

Note: This Will provides no distribution to Helen (Eskew) Frenzl or any member of the Eskew family. It does not reference the JHF Trust, its beneficiaries, or Lewis's ongoing obligations as JHF Trust Trustee. The Lewis & John Frenzl Scholarship Fund, Inc. is not referenced. Witnesses: Daniel Mong and Kevin E. Clapham (Denver addresses); notarized in Washington County by Elizabeth P. Kennedy. No drafting attorney is identified anywhere on the instrument.

2023.02.02 LCF Last Will and Testament — full OCR pass 2026.06.12

2015.11 — Site Visit Documentation by Landon Eskew, then 26

This documentation exists because Landon personally went out to visit his great-uncle Lew — a stop at the Frenzl Farm on a trip back to see Colorado family, traveling from Landon's residence at the time in North Dakota. These weren't investigative photos; they were a 26-year-old visiting family. They became evidence later.

2015.11.26 — Frenzl Farm, 26921 County Road PP, Akron CO, 2:40 PM. Three photographs: (1) the old workbench in the small Quonset west of the house; (2) a Polaris Sportsman 500 four-wheeler; (3) a 1971 Ford Ranger pickup.

Landon Eskew site photo, 11/26/2015 — 1971 Ford Ranger pickup in the shed. Note the well-maintained floor.

Landon Eskew site photo, 11/26/2015 — Polaris Sportsman 500, small Quonset west of the homestead.

These assets were later omitted from or unaccounted for in JWI's Schedule A inventory submissions. When court proceedings began, the Imhofs submitted an updated asset sheet but "couldn't find" the four-wheeler in the shed — while renting all of the Frenzl land, while Justin and Teresa sat as signatories on the JHF bank account, and while Teresa held PR appointment.

And the assets never moved. Upon site visit after Lewis Frenzl's death [citation date needed — pull date from post-2023 site visit photo EXIF], these same assets were still at the homestead property, in the same Quonsets.

Landon site photographs — assets/Ch2_image023-024.png; full-resolution originals recovered from MHT as Ch2_image118–123.jpg (identify and caption below)

Recovered full-resolution photo set (pending identification)

The six camera-resolution JPGs below were embedded in the OneNote 2015 section but were never extracted by the original conversion. Recovered 2026.06.12. Landon: identify each (site visit vs. binder photos) and assign captions.

Caption pass needed — likely candidates: workbench Quonset photo, Ranger, Polaris, Frenzl binder spreads at Bill & Karen's (11/28/2015, 10 PM).

2015.11.28 — The Frenzl Binder: What Was Taken, and What Survives

This date is only a milestone of when Landon photographed the Frenzl documents remaining in Bill and Karen Eskew's possession. The story of the binder itself, as Karen Eskew later told it to Landon and Devin, is the important part:

Lewis Frenzl invited Bill and Karen down to the homestead property. When they arrived, Justin was there with Lew — and they were surprised to see him there. Justin told them that portions of the binder Bill Eskew had received — containing the October 4, 2000 documents — needed to be removed "because they weren't needed anymore." Justin removed those documents from Bill's binder copy and never returned them.

What we know about the binder's contents:

- The John H. Frenzl Trust began at section six of the binder and consisted of 16 pages.

- That means there were prior sections — which would have contained Lewis Frenzl's trust, potentially Frenzl Brothers partnership business documentation, and further breakdowns of assets.

- We will never know exactly, because after that date Bill and Karen Eskew never received those documents back.

Judy Shively, the trust attorney for both JHF and LCF, is in possession of these original documents to date. She was sick for her deposition, which was never rescheduled. Her file would tell us what the binder contained — and for reasons never explained, it was never produced.

Per Karen's subpoena response: "According to JWI there was only one notebook after LCF death."

Landon Eskew photo, 11/28/2015, 10 PM — the "Frenzl Notebook" at Bill and Karen Eskew's house. Note the binding type and the stamp at the bottom left.

Karen Eskew subpoena responses · Karen's account as told to Landon & Devin · Shively deposition: noticed, not taken, never rescheduled

2015.12.31 — Cumulative Breach Ledger

As of December 31, 2015:

- ☐ No documentation that the JHF Trust received a 50% split of any equipment auction proceeds (2013) — and per the 2015 Form 4797, the Trust's half-interest was written off as an asset disposition, not received as cash

- ☐ Whereabouts of the CaseIH sprayer unknown — carried from Ch.0/Ch.1 unresolved items; one-half belongs to the JHF Trust

- ☐ Contents of the pre-section-six binder documents removed by JWI on or before 11/28/2015 — never returned, never produced (Shively)

- ☐ No proof of JWI lease payment, 2013 growing season

- ☐ No proof of JWI lease payment, 2014 growing season

- ☐ No proof of JWI lease payment, 2015 growing season

- ☐ No proof of any initial $150,000.00 contribution to the Lewis & John Frenzl Scholarship Fund, Inc.

- ☐ No tax recognition of consideration to the JHF Trust for the Frenzl Brothers vehicle titles moved to LCF personally (9/17/2015)

JHF Trust bank statements 2013–2015 · Farm Lease terms · Ch.0/Ch.1 ledgers

2016 — Account Access, Account Cleared

2016 Petitioner's Exhibits (year-opening set)

PETITIONER'S EXHIBIT #28 — (caption pending Landon review)

PETITIONER'S EXHIBIT #29 — (caption pending Landon review)

(exhibit continuation — caption pending Landon review)

2016.03.18 — 2015 JHF Trust Taxes Finalized: The Year-Over-Year Tell

Melanie Krening finalizes the 2015 JHF Trust tax returns. Set against the prior years, the trajectory is the tell:

| Tax year | Filed | Rents (Sch E net) | Farm activity (Sch F) | Total income | What's being added to the books |

|---|---|---|---|---|---|

| 2012 | 3/23/2013 | $10,150 gross | — | $10,150 | — |

| 2013 | 4/2014 | $62,756 | $112,384 gross / −$49,882 net | $12,874 | Grain Bin ½ int. |

| 2014 | 12/18/2014 (early) | not produced in detail | not produced in detail | n/a | Powerlift Doors ½, Grain Bin remainder ½; Form 4797 writes off equipment |

| 2015 | 3/18/2016 | collapsing | no MACRS statements | n/a | Well $31,450 · Stock Tank $17,753 · Sprinkler Tires $6,400 · Building Repairs $15,271 · Fencing $4,135 |

Read the direction of money: revenue lines shrink, capital outflows grow. From 2015 forward the Trust is not operating as an income-producing landowner — it is functioning as a checkbook for improvements to land and infrastructure that the tenant (JWI) farms and that the Estate of Lewis C. Frenzl controls. It begins to reveal as telling that the immediate goal was to drain the JHF Trust into projects that would indirectly show as benefiting LCF — while the end goal, documented across the rest of this chapter and Ch.3, was to convert JHF Trust assets into JWI's possession.

The 2015-return asset additions, kept together as one tax group:

- 2016.06.07 — 'Sprinkler Tires' placed in service, $6,400.00. No location specified (sandhills vs. baseline pivots unstated). Strangely, no MACRS depreciation statements.

- 2016.07.01 — 'Building Repairs' placed in service, $15,271.00. The only buildings within JHF Trust reach are on the homestead property — controlled through the Estate of Lewis C. Frenzl. No location specified. Trust money, Estate benefit.

- 2016.08.18 — 'Fencing' placed in service, $4,135.00. No parcel location specified.

JHF 2015 Tax Returns · KSH production set

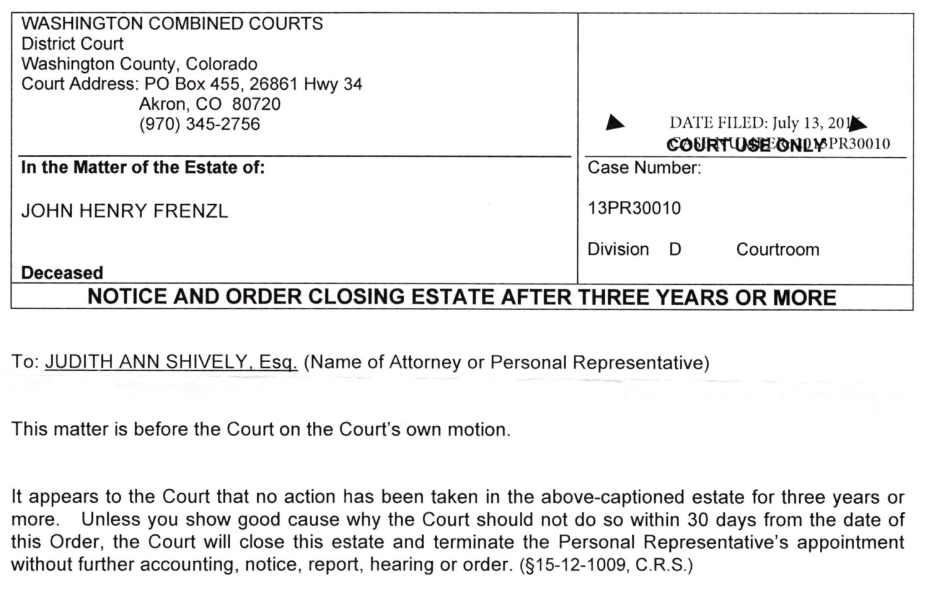

2016.07.13 — Washington County Closes the JHF Estate

The Washington County Combined Courts issues a Notice and Order of Closing Estate After Three Years (C.R.S. § 15-12-1009): three years having passed, the estate closes administratively, without further accounting.

JHF 2016 Three Year Closing N&O

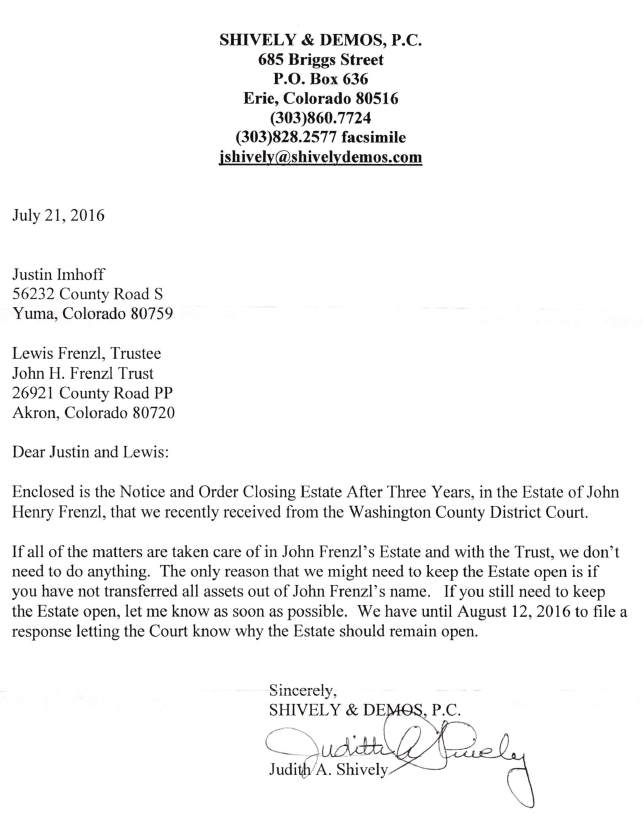

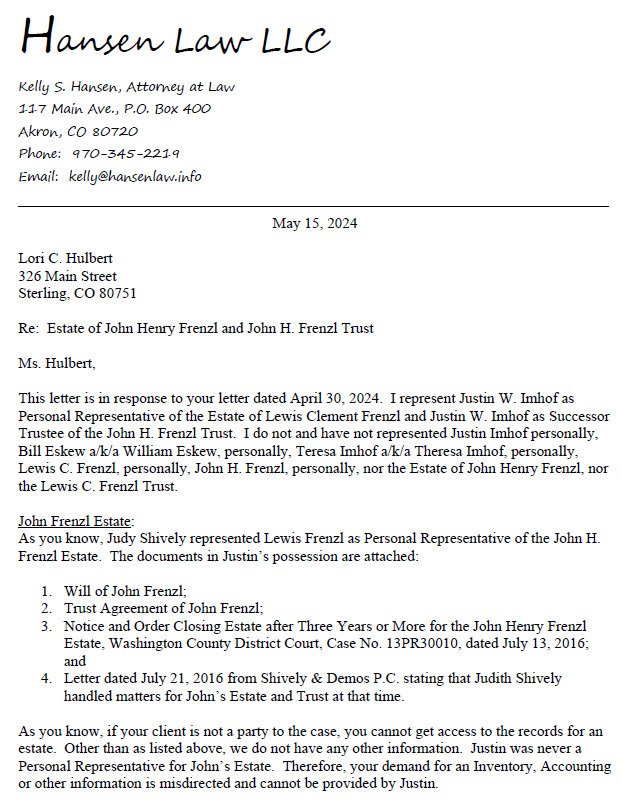

2016.07.21 — The Shively Letter: Why It Was Sent, and What It Disproves

Why the letter exists: John's estate had sat for more than three years with no one completing its administration. Under C.R.S. § 15-12-1009 the court closes such estates by its own motion — the statutory housekeeping that follows says, in effect, "administration is complete; everything has been moved out of the estate; nothing is left." Judith Shively (Shively & Demos, P.C.) sends the closing documentation accordingly.

What was asserted vs. what was true:

The closing's premise — the estate's assets had been fully distributed and nothing remained to administer.

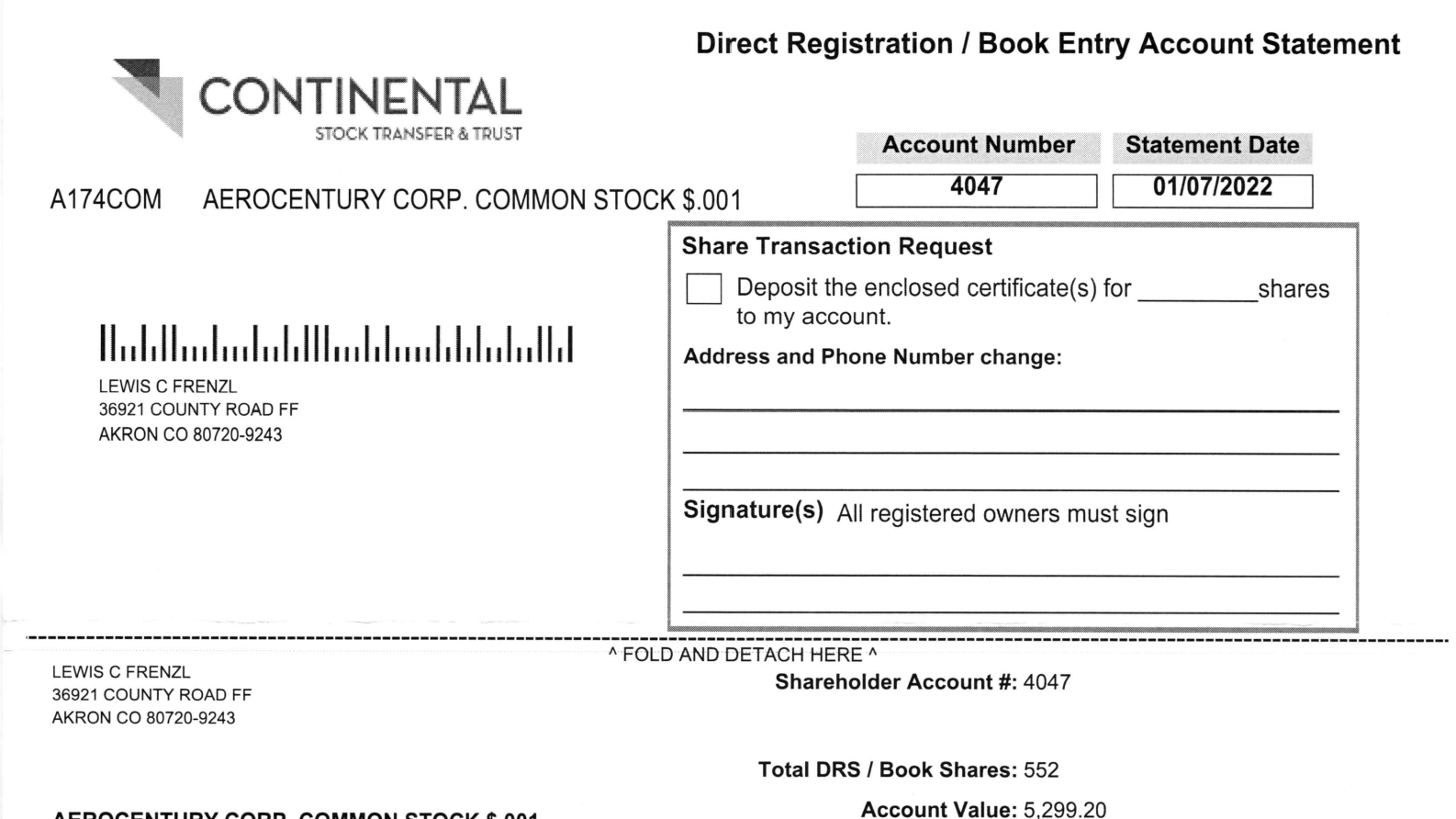

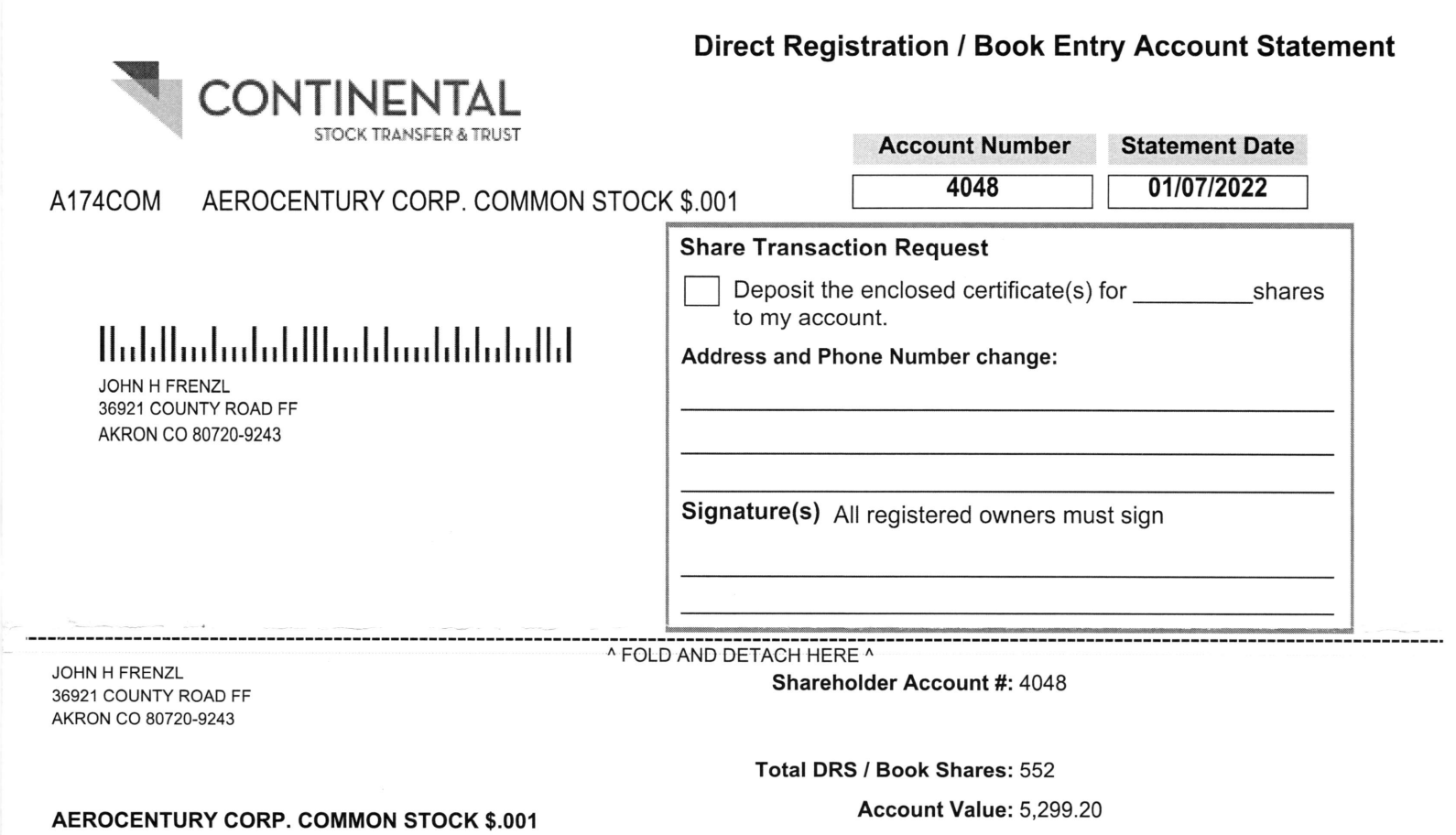

The reality, still true today — there are assets to this day titled in John Frenzl's personal name that belong to John Frenzl's estate and have never been moved into his trust. The pour-over will directs the residue into the JHF Trust — but no trustee, to date, has ever completed that transfer. (Example: the Aerocentury Corp stock still held in John's name as a shareholder in 2022 — see 1/7/2022.)

Who the letter was addressed to — and why that matters:

The document is addressed to JWI and LCF as Trustee — with Justin's name appearing first in the header, above Lewis Frenzl.

What JWI claimed: Justin represented to Landon and Devin Eskew that he had no connection with the JHF Estate — no PR rights, no capacity of any kind. What Kelly Hansen claimed: her 5/15/2024 email states Justin "did not have any dealings with the estate." What the document shows: the estate's own attorney addressed estate correspondence to Justin, first-named, in July 2016.

Both future statements are factually inaccurate against the contemporaneous record.

Shively letter 7/21/2016 · Kelly Hansen email 5/15/2024 · JHF 2016 Three Year Closing N&O

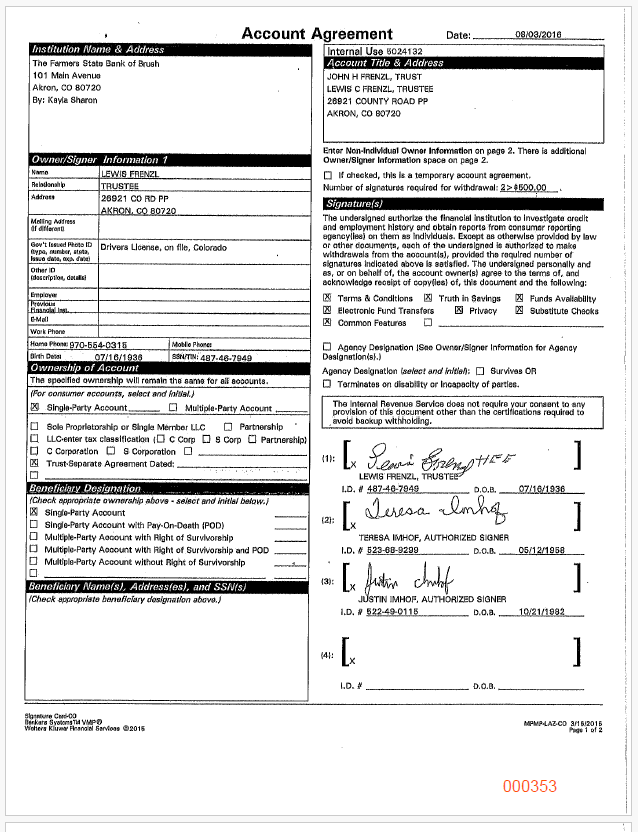

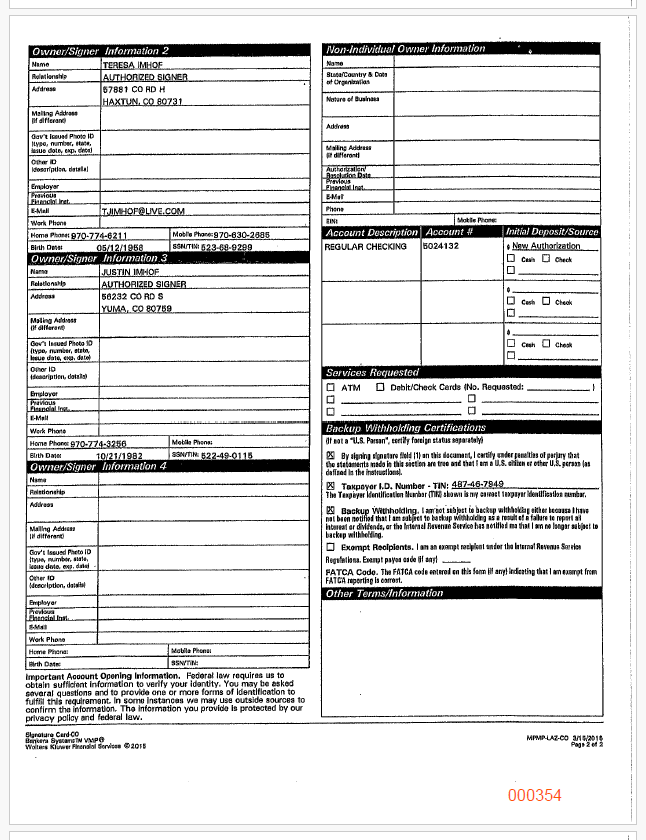

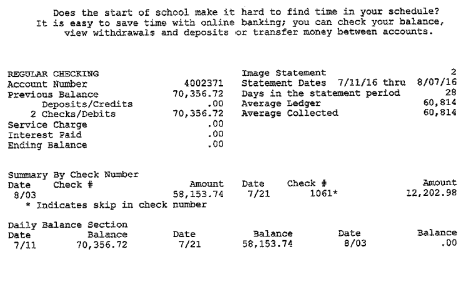

2016.08.03 — JWI and TJI Become Signatories (JWI000353–000354)

Justin Imhof and Teresa Imhof are made signatories on JHF Trust bank account xx2371.

JWI000353–000354 — signature card / account agreement adding JWI and TJI to JHF Trust account xx2371, 8/3/2016. See also FSB Discrepancies/2016.08.03 LCF TJI JWI Account Agreement.pdf.

(account agreement continuation — caption pending review)

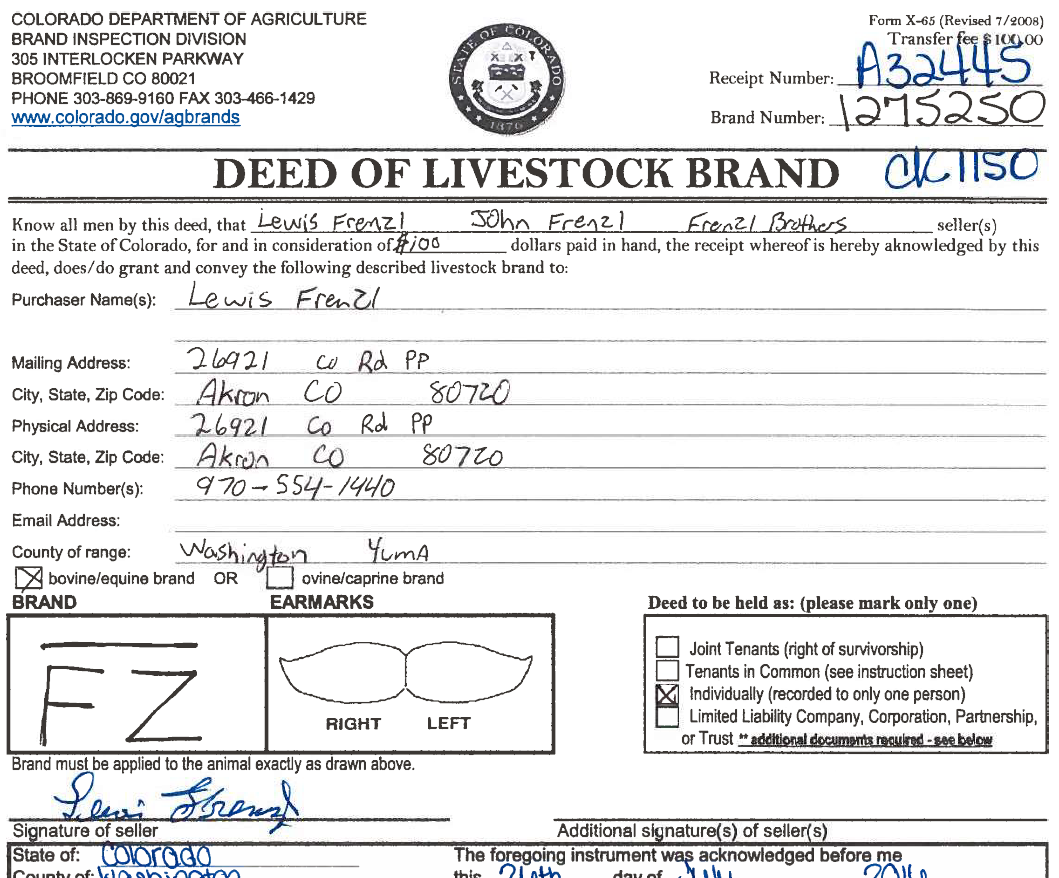

2016.08.04 — Bar FZ Brand Transferred Out of the Estate

One month after the court closes the JHF Estate, the "Bar Over F Strung Z" (Bar FZ) livestock brand is transferred out of JHF's Estate. The handwriting on the transfer paperwork has been analyzed and determined consistent with Justin Imhof's hand. On 4/3/2024, Kelly Hansen stated the Bar FZ brand became deeded solely to Lewis Frenzl under the terms of John's 2000 Will — but the JHF Will directs the residue of John's property to the JHF Trust, not to Lewis Frenzl personally. (Cite '193-380' from the 2024.04.03 email; submit to court record.)

PETITIONER'S EXHIBIT #12 — brand transfer documentation. Note handwriting discrepancies.

PETITIONER'S EXHIBIT #30 — (caption pending Landon review)

2016.08.07 — The Account Is Cleared (JWI000572)

Four days after Justin and Teresa Imhof are added as signatories, the JHF Trust account is cleared out.

Lean on the sequence, because the sequence is the evidence: Lewis Frenzl had been the sole signatory on this account for nearly four years without incident. The drawdown did not happen in those four years. It happened the same week two new names went on the signature card — and it was not Lewis's decision. It was Justin and Teresa making the specific decision to move the rest of John Frenzl's money out of John Frenzl's trust account. That is theft — plain and simple, stated factually: trust funds left the trust's account at the direction of non-beneficiary signatories with no trust purpose, no documentation, and no authority beyond physical access to the account.

The money was only put back as 2017 arrived — when the scholarship needed paying, or taxes came due, or some obligation of that effect forced the issue — and, on the record as we read it, when Lewis realized his brother's money was not there. Even then the replacement came back approximately $20,000 short. There is no explanation anywhere in the produced record for where that $20,000 went or why the restoration was deficient. That explanation is owed by — and can only come from — the signatories who initiated the transfer.

JWI000572 — JHF Trust account xx2371 activity showing the post-signatory drawdown, 8/7/2016, and the deficient replenishment ~5 months later.

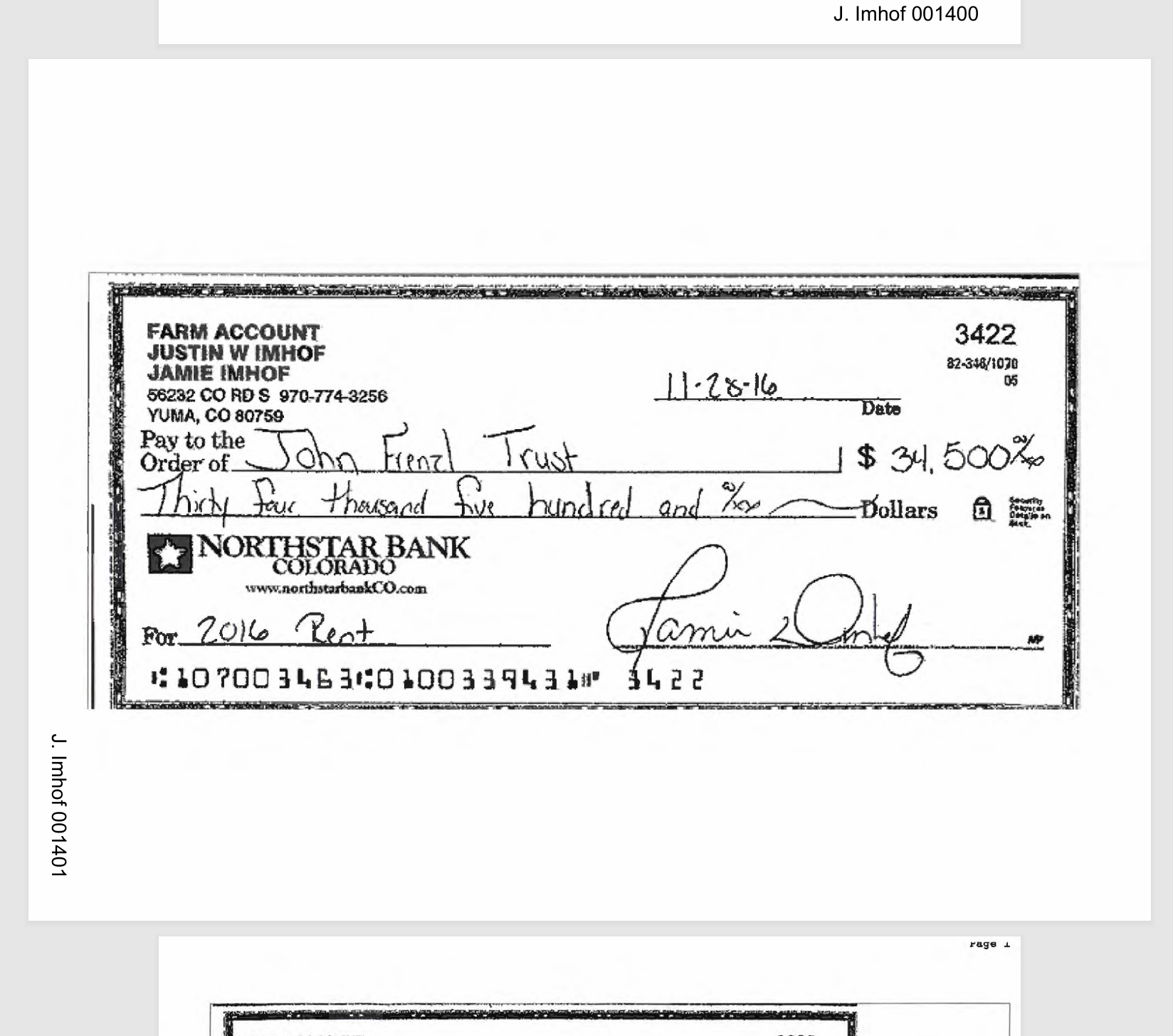

2016.11.28 — The Rent Check That Had Nowhere to Go (JWI001401)

From JWI's 3rd Supplemental Disclosures: Justin writes a rent check that CANNOT BE deposited into any JHF Trust account — and that DOESN'T GET deposited into any JHF Trust account.

Why couldn't it be deposited? Because the account was gone. Reading the produced records together with the 8/7/2016 drawdown: Justin and Teresa had closed the JHF Trust bank account (xx2371) after clearing it. So when a rent check finally materialized for the Trust, there was no JHF Trust account in existence to receive it — and instead of reopening the Trust's account, the check was funneled back through an account that did not belong to John Frenzl or his Trust. Trust income, laundered through a non-trust account, at the direction of the same two signatories.

This single exhibit cross-references three independent problems: (a) the account closure that should never have happened, (b) a rent payment whose existence contradicts the years of "no rent due" silence, and (c) the deposit of trust income somewhere other than the trust.

JWI001401 (JWI 3rd Supplemental Disclosures) — the 11/28/2016 rent check. Cross-reference: JWI000572 (account drawdown/closure), 2019–2020 $36,500 in-and-out cycles (below), Petitioner's Exhibits #28–#30.

2016.12.31 — Cumulative Breach Ledger

As of December 31, 2016 (new items from this year stacked at top):

- ☐ NEW: Account xx2371 cleared 8/7/2016 by new signatories JWI/TJI; restored months later ~$20,000 deficient — deficiency unexplained

- ☐ NEW: JHF Trust account closed by signatories; 11/28/2016 rent check (JWI001401) diverted into a non-trust account

- ☐ NEW: Bar FZ brand transferred out of the estate (8/4/2016) in JWI's handwriting, contrary to the JHF Will's residue-to-Trust direction

- ☐ Whereabouts of the CaseIH sprayer (½ JHF Trust) — still unknown

- ☐ Binder documents removed by JWI — still unreturned; Shively file still unproduced

- ☐ No proof of JWI lease payments, growing seasons 2013–2016

- ☐ No proof of any $150,000.00 Scholarship Fund contribution

2017

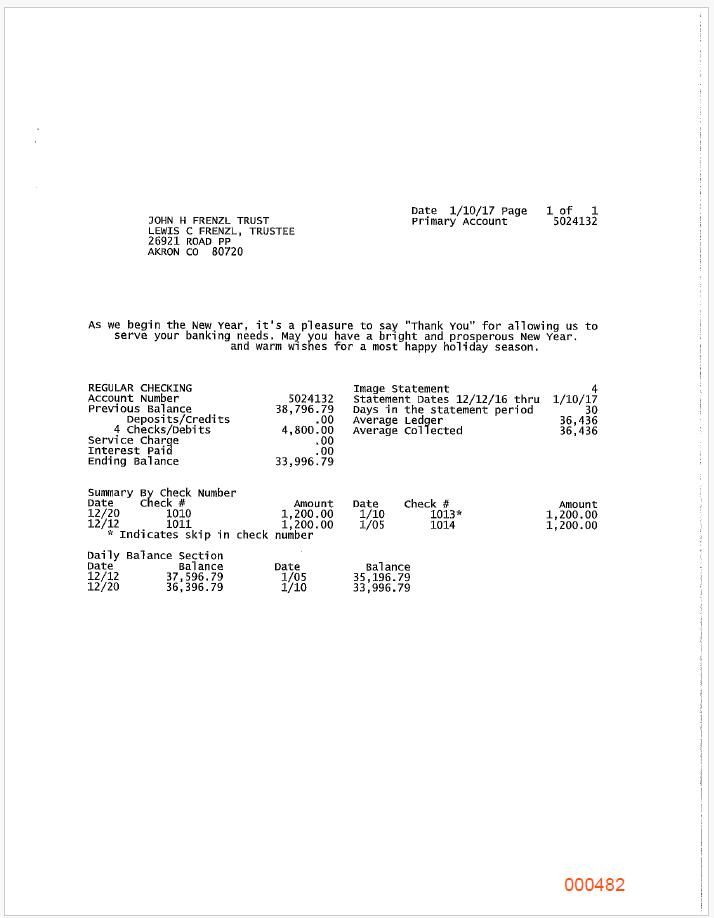

2017.01.10 — JWI000482

JWI000482 — (caption pending Landon review)

2017.01.27 — Third Farm Lease (WaCo REC#866668)

Three years after the second Farm Lease, a third replacement Farm Lease is drafted between the JHF Trust and Justin Imhof as Lessee, covering 100% of Washington County lands owned 50% by Lewis Frenzl's Estate and 50% by the JHF Trust. Signed by Lewis Frenzl as Trustee. Still backdated to 1/1/2013. Term now runs to December 31, 2032.

Rental terms matrix — all three leases plus term escalation:

| Item | Original (REC#857958, 9/11/2013) | Second (REC#859040, 1/28/2014) | Third (REC#866668, 1/27/2017) |

|---|---|---|---|

| Term & renewal | 5-year term + automatic 5-year renewal | 10-year term + automatic 10-year renewal | 20-year horizon — expires 12/31/2032 w/ automatic renewal |

| Grassland | $18/month/pair | $18/month/pair | $18/month/pair ✅ |

| Non-irrigated | 2/3–1/3 split + USDA pro-rata | $30 flat/acre, JWI keeps 100% USDA | $20 flat/acre, JWI keeps 100% USDA ❌ |

| Irrigated | 60/40 split + USDA pro-rata | $100 flat/acre, JWI keeps 100% USDA | $100 flat/acre, JWI keeps 100% USDA |

| Fencing materials | JHF Trust pays 100% | JHF Trust pays 100% | JHF Trust pays 100% ❌ |

| Irrigation costs (utilities, repairs, maintenance, motors, sprinklers) | JHF Trust pays 100% | JHF Trust pays 100% | JHF Trust pays 100% ❌ |

| Backdated effective date | 1/1/2013 | 1/1/2013 | 1/1/2013 ❌ |

The renewal periods were increased by JWI across each individual lease — five, then ten, then twenty — not all within this one document. Each renegotiation roughly doubled the length of time the degraded terms would bind the Trust. By the third lease, a contract that began as a 5-year commitment had become a multi-decade encumbrance at $20/acre dryland with the Trust still paying all infrastructure costs. (Formatting note: this matrix must render identically in the .md and in any .pdf export — keep it as a plain pipe table, no HTML.)

Supersession error: REC#866668 cites REC#857958 (the first lease) as the instrument it supersedes — but REC#859040 (the second lease, which itself superseded REC#857958) is the operative lease on this date. The incorrect predecessor is cited.

Document irregularities (comparing REC#859040 and REC#866668 side by side):

- Under Leased Premises, N½-Sec5 (100% JHF Trust land) now specifies "grass corners" — further devaluing the rent basis for that parcel for the next twenty years

- "Renewel" is misspelled in the Term section

- Right-hand margins do not align in the Rent section

- Multiple inconsistent font types and sizes, including the last three words of page one

- Same 1/1/2013 backdate as every prior lease

Document formatting is inconsistent with attorney-prepared instruments. No evidence exists that the JHF Trust had independent legal counsel review this lease. At the time, 80-year-old Lewis Frenzl, who did not use a computer at this level, would not have caught that small tweaks were accumulating to Justin Imhof's benefit.

PETITIONER'S EXHIBIT #31 — REC#866668 third Farm Lease.

(lease comparison detail — caption pending review)

857958 · 859040 · 866668

2017.12.31 — Cumulative Breach Ledger

As of December 31, 2017:

- ☐ All 2016 ledger items remain open

- ☐ No proof of JWI lease payments, growing seasons 2013–2017

- ☐ No proof of any $150,000.00 Scholarship Fund contribution

2018

2018.02.21 — Account Lock-Out Order (JWI000352)